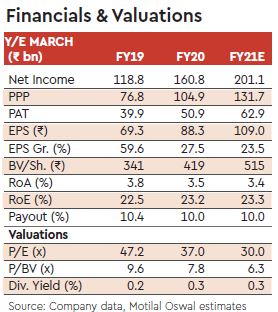

Bajaj Finance’s PAT grew 43% y-o-y to Rs 12.0 bn (in line) in Q1FY20. The quarter was characterised by continued strong AUM growth and stable margins/ asset quality. Consol. AUM increased 41% y-o-y to Rs 1.3 trn, led by strong growth across segments, barring commercial lending. Adjusted for the IPO funding book, AUM growth was at 38% y-o-y. AUM growth in consumer B2B financing was robust at 31% y-o-y, driven by 60%+ y-o-y growth in 2W/3W finance. In 2W lending, BAF financed 51% of Bajaj Auto’s 2W sales v/s 44% in Q4FY19 and 34% in Q1FY19.

Margins (calc.) were sequentially stable at 12%, with cost of funds largely stable at 8.5%. The borrowing mix was mostly stable q-o-q, with share of bank/ market borrowings at ~33%/50%.

Asset quality remained stable, with the GNPL ratio at 1.6% and PCR at 61%. However, BAF experienced an increase in overdues in certain products, such as digital product financing and 2W/3W financing. As a result, management has decided to cut fresh disbursements by 15-18% in digital products, and by 10-12% in SME and consumer B2C.

On liability side, company continues gaining traction in deposits, the share of which in borrowings increased ~500bp y-o-y to 14%. Fee income continues growing faster than balance sheet —it was up 65% y-o-y to Rs 5.7 bn.

Bajaj HFC: Its book now stands at ~Rs 220 bn v/s Rs 72 bn in the year-ago period. It reported PAT of Rs 0.7 bn. Asset quality was largely stable, with the GS3 ratio at 0.06% and PCR at ~35%.

Valuation view

BAF has maintained its robust growth trajectory, with deepening geographical penetration and increasing repeat business. Over the past two years, it has also enhanced its capabilities on two fronts— generating higher fee income and improving the deposit franchise. We expect the improving deposit franchise to be a key driver for incremental liabilities over the next few years. Given its parentage and AAA-credit rating, BAF has comfortably sailed through the recent liquidity crisis and maintained strong growth rates. However, the recent asset quality concerns in certain products might cause some slowdown in loan growth. We expect AUM growth of 30% y-o-y for FY20 v/s 38% CAGR over past three years. We largely maintain our estimates. Neutral with a TP of Rs 3,550 (7x FY21e BVPS).