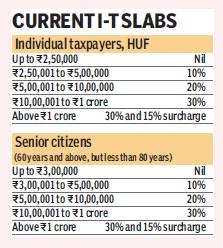

As Finance Minister Arun Jaitley presents Budget 2017 on Wednesday, individual tax payers will wait to see if he raises the exemption limits from Rs 2.5 lakh, changes the tax slab rates, increases the investment limit under Section 80C and makes maturity withdrawal from National Pension System (NPS) completely tax free. The finance minister has said that the government, at some stage, will make taxes, both direct and indirect, more reasonable.

Deductions under Section 80C

Section 80C has a maximum limit of Rs 1.5 lakh. Investments in Public Provident Fund, National Savings Certificates, employee’s contribution to provident fund, tax-saving mutual funds, five-year fixed deposits in banks or post office and premiums paid for life insurance products all come under the purview of Section 80C. It also covers market-linked investment options, such as equity-linked savings scheme of mutual funds and unit-linked insurance plans. The limit was last increased in 2014 Budget from Rs 1 lakh to Rs 1.5 lakh. Tax experts feel that the limit should be increased to incentivise individuals to save, invest and contribute towards the economy.

You may also like to watch:

[jwplayer vffub1XP]

National Pension System (NPS)

In the 2015 Budget, finance minister Arun Jaitley introduced an additional income tax deduction (from FY 2015-16) of Rs 50,000 for contribution to NPS under Section 80CCD(1B). To get the tax deduction, the investment has to be made in Tier I NPS account only. There is no upper limit on contribution to NPS. But an individual will get tax deduction of only up to Rs 50,000. This is above the 80C limit of Rs 1.5 lakh.

The deduction is irrespective of the type of employment. So, a government employee, a private sector employee, self employed or an ordinary citizen can claim benefit of R50,000 under Section 80CCD(1B). Other two sections of tax deduction are Section 80CCD(1) and Section 80CCD(2). The first is for those who only contribute to NPS and not to EPF. Employee contribution up to 10% of basic salary and dearness allowance (DA) up to Rs 1.5 lakh is eligible for tax deduction. The self employed can also claim this tax benefit.

Under Section 80CCD(2), employer’s contribution up to 10% of basic plus DA is eligible for deduction. Employer’s contribution is an additional deduction as it not part of Rs 1.5 lakh allowed under Section 80C. So, it is also beneficial for employer as it can claim tax benefit for its contribution by showing it as business expense in the profit and loss account.

NPS falls under the EET (exempt-exempt-tax) regime. The account holder will have to compulsorily buy an annuity with at least 40% of the corpus amount at the age of 60 plus. The corpus will be the total of his contribution plus the returns earned from his investments. So, on this 40%, there will be no tax at the time of maturity. However, income from annuity will be taxed at the individual’s tax-slab rate.

In last year’s Budget, the finance minister had made withdrawals from NPS on maturity tax free for up to 40% of the total corpus accumulated. So, effectively an individual has to pay tax on 20% of the maturity corpus. Other savings schemes such as PPF and EPF, however, enjoy tax benefits in all the three stages: contribution, interest earned and withdrawal. So, it is expected that the government will make NPS completely tax free.