By Indranil Sen Gupta & Aastha Gudwani

We grow more confident of our call of 50bps of RBI rate cuts in 2020 after the FOMC cut 50bps Tuesday. Governor Das has told the media that “…we’re ready for a response should the situation warrant…”. While RBI is unlikely to respond right now, an immediate rate cut would reduce lending rates for SMEs before the ‘busy’ industrial season ends in March. We estimate that COVID-19 poses a 50bps risk to India’s 1H2020 growth if China’s slowdown deepens. In any case, at the core of the current slowdown, is a spike in real lending rates, in our view. Against this backdrop, we expect RBI MPC to cut a second 25bps in October/December after 25bps in June/August as inflation comes off. Global rates are falling with our US economists expecting the Fed to cut 25bps each in March and April. To pull down lending rates further (50bps in FY21 BofAe), we expect RBI MPC to infuse $45+bn of durable liquidity in FY21 atop $64.5 bn FYTD.

COVID-19 poses 50bps risk to 1H2020 growth

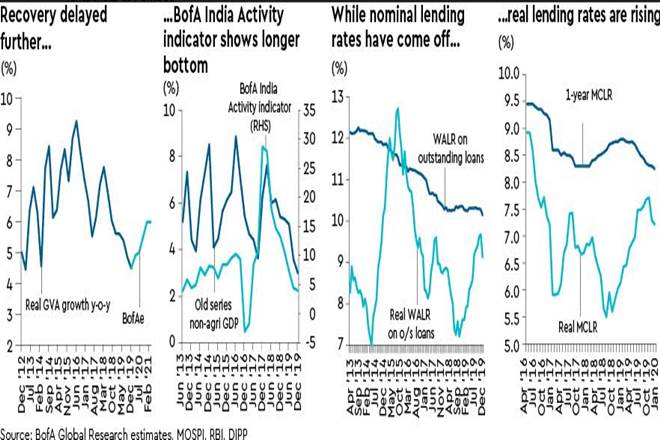

We monitor the effect of the slowdown in China, due to the COVID-19 outbreak, on India’s growth. We do not see much impact if China’s Q1FY20 GDP growth slows to our economists’ 4.2% forecast. However, if the situation were to worsen, we estimate India’s 1H2020 growth could drop about 50bps cumulatively on disruptions in China-India trade, including pharma/electronics input imports, as well as in global markets. As it is, we see India’s growth at an anaemic 4.9% in FY20 and 5.6% in FY21. Our BofA India Activity Indicator suggests that the worst is over—COVID-19 risks apart—but, at a deeper and longer bottom.

RBI has committed to “…monitoring global and domestic developments closely and continuously and stands ready to take appropriate actions to ensure orderly functioning of financial markets, maintain market confidence and preserve financial stability…”. At the heart of falling growth lies rising real lending rates, in our view (see graphic). Although nominal MCLR has fallen by 50+bps since March, on RBI easing, real lending rates have shot up 76bps on falling core WPI inflation. Against this backdrop, we expect the MoF/RBI to cut 50bps in FY21.

Two percent interest rate subsidy for a year to MSE. This will shield them from the real lending rate spike at the cost of 0.1% of GDP. Fed cut 50bps Tuesday; 25bps each in March and June. Our US economists expect the FOMC to cut 25bps each in March and April after Tuesday’s 50bps. Fed chairman Powell has assured that the Fed will use tools and act appropriately depending on the flow of events.

Sen Gupta is Chief India economist, and Gudwani is India economist, BofA Merrill Lynch. Views are personal

Edited excerpts from BofAML’s “India Economic Watch”

(dated March 4, 2019)