The Reserve Bank of India (RBI) on Friday announced that it will conduct Rs 50,000 crore worth of long-term repo operations (LTRO) that would be equally split between the one-year and three-year tenors. The 3-year LTRO will be conducted on February 17 while the one-year LTRO will be done on February 24.

The central bank clearly stated that banks would be required to place their requests for the amount sought under LTRO at the prevailing policy repo rate and bids below or above the policy rate will be rejected. The announcement was first made during Thursday’s monetary policy where the central bank stated it will conduct term repos of one-year and three-year of appropriate sizes for up to a total amount of `1 lakh crore at the policy repo rate.

This means banks would be able to borrow one-year and three-year tenor money at just the policy repo rate, that currently stands at 5.15%. “Since June 2019, the Reserve Bank has ensured that comfortable liquidity is available in the system in order to facilitate the transmission of monetary policy actions and flow of credit to the economy. These efforts are being carried forward with a view to assuring banks about the availability of durable liquidity at reasonable cost relative to prevailing market conditions,” the RBI had said.

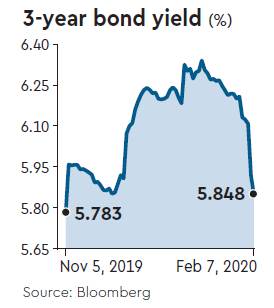

The announcement has led to drastic fall in short-term bond yields with the rally continuing even on Friday. For instance, the 3-year government bond yield has dropped a total of 26 basis points over the last two days to a three-month low of 5.848%.

MS Gopikrishnan, independent market expert, believes that the market could be disappointed with the fact that the first set of LTROs have been split 50:50 between the two tenors rather than announcing a larger quantum for the 3-year tenor.

“The market could have been hoping the bulk of the amount to be allotted for the 3-year tenor. If this trend continues then the next Rs 50,000 crore would also be split in the same way. As a result, there could be a limit to further fall in the short-term yields as the demand would outpace the supply for LTRO. This is because those market participants who do not get the money in the LTRO may sell the short-dated securities that they recently lapped up,” Gopikrishnan said.

Going forward, it would be noteworthy to watch whether the RBI will do further LTRO in addition to the already announced Rs 1 lakh crore. If that happens, there could be further downward pressure on the short-term yields which at present are already headed towards the lows seen during the financial crisis times.

The central bank also pointed out that in case of over-subscription of the notified amount, the allotment will be done on pro-rata basis. The eligible collateral for LTROs and the applicable haircuts will remain the same as applicable for LAF.