Thirteen months ago—December 2015—the US Fed hiked its policy interest rate by 25 bps. With much optimism it indicated four rate hikes in 2016. Of which, only one happened, that too at the fag end of the year. In December 2016, again the Fed has indicated three rate hikes in 2017. Given the plethora of arguments on both sides, will it be able to tread the path that it has indicated? Interestingly, the US treasury yields have been rising—with two-year treasury yield up 40 bps in last four months—on expectations of a rate hike in 2017.

In 2016, while the US domestic economic fundamentals were improving, a big reason for the delay in rate hike cycle were global uncertainties. String of weak economic data from China led to massive fall in the Chinese stock market and other global stock markets. The slowdown in China was accompanied by huge capital outflows and devaluation of Yuan. In the first three months of 2016 itself capital outflows were $75 billion (total outflows were $300 billion in 2016). The Shanghai Composite index fell sharply by 18%, while S&P 500 index fell by 9% between January-March 2016. Concerns in Europe, like the Brexit referendum, stressed banks in Italy and Portugal added to the global turmoil.

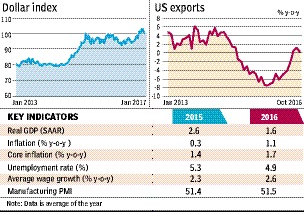

Another factor, which could have made the Fed go slow on the rate hike in 2016 was a strong US dollar. The US dollar had strengthened by 10% in 2015 on US rate hike expectations amid accommodative monetary policy by other major central banks. Strong US dollar has been hurting US exports.

Some parameters for the US economy have improved considerably compared to last year. The unemployment rate has reduced to 4.6%-5.0%, close to estimates of Fed’s normal level. Consumer spending remains robust as wage growth has risen above 2% y-o-y. Monthly inflation rate has been inching up closer to the Fed’s target of 2%. There is a growing expectation that under president Trump, the US would go for fiscal stimulus which would further push-up inflation. These factors have led to increased optimism in the economy and higher credence to strong Fed rate hikes expectations for 2017.

Fed funds rate has been very low since 2008 (0.50%-0.75%, at present). If interest rates continue to remain low even while the economy shows sign of recovery, there is a risk of overheating. Implying that people may start borrowing at low interest rates and investing recklessly, spurring inflation or leading to a financial/real estate bubble. Also, in case the economy is hit by another crisis, the Fed will have limited scope to use monetary stimulus as interest rates would already be low. Low interest rate adversely impact American pensioners and are a big disincentive for savers. This phase of low interest rate, which has lasted for about nine years has been the longest so far.

Global growth outlook has improved and may even be taken as conducive for rate hikes. IMF projects global GDP growth to accelerate to 3.4% in 2017 from 3.1% in 2016. While growth in China is projected to slow to 6.5% in 2017 from 6.7% in 2016, it should not weigh on US policy makers as long as the slowdown is orderly.

But the US economy grew by 1.6% y-o-y in 2016—the weakest pace in five-years. Growth was restrained mainly by poor exports due to strong dollar. Since the second half of 2016, US dollar has gone up by 7%. Evidently, this has again raised concerns on the growth prospects for US exports. President Trump and the US treasury secretary have been making noises on dollar being too strong for their liking. As a result, the dollar rally paused. However, talking down the dollar may only be effective in the short term and will not be sustainable if there are aggressive rate hikes by the Fed in 2017. A stronger dollar would not only jeopardise US growth, but could also cause turbulence in the global markets through capital outflows from emerging markets like India and China, as they become less attractive to dollar investors.

Another aspect to be considered on the domestic front is that the US growth so far has been mainly because of strong consumer spending, which accounts for two- thirds of the economic activity. Business investments remain weak in 2016, albeit showing signs of improvement. Higher interest rates could adversely impact the already weak investment scenario.

It is indeed a difficult decision for the Fed. Domestic indicators such as the US labour market, inflation and housing market point towards a healthy US economy, which is well positioned for rate hikes in 2017. Global sentiments and outlook are also stable. However, consistent US dollar strengthening remains a concern for the US and it could result in the Fed toning down its aggressive stance on rate hikes. Moreover, global concerns in the form of a slowdown and high debt in China may re-surface. Geopolitical tensions, the upcoming European elections (France and Germany) and the on-going Brexit talks are some of the other global threats. Hence, it may not be easy for the Fed to go ahead with three rate hikes as promised. We may at best get one or two rate hikes in 2017.

-Rajani Sinha

& Rutuja Morankar

The authors are corporate economists based in Mumbai. Views are personal