By Ashok Gulati and Manish K Prasad

As India assumes the G-20 presidency, one of the primary jobs under the finance track is to ensure that the G-20 nations come up with a credible policy framework to tame inflation, especially food inflation, while protecting growth and ensuring overall financial stability. The massive stimulus that was injected in almost all G-20 nations to circumvent the fear of recession during Covid-19 has come back to haunt the world in the form of excess liquidity causing inflation. On top of that, the Russia-Ukraine conflict has flared fuel and food prices, and climate change in the form of intense heat waves, floods, and droughts, is also hitting back on food prices in several countries. The central bankers of the G-20 have been on the job and are using monetary policy tools to douse inflation pressures. But the job is not yet done. The year 2023 will be a test case for the collective wisdom of the G-20 in taming inflation and protecting growth.

Also Read: G20 finance track meeting to start from Tuesday

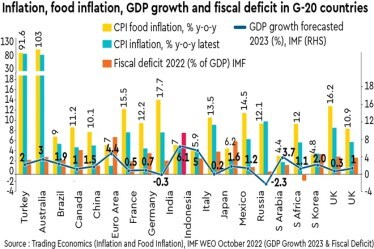

Look at Turkey, with food inflation surging at 103%, and Argentina, with food inflation at 91.6%. One wonders how they are controlling social unrest as the life-long savings of the people are being eroded with such high rates of inflation. Even in a country like Germany, food inflation, at 17.7%, is an unprecedented phenomenon in decades. India is in a much better position, with 7% food inflation, and the RBI Governor recently pronounced that the worst of inflation is behind us. Maybe it is time to appreciate RBI’s policy in managing inflation. The beauty is that India is taming inflation while recording the highest GDP growth—6.1% in 2023, as forecast by IMF’s World Economic Outlook in October 2022. In terms of GDP growth, China is likely to be at 4.4%, the US at 1%, the Euro area at 0.5%, and the UK at a meagre 0.3% (see graphics).

Incidentally, global growth is likely to tumble from 6% in 2021 to just 3.2% in 2022 and 2.7% in 2023. Advanced economies are likely to see even lower growth at only 2.4% and 1.1% in 2022 and 2023, respectively. Similarly, China’s growth has been downgraded to 3.2% in 2022 (the lowest growth in more than four decades, excluding 2020, when the pandemic broke, and a tad higher to 4.4% in 2023.

Against this global backdrop of inflation and growth, India can surely stand tall and may even give a lesson or two to the G-20 on how it has managed not to let food inflation spiral out of control and yet maintained the highest rate of GDP growth.

In this context, it may be noted that food inflation has been hurting not just the G-20 economies, but also many African nations, where purchasing power is very low. If India is to represent agenda of the Global South, one thing it must do is invite the African Union to the G-20. African nations are badly hit by food inflation for no fault of theirs and need support from the G-20.

Also Read: The CAG’s G20 opportunity

Interestingly, finance minister Nirmala Sitharaman, at a conference recently organised by ICRIER, had remarked that managing inflation with growth has to be done in a synchronised manner between RBI, ministry of finance, ministry of food, and many other ministries. It is like playing an orchestra with various policy tools to create a symphony. It can’t be done just by central bank alone. This is an important lesson that India can offer to the G-20 nations. But which policy instrument to play at what time, and at what volume, is an art of policy making that needs to be fleshed out clearly for others to follow.

However, there is no room for complacency even for India as we step into 2023. While our GDP growth prospects are the brightest, and inflation is under control (though still not below the upper tolerance band of RBI), our fiscal deficit at 9.9% (the Centre and states combined) is the highest amongst the G-20 countries. That’s not a sign of sound macro-economic management. The Fiscal Responsibility and Budget Management Act of 2003 (FRBM Act), which was passed by Parliament during the Vajpayee government, had envisioned bringing down fiscal deficit to 3% of GDP. That has remained a tall order for almost all governments since 2003. If Nirmala Sitharaman can bring down fiscal deficit of the Centre in a calibrated manner to somewhere between 3-4% in the next year or two without jeopardising growth, that would be a real feather in India’s cap when it comes to macro-economic management. It is not impossible, and can be done if efficiency in public expenditure is kept at a high priority.

The prime minister has recently been talking about staying away from ‘revdi’ (doles) culture. The issue has also attracted the attention of the Election Commission as well as the Supreme Court. Earlier, the Finance Commission, under the chairmanship of NK Singh, had flagged the growing culture of subsidies at the central and state levels. The time has come to bite the bullet on this. No one can deny the need for targeted subsidies to the most vulnerable, but the dole culture has gone far beyond that welfare objective and has become bait to win elections. It is this ‘bribe for votes’ that needs to be tamed. The best way to proceed is to set up a high-level committee of credible professionals to look into this and suggest ways and means to bring in frugality and efficiency in public expenditures of the Centre and the states, making it more growth-oriented, more jobs- and livelihood-creating, and more environment-protecting. If India can do that in a professional and pragmatic manner, it can surely lead the G-20 to a much more sustainable finance track!

Gulati is distinguished professor, and Prasad is researcher, ICRIER