At the last count, more than three dozen applicants were awaiting a Payment Aggregator (PA) licence. The rush is surprising not only because the space is crowded with some 30 incumbents but also because the rules of the game are tough. The proverbial spoke in the wheel in the Reserve Bank of India’s draft guidelines is the CPV—or the Contact Point Verification.

The need for a physical KYC and the accompanying due diligence requirements are onerous. In fact they’re very similar to what the RBI expects of universal banks. In addition, PAs also need to verify the bank account in which the funds of merchants are settled. Ranadurjay Talukdar, Partner and Payments Sector Leader, EY India is of the view that conducting a CPV, is a tedious and time-consuming process, especially for smaller merchants. “This could have an adverse impact on payment acceptance itself because it will not be cost-effective to verify small merchants,” Talukdar said, adding that it could be a deal-breaker for some. He also points out that if PAs opt to not service smaller merchants funds could be diverted to their personal accounts. “This will impact peer-to-merchant volumes,” he added.

By one estimate a physical verification could cost as much as Rs 5,000 per KYC. Outsourcing the task to Business Correspondents (BC) or other agencies could result in incomplete verification given the volumes will be large. Nidhi Tiwari, Partner, Kearney, feels that given the costs and the onerous responsibilities, PAs will require focused strategies to be able to sustain their operations. “It will require lot of focused work and effort to identify the right use cases, the right segment of merchants to focus on and the right value proposition for targeting those merchants,” she told FE.

Some incumbents have suggested that a KYC done by a bank for a merchant should be adequate for the PA too. However, as Vivek Mandhata, Managing Director &Partner, BCG points out, while this may be the ideal answer, the regulator may want the PA to take full accountability of KYC as well because the settlement process is such that the money is being routed from the sponsor bank via the PA’s bank to the end-customer’s bank account.

RBI is also unlikely to allow designated providers to help with the KYC process, as other regulators have done. It is also unlikely to accept the website as the place of business for an online venture. Even as costs stay high since PAs will also need to invest in technology and incentives for customers, the margins will be wafer-thin.

As Ramakrishnan Ramamurthy, Executive VP, Worldline Solutions, points out, the margins could be 4-10 basis points. “As such, only entities that have the appetite to play a large volume game will survive,” Ramanurthy says. Ironically, though, it is this difficult environment that is prompting many to stay in the game. Each one’s hoping the others will get out sooner or later and they will be the last men standing. A couple of them have quit realizing the “real impact of putting in place the structure to commence the operations”. But, as Ramamurthy points out, there is scope to create value even beyond the cross-selling opportunity. “There are niches to be exploited especially with offline transactions also coming into the fold. With smaller merchants you can a charge a little more,” he says.

Tiwari believes players are looking to influence the merchant and consumer payment transaction journey experience. “The PA route can help players to have an influence on the merchant’s and consumer’s transactions and gradually try and monetise this. No one wants to miss this opportunity,” Tiwari says. She observes that most of the players are hoping they will be able to cross-sell. “PAs are looking at value-added services and lending opportunities,” she says.

As Talukdar points out, the addressable opportunity is big because it includes everything from UPI, cards to wallets. “It’s much more than just P2M, it can also be B2B since suppliers and vendor payments are also included, as well as B2G and P2G flows (payments made to the government). There are also commercial cards which target RTGS/NEFT flows and which fetch the bank interchange and interest revenues” Talukdar says.

The point, however, is that PAs don’t control the type of transaction, which could be either a low-margin UPI transaction or a more lucrative card transaction. As BCG’s Mandhata points out, “it will be more about how they capture value chains and transaction volumes.”

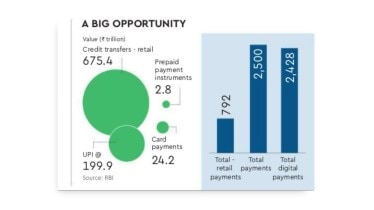

The total value of digital payments in FY24 was Rs 2,428 trillion. While retail transactions add up to some $3.6 trillion, Tiwari points out a good part of the payments is accounted for by UPI transactions which attract zero MDR. “So money will have to be made through lending and value-added services,” she says. Indeed, as EY’s Talukdar points out, big business groups like the Tatas and Reliance Industries are also attempting to capture the in-house flows by setting up their own PA entities. According to BCG’s Mandhata, while the market may be initially fragmented, there will be consolidation. “It is not a high economics play but a scale business so there will be some exits,” he says. Unless the regulator has a change of heart the exits could be many.