With 12-month forward premiums running over 3.5% per annum till as recently as June 2022, there was little enthusiasm amongst exporters for using options, particularly when the cost for buying an at-the-money forward (ATMF) option was in the range of 2.5-3%. ATMS (at-the-money-spot) options were cheaper at around 0.8-1%, but it still seemed like a lot of money to pay when 3.5% was available just of the asking (selling forward).

Of course, few exporters sell their entire exposure forward, partly because of business uncertainties and partly because…well, because most exporters still carry the belief that the rupee will always keep falling. To be sure, last year, the rupee did fall sharply, which burned most forward hedges, but markets are markets and we always have to guard against fighting last year’s battles.

With the forward premiums having come down substantially in the last year or so, and, importantly, with implied volatility also having fallen sharply, particularly over the past three or four months, option strategies appear to have come into their own for hedging exports.

But buying options is not that straightforward and, for an exporter, simply buying put options—whether ATMF or ATMS (at the money forward or spot, respectively)—doesn’t do the trick. The option premium to be paid ends up reducing the net value substantively, often rendering the option realisation rate below the Day 1 forward rate.

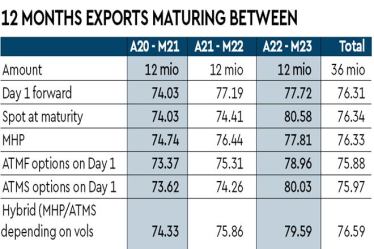

For 12-month exposures maturing between April 2020 and March 2023, ATMF options outperformed Day 1 forward just 36% of the time; ATMS options, which cost less, did, surprisingly, a bit better, beating Day 1 forward 42% of the time. (In general, with options, as in life, paying less will get you less value.)

On average, neither strategy was as attractive as MHP, our benchmark hedging programme. MHP, which uses no market view, uses only forwards, and follows pre-set hedging rules, outperformed ATMF options 65% of the time and ATMS options nearly 60% of the time. It was clearly a superior strategy over this period.

Indeed, it was marginally ahead of a 100% Day 1 forward hedge on average and, despite the sharp depreciation of the rupee in 22-23, was more or less on par with spot at maturity (SAM).

When considering options, it is also important to recognise that because the options market is not as liquid as spot USD-INR and option prices are not readily available to most corporates, banks often build in unconscionable charges onto the spreads they charge for options. The RBI appears asleep at the wheel on this; rather than demanding that banks provide customers with screenshots and calculations of pricing for options (and, indeed, all derivatives), it seems to prefer a hands-off approach. Thus, the actual performance of options strategies for most companies would very likely be worse than the numbers described above.

To address all these issues, we have recently developed a hybrid programme where we use puts when the implied volatility is below a particular cut-off (which is reflected in lower option premiums) and MHP when vols are higher.

The programme works reasonably well, in that it outperforms all the strategies mentioned earlier and even beats Day 1 forward (and, coincidentally, SAM) by close to 0.5%. To be sure, banks would squeeze you on the option price here as well but since the model used options only about a third of the time, the hit would be relatively modest.

There could be other option strategies that could be used but, as I already said, it is important to recognise that the more exotic the strategy, the worse is likely to be the hit at the bank interface. In general, we believe in keeping things simple, which is why MHP used only forwards; given the structural change both in the forward premiums and option prices, we feel it is the right time to introduce options into the mix.

Th author is CEO, Mecklai Financial

www.mecklai.com