.")

It is incomprehensible to many that the central government has not substantially increased its insulting payout of Rs 500 to about 5 lakh migrant workers; it is important to recognise that there are around 400 lakh people who have been destabilised by the lockdown and are fighting hunger, and, in many cases, outright destitution. Support for business, which is obviously secondary at a time like this, has been a little more forthcoming, particularly from RBI, but still remains pretty meagre.

Many analysts—both social and corporate—have been recommending the Centre add another 5-6% of GDP as the minimum additional support, over and above the 0.8% already announced. State governments are also strapped since they, too, are largely out of fiscal space, and the Centre is holding up many dues; thus, NGOs have been picking up some of the slack, but all their efforts, worthy as they are, add up to just a drop in the bucket of need. Rather than depending on ‘giving’, which is, at the best of times, catch as catch can, what is needed is an institutionalised process to support the people and, of course, develop the nation.

The government doesn’t seem to have the skill (or, perhaps, the interest) in creating institutionalised process; nor does it understand that, rather than some kind of rajah, it is simply the custodian of the peoples’ money and its job is to distribute it in an even-handed fashion, according to need. And the need today is louder than it has been in certainly more than the 21 years that Modi feared we would lose if we did not lock down. He needs to open his heart, such as it is, and the government’s wallet to ensure that the dispossessed receive a steady monthly income of at least Rs 4,000-5,000 a month for three months, assuming the lockdown does not extend beyond that.

This will certainly push the budget deficit much higher, and it is clear that, like most countries, we will have to suffer continuing high deficits for years to come. In addition to tiding over the current trauma, India needs to invest substantially in health and education (in addition to infrastructure, of course) for the next several years. Contrary to the oft-stated belief that we are too poor to invest in these critical services, the truth is that we are poor because we haven’t invested in health and education over the decades.

Continuing high deficits will terrorise the rating agencies, which may frighten away portfolio investors, which, in turn, may result in even greater falls in equities and, indeed, the rupee. But that is the price we have to pay for years of heartless profligacy and poor planning and implementation.

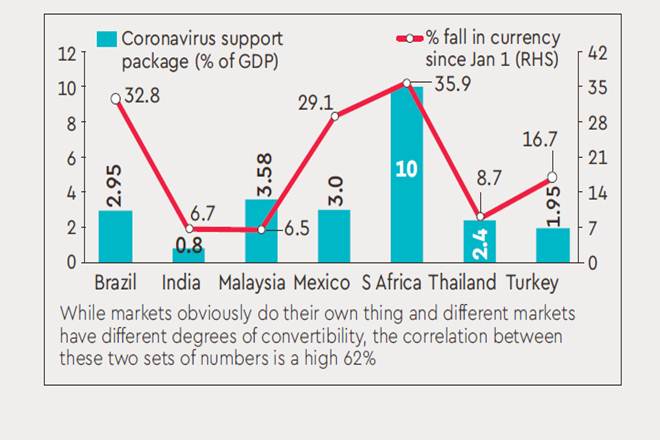

If the government were to follow FICCI’s recommendations and put out a package of 5-6% of GDP, with a focus on both the poor and the MSME sector, it is possible that the rupee may decline to, say, 85 or 90. (The accompanying table shows that several other emerging economies have already delivered significantly larger support to their people than we have and are living with much sharper declines in their currencies; 85 to the dollar would render the rupee’s decline at 19%, a bit more than Turkey but much less than Brazil, Mexico and South Africa.)

This would, of course, have its own impact on import costs and inflation, and loan repayments. Interest rates would rise and the equity market would shiver even more. On the other hand, it would make exports much more competitive, which would immeasurably assist in accelerating FDI, which is apparently searching for a new home (from China).

Since we are largely self-sufficient in foodgrains and most food items, the poor would be better off, which needs to be the number one priority. Equally, following up with meaningful investments in education and health could create a virtuous cycle, with healthier and better-trained employees, without which the Prime Minister’s now-near-defunct Make-in-India initiative would remain just another flashcard programme.

We need a changed government that uses our hearts as the starting point and our brains as the structuring/planning/implementing tool—we have to start building this now.

The author is CEO, Mecklai Financial. Views are personal