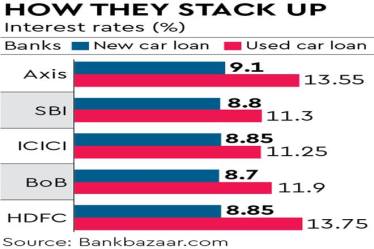

Buying a pre-owned or used car comes with several benefits as it is more affordable. While it is not difficult to finance your pre-owned car, there are certain factors you have to keep in mind to avoid any additional financial burden. The most important point: the interest rate on the loan for a pre-owned car is higher than that on a new car loan. It is, therefore, better to make a substantial down payment and opt for a loan with a shorter tenure.

Here’s a step-by-step guide to help you through the process.

Check your budget

Before you start looking for a loan to buy a pre-owned car, assess your financial situation and set a budget. Consider your monthly income, expenses, and existing financial commitments. Decide on the maximum amount you can comfortably allocate for your car loan instalment without straining your finances.

Check your credit score

Your credit score plays a crucial role in loan approval and the interest rate you receive. Check your credit score with credit bureaus like CIBIL, Equifax, or Experian. Adhil Shetty, CEO, Bankbazaar.com, says: “A good credit score (typically above 750) will enhance your chances of getting a loan with favourable terms. If your credit score is low, work on improving it before applying for a loan.”

Research Lenders

Banks, non-banking financial companies (NBFCs) and online lenders offer loans for used car. Compare their interest rates, loan terms, processing fees, and other charges. Look for lenders offering you competitive interest rates. Look for lenders offering you competitive interest rates.

Documentation

Lenders require specific documents to process your loan application. Generally, you’ll need identity proof (Aadhaar Card, PAN Card etc.), address proof, income proof (salary slips, IT returns, etc.), and bank statements. Prepare these documents in advance to speed up the loan application process.

Choose tenure carefully

Choose the loan tenure that best suits your financial situation. A shorter tenure will mean higher monthly instalments but lower overall interest payments. Conversely, a longer tenure will reduce monthly instalments but lead to higher interest costs over the loan term.

“One key factor you must know is that the interest rate is likely to be higher in the case of an old car loan. You must opt for the loan tenure carefully so that you don’t end up paying too much for an old car,” says Shetty.

Arrange Down Payment

While some lenders might give you up to 100% of the car’s value as a loan, it’s advisable to make a substantial down payment. A down payment of 15%-30% of the car’s value will improve your loan terms and reduce the burden of monthly instalments.

Applying For A Loan

Once you have taken all the steps mentioned above, proceed with your loan application. Many lenders offer online application options, making the process convenient and faster. Fill in the required details accurately, and attach the necessary documents as per the lender’s directions.

Approval and Disbursement

After reviewing your application, the lender will process your loan. If your application meets their criteria, they will approve the loan, and you will receive a loan offer. Carefully review the terms and conditions of the loan before accepting it. Once accepted, the loan amount will be disbursed to your bank account or provided through a cheque.

Purchase the Used Car

With the loan amount in hand, proceed to purchase the used car you desire. Ensure that all the necessary documents, including the car’s registration and transfer papers, are in order. It’s recommended to conduct a thorough inspection and get a trusted mechanic’s opinion before finalizing the purchase.

Get Ready for Repayment

Repay the loan in accordance with the agreed-upon terms. Set up automatic payments or reminders to avoid missing any instalments.

Shetty explains, “Timely repayment will keep your credit score intact and improve your financial credibility for future loans. One key factor you must know is that the interest rate is likely to be higher in the case of an old car loan. You must opt for the loan tenure carefully so that you don’t end up paying too much for an old car.”

These steps will help you manage your finances responsibly. Remember to consider the loan terms, interest rates, and your financial capability to ensure a smooth and stress-free experience.