Buying a new car is not only about getting the money in place or getting the loan. There are numerous choices that an individual needs to make when it comes to buying a car. Simply picking a model and brand of your choice is also not the only choice you have to make while buying a car. One of the first questions you have to face is whether you want to buy a new car or a used car. Opting for either of the options will make a huge difference to your finances. Additionally, if you are planning to opt for a loan, you need to find out whether you qualify for a loan or not.

Usually, companies offer 3 types of car loans – new car loans, used car loans, and loans against cars. One opts for a new car loan when purchasing a brand new car. The new car loans are offered at interest rates ranging from 8 per cent to 15 per cent per annum.

Used car loans are usually offered by banks and lenders when an individual opts for a second-hand or a used car. The rate of interest for these loans are slightly higher compared to new car loans. However, note that the loans against pre-owned cars are available for cars that are not older than 5 years.

Loan against a car, as the name suggests, can be opted for by keeping an old car as collateral with the bank.

Advantages and Disadvantages of a new car loan

Advantages: When it comes to taking a car loan, banks prefer to disburse loans for new cars because comparatively the risk is lower, while the loan amount disbursed is also higher. It is so because new cars come with a warranty from the manufacturer, hence, it reduces some work for the lenders.

In case of a new car, a borrower can get a loan for about 90 per cent of the cost of the car. Various banks also provide new car loans on the ‘on-road’ cost which reduces the burden of the borrower. At the same time, interest is also low.

The tenure of these loans usually range between 5 and 7 years, benefiting the borrowers who can manage their EMIs comfortably. The interest rate of new car loans ranges from 8 per cent onwards.

Disadvantages: When taking a loan to finance a new car, there are certain things to keep in mind. For instance, as there is an insurance premium attached to the new car, note that your annual cash outflow will rise. The total outflow will increase due to the insurance premium, even if the interest rate is low.

Advantages and Disadvantages of a Used Car Loan

Advantages: Most importantly, the cost of a used car will be lower than that of a new car. Hence, the cost of insurance for the borrower will also reduce. With an old car loan, not only the borrowing amount will be lower, but the repayment terms will also be flexible. Borrowers usually get a tenure of 4-5 years to make the repayment of the loan.

Disadvantages: In the case of a used car, the loan amount is usually limited to a maximum of 80 per cent of the value of the car. The rest of the money will have to be the borrower’s own down payment. With old car loans, the interest rate is also higher as compared to the new car loans. For instance, the interest rate ranges from around 10 per cent to 17 per cent, hence, the EMI burden will also be higher.

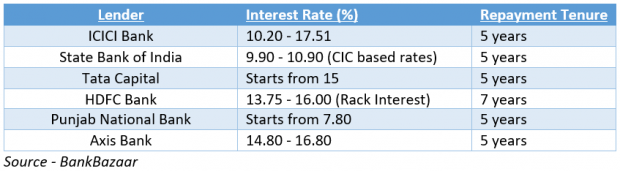

Pre-Owned Car Loan Interest Rates