All eyes are on the upcoming budget and a lot of speculation about the launch of schemes have been made for the power and renewable sector. According to a recent study by CRISIL, the capex for renewable power may see double digit allocation and the capacity is seen at 180 GW by FY26 with solar energy continuing to dominate.

Crisil report on possible capacity increase

The renewable energy capacity stood at 72 GW in FY20 and increased by 35 per cent to 97 GW in FY22. As of now, the capacity is at 130 GW at the end of FY24.

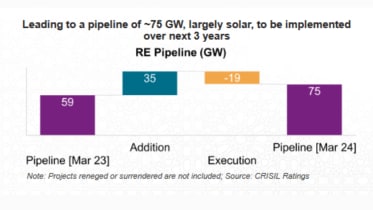

According to CRISIL, healthy executable pipeline of 75 GW will contribute 75 per cent of 50 GW addition while C&I and roof-top may contribute remaining 25 per cent going forward in FY25 and FY26. The auctioned capacity in FY24 increased 2.5x to 35 GW from 12 GW in FY23.

Further, 12 GW of renewable energy additions is likely to come from solar rooftop and C&I supported by favourable policy changes. The PM rooftop solar Yojana has an outlay of Rs 75,000 crore to bring solar rooftop to 1 crore households. The launch of online portal PM Surya Ghar is expected to make the approval and implementation process easier. Additionally supportive green open access policies of select states and reduction in open access charges for select states is expected to haten the transition.

The risks involved

Relatively high tariffs of storage and storage linked capacities pose a risk to increasing renewable energy adoption. Nearly 65 per cent of auctioned capacity has power supply agreements unsigned till April 2024. Tariffs are relatively high when compared to pure-play solar/wind since these projects store power at time of generation and discharge later at time of demand. Hence, tariffs of such projects should be compared with thermal project tariffs that can also supply power all day and match with demand. Moreover, development of timely storage infrastructure is critical for absorption of intermittent and uncontrollable nature of renewable generation.

What’s the capital required and plan to raise it

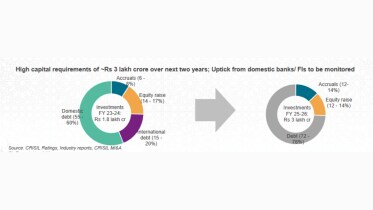

Notedly, there is a requirement of high capital of approximately Rs 3 lakh crore over next two years. Uptick from domestic bank also need to be monitored. The investments in FY24 stood Rs 1.8 lakh crore, out of which domestic debt was a major part of it, at around 55-60 per cent. International debt is at 15-20 per cent. The Equity share is at 14-17 per cent and accruals account for 6-8 per cent respectively. For FY25-26, debt is targeted to account for 72-76 per cent in the investments, followed by equity and accruals, at 12-14 per cent each respectively.

Leverage is expected to be stable at about 6.8-7.0 times driven by stable operational performance, receivables to remain steady, excluding capex, leverage is 5–5.5 for operating portfolio. Meanwhile, higher capex intensity to put pressure and raise of equity to be monitorable.