")

By Shamna Thachaparamban

The allocation of tax revenue from the central government to states has become a subject of considerable debate. Karnataka and Kerala, two dynamic states in India with diverse economic contours, have experienced notable declines in their share of tax revenue from the Centre, sparking concerns and discussions about the underlying reasons and implications. Karnataka, often dubbed the ‘Silicon Valley of India’ due to its thriving IT industry and robust economic landscape, has witnessed a large decline in its tax share from the central government. Meanwhile, Kerala is renowned for its high human development indices and social welfare initiatives, which are even comparable to those of developed countries.

The 15th Finance Commission’s recommendations, based on various criteria including income distance, population, demographic change, fiscal capacity, area, and developmental needs, play a pivotal role in determining the distribution of tax revenue among states. For horizontal devolution, the Commission suggested 12.5% weightage to demographic performance, 45% to income distance, 15% each to population and area, 10% to forest and ecology, and 2.5% to tax and fiscal efforts. The share of states in the central taxes is recommended to be 41% for the 2021-26 period. However, cess and surcharge collected by the Union government are not included in the divisible pool and hence are not shared with the states.

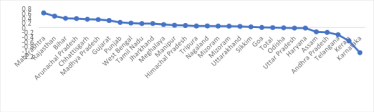

The economic significance of states notwithstanding, their contributions to the national GDP have not translated into proportional increases in their shares from the divisible pool. Notably, Karnataka, a significant contributor to the nation’s economy, has witnessed a reduction in its share from 4.71% in the 14th Finance Commission to 3.67% in the fifteenth FC. As a result, Karnataka might be losing out on its rightful share due to factors beyond its control. While Karnataka grapples with the discrepancy between its economic growth and intra-state disparities, Kerala faces challenges in reconciling its social welfare priorities with fiscal constraints. Despite its commendable achievements in healthcare and education, the state is facing an acute fiscal crunch. The state’s revenue sharply declined, falling to 1.925% in the 15th Finance Commission from 2.5% in the 14th Finance Commission.

Notably, the per capita GSDP of Karnataka has been on an upward trajectory, growing at a Compound Annual Growth Rate (CAGR) of 9.3 percent from FY15 to FY23, surpassing India’s per capita GDP. The case of Karnataka features the complex interplay between economic growth, regional disparities, and social inclusion. Meanwhile, Kerala, categorized as a “highly debt-stressed” state by the 15th Finance Commission and subject to study from the Reserve Bank of India (2022), requires urgent corrective measures.

The major reason for Karnataka and Kerala losing out is that their per capita income growth has been much faster than most other states, thereby reducing the income distance from the highest per capita income state (Haryana). In effect, taking income-adjusted distance, Kerala is treated as the first, followed by Karnataka. Even though in Karnataka, the increase in income coped with the decrease in population, whereas in Kerala, the decrease in population outweighs the increase in income. Based on the income distance criteria, the share of Karnataka is 1.093, while for Kerala it is 0.57. Kerala is a big loser in this concern, aggravated by rapid per capita income growth.

Addressing these disparities is crucial to fostering inclusive growth and upholding the principles of cooperative federalism in India. While the Finance Commission’s criteria aim to ensure equitable distribution, they must evolve to reflect the changing dynamics of state economies and their developmental priorities to ensure a fair distribution of resources among states. It is imperative an evaluation of the criteria for resource allocation, considering the principles of fiscal federalism and the specific needs of each state, or compensating by grants considering inter-state disparities or those which are considered highly meritorious.

Figure1. Difference in tax share (between 14th FC &15th FC)

The author is Assistant Professor at Gulati Institute of Finance and Taxation, Kerala.

(Disclaimer: Views expressed are personal and do not reflect the official position or policy of Financial Express Online. Reproducing this content without permission is prohibited.)