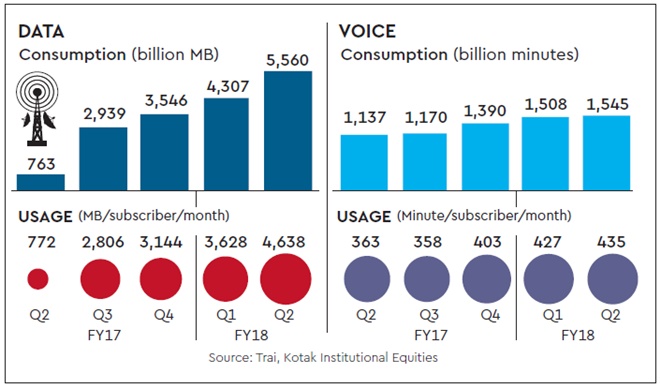

After almost a year of declining revenues, there is finally a silver lining for telecom operators if the latest numbers from the Telecom Regulatory Authority of India (Trai) on the sector’s performance during the July-September quarter of 2017-18 are to be believed. The industry revenue from data alone rose for the second consecutive quarter on a sequential basis. Data revenue during Q2FY18 rose by a staggering 59% to Rs 11,900 crore, compared with Q1FY18, registering a quantum growth quarter-on-quarter. On a year-on-year (Y-o-Y) basis, data revenue grew double-digit at 27% from Rs 9,400 crore in Q2FY17. Analysts said revenue from data rose in FY18 as Jio started charging its subscribers from April 1, 2017. Besides, when the company revised its tariff plans in July 2017, they became costlier by around 33% for consumers. The move also provided the industry with an opportunity to stem the free fall in ARPU levels seen in the past quarters. According to Kotak Institutional Equities, the ARPU range of Jio’s plans announced in July stood at Rs 122-661, as against Rs 97-630 announced earlier. Besides, as operators came out with more bundled offers to not just ring-fence their higher ARPU subscribers but also to add more data users and encourage 2G users to upgrade to 4G, consumption rose manifold. Average data consumption per subscriber on a Y-o-Y basis rose six-fold to more than 4.6GB during Q2FY18 from 772 MB.

Brokerage firm CLSA in a report in November said, “Jio’s launch has triggered an exponential growth in data usage with Bharti also seeing a 4x jump in per-subscriber usage to over 4GB/month. While Bharti lost data subscribers when Jio was free, since April 2017, when Jio turned pay, Bharti has added over 8 million data subscribers and 14 million 3G/4G data subscribers.” Another factor spurring data consumption is the growth in smartphone users. India has around 400 million smartphone users, which is expected to grow in the near and medium term, as more consumers upgrade to smartphones. Analysts expect more than 50% of the country’s population using smartphones in the next two-three years. According to CLSA projections, feature phone shipments in FY19 will remain flat at 137 million compared to FY18, whereas smartphone shipments will grow by more than 7% to 131 million during the same period. According to research firm Canalys, India overtook the US as the world’s second-largest smartphone market after China, with shipments touching a record 40 million units during October-December 2017.

While the story of India’s experiments with data is bright, the voice segment is still a sore point for telecom operators. Voice revenue and ARPUs have been weakening consistently as incumbents diluted their bundled plans to cater to a larger base of customers. Voice revenues have been declining consistently since the last five quarters. Revenue during Q2FY18 stood at `17,000 crore, a quarter-on-quarter decline of 13%. The year-on-year drop was steeper at 34% from Rs 25,700 crore. The decline in voice revenue in Q2FY18 against Q1FY18 was more compared to that in Q1FY18 compared to Q4FY17 as July-September is a seasonally weak quarter. Also, operators absorbed the increase in indirect taxes due to a GST rate of 18% against a service tax of 15% as intense competition prevented any pass-through of the hike to subscribers.

The decline is also more pronounced owing to the intensifying competition in the market. BNP Paribas said that even though subscriber growth is returning for Bharti Airtel, Vodafone India and Idea Cellular on the back of the exit of weaker operators, the incumbents have become more aggressive reducing their price premium over Jio – to around 10%. The brokerage in the same report in November said that it expects Arpu pressure to continue in Q3FY18 given the interconnect usage charge (IUC) rate cut, acquisition of low-end customers and aggressive new plans. “However, we expect recovery starting Q4FY18 due to industry consolidation, tariff increases by Jio, unsustainable tariff levels and rising data usage,” the report added.