– By Pranav Trigunayat

The IMF has recently revised India’s GDP growth rate for 2024-25 by 20 basis points from the previously project 6.8% in April to 7%. On the same lines the World Bank has also increased its projected growth rate for India from 6.8% to 7.2% and the Asian Development Bank has retained its forecast at 7% for 2024-25. This upward revision rides on multiple factors which come together at a time when the projections for many developed countries like US and Japan have seen a dip, plagued by disruptions and slowdowns. It is important to point out that this revision follows a slower growth of real GDP in Q1 of 2024-25 which grew at 6.7% as compared to 8.2% in the corresponding quarter of 2023-24.

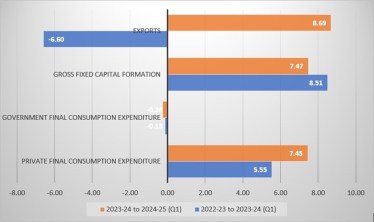

While there have stipulations pinning this slowdown on the damp performance of agriculture (growing at 2% in Q1 of 2024-25 vis-à-vis 3.7% in Q1 of 2023-24), services (registering a continuous decline in the growth rate from 16.7% in Q1 2022-23 to 10.7% in Q1 2023-24 and 7.2% in Q1 2024-25) and reduced public expenditure (which declined in absolute terms), there are a number of reasons to believe that the Indian economy is likely to better its performance. The prime driver of this growth is believed to be an increase in agricultural growth rate buoyed by a robust monsoon and an increase in the area under kharif cultivation. According to a notification released by the Ministry of Agriculture, the area under paddy and pulses have increased by 9% and 9.3% respectively and the overall increase in area under kharif crops has been 16.38% as compared to the previous year. The government of India, in June, also announced an increase in the MSP of all 14 kharif season crops, which carries the potential of reviving rural demand when seen in conjunction with higher sowing. The higher rural demand is likely to provide a thrust to growing private final consumption demand which has witnessed an increase in the growth rate from 5.55% to 7.45% between first quarters in 2023-24 and 2024-25 respectively (See figure 1). Additionally, the external trade performance has also shown symptoms of a substantial recovery in the backdrop of slowing global activity, with exports growing at 8.69% in Q1 2024-25 relative to Q1 2023-24 in which it had contracted by 6.6%. The festive season in Q2 and Q3 if 2024-25 is also likely to provide a fillip to consumer sentiments and foster a higher growth of demand, auguring well for the economy. This also bodes well with a constant rise in real wages for all categories of workers in the last one year barring a slight blip for regular salaried employees in Q1 2024-25. A part of the positive outlook, as stated in the RBI monetary policy meeting in June, also stems from sustained growth in the manufacturing sector which has recorded a growth rate of 7% in Q1 of 2024-25 as compared to 5% in the same quarter in 2023-24. This has also been aided by an improved growth rate in electricity, gas, water supply and other utilities (10.4% in 2024-25 Q1 vis-à-vis 3.2% in 2023-24 Q1) and in the construction sector (10.5% in 2024-25 Q1 as against 8.6% in 2023-24 Q1).

Despite these positive indications, there are concerns that must be addressed to meet the revised growth projection. The primary factor underlying these worries is the effect of declining government final consumption expenditure which has contracted further in Q1 2024-25(see Figure 1). In addition to this, after a constant decline since 2017-18, the stagnation in the unemployment rate at 3.2% in June 2023-24 also presents a challenge to the recovery on the demand side. The increasing unemployment rate in rural areas from 2.4% in 2022-23 to 2.5% in 2023-24, in particular, is alarming. This stagnation in unemployment rate comes amidst a swelling labour force participation rate and work force participation rate. A silver lining in this is a contraction in the demand for work under MGNREGA for four months in a row, reflecting higher demand for agricultural labour in the kharif season.

In a similar vein, although India has managed to keep its export growth resilient in an overall global slowdown it faces a number of challenges to keep up its trade performance especially in the event of competition from cheaper Chinese exports. A year-on-year contraction in India’s core sector in August is another hurdle to the industrial resilience and growth. An escalation in geo-political conflict in the middle-east is also likely to cast aspersions on India’s efforts despite a record decline in international brent crude oil prices.

However, the uptick in many metrics does offer India an opportunity for accelerating its long-term economic recovery. The contours of the policy framework in this international situation need to be designed around a resurgence in government expenditure geared towards higher employment generation, capital formation and continuing the export growth. Priorities must also focus on arresting the declining growth trajectory in the services sector and addressing the unemployment landscape. The employment led initiatives announced in the recent budget, according to many experts, suffer from limitations in their ability to generate jobs. The job creation in the private sector hasn’t gained any substantial momentum even as its profits have increased, highlighting the need to revamp employment initiatives. Despite these obstacles, there are reasons to think that certain easy wins exist, creating an opportunity for the Indian economy to overcome its sluggish growth.

(Pranav Trigunayat is Assistant Professor, School of Liberal Studies at BML Munjal University.)

(Disclaimer: Views expressed are personal and do not reflect the official position or policy of Financial Express Online. Reproducing this content without permission is prohibited.)