Economic Survey 2017: Arvind Subramanian’s Economic Survey has categorically slammed rating agencies – Standard & Poor’s – for not changing India’s credit rating, while upgrading that of China. Subramanian questions the ‘poor standards’ of ratings agencies, slamming them for not considering India for a ratings upgrade. “In the case of India, Standard & Poor’s in November 2016 ruled out the scope for a ratings upgrade for some considerable period, mainly on the grounds of its low per capita GDP and relatively high fiscal deficit. The actual methodology to arrive at this rating was clearly more complex. Even so, it is worth asking: are these variables the right key for assessing India’s risk of default?” That’s the question that the survey has raised!

Per capita GDP: According to the Survey, this is a very slow moving variable. Lower middle income countries experienced an average growth of 2.45% of GDP per capita (constant 2010 dollars) between 1970 and 2015. At this rate, the poorest of the lower middle income countries would take about 57 years to reach upper middle income status! So if this variable is really key to ratings, poorer countries might be provoked into saying, “Please don’t bother this year, come back to assess us after half a century”, the survey mocks.

You may also like to watch this:

[jwplayer bIVBV6eI]

Fiscal variables: India is deemed an outlier because its general government fiscal deficit ratio of 6.6% (2014) and debt of 67.1% are out of line with its emerging market “peers”. India has a strong growth trajectory, which coupled with its commitment to fiscal discipline exhibited over the last three years suggests that its deficit and debt ratios are likely to decline significantly over the coming years, the survey says, adding that even if this scenario does not materialise, India might still be able to carry much more debt than other countries because it has an exceptionally high “willingness to pay”.

Now, contrast this to China…

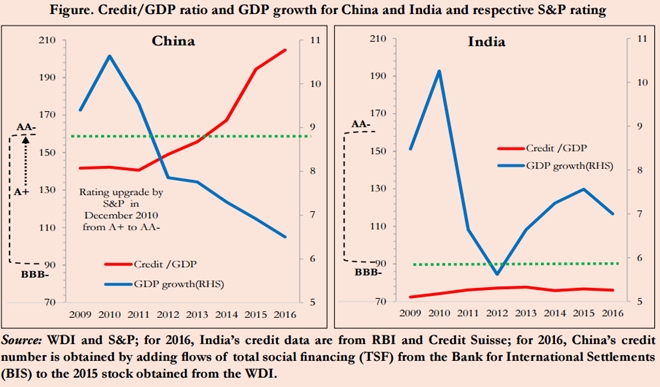

In 2009, China launched a historic credit expansion, which has so far seen the credit-GDP ratio rise by an unprecedented about 63 percentage points of GDP, much larger than the stock of India’s credit-GDP. At the same time, Chinese growth has slowed from over 10% to 6.5%, the survey points out. (see figure below)

So, why does China deserve a ratings upgrade then? How did Standard and Poor’s react to this ominous scissors pattern, which has universally been acknowledged as posing serious risks to China and indeed the world? the survey questions. “In December 2010, S&P increased China’s rating from A+ to AA – and it has never adjusted it since, even as the credit boom has unfolded and growth has experienced a secular decline. In contrast, India’s ratings have remained stuck at the much lower level of BBB-, despite the country’s dramatic improvement in growth and macro-economic stability since 2014.” the survey elaborates. Subramanian doesn’t mince words! He says that these contrasting experiences raise a question: can they really be explained by an economically sound methodology?