The last date to furnish your income tax return is July 31, 2018. Thankfully, the Income Tax Department has provided the e-filing facility for all categories of ITRs. There are multiple ITR forms one has to choose from depending on the nature of one’s income.

For example, if you have earned income from salary combined with income from other sources, then you need to file ITR Form-1 (Sahaj). However, if your total income in the FY 2017-2018 had been more than Rs 50 lakh, then you can’t file ITR Form-1.

One noticeable thing is that ITR Form-1 (Sahaj) cannot be used in case the income of your spouse or a minor child, pertaining to capital gains, is to be clubbed with your income.

ALSO READ: What is the last date of filing Income Tax Return?

If you earn a salary but, in the previous year, you have income from capital gains/loss, short term or long term, then you are required to furnish your return using ITR-2.

Moreover, if you have income from one house property ( excluding cases where a loss is brought from the previous year) along with your salary income, then you are required to use ITR Form-1 (Sahaj). However, in the case of income from more than one house property, then file ITR Form 2.

Moreover, in a scenario where you earn income from salary and you are servicing a home loan for a self-occupied property, then you are required to file ITR Form 1 (Sahaj).

ALSO READ: 5 ways to e-verify your ITR

Let’s see how to file ITR-1 in this particular case:

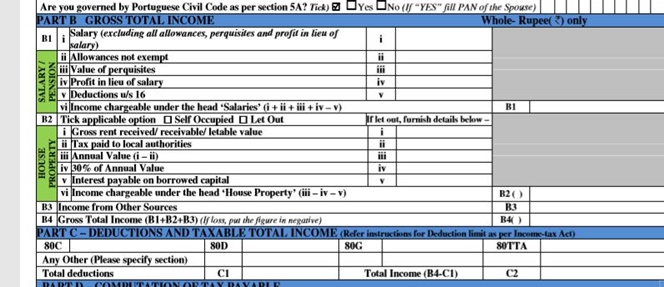

ITR Form 1 has five parts

PART A- General information like PAN number, name and Aadhaar number

PART B- Gross Total Income including your salary and home loan interest paid

PART C- Deductions and taxable total income

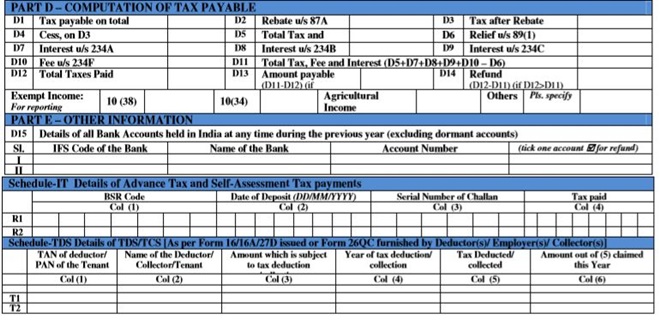

PART D- Computation of tax payable including cess, interest, fee, and rebate

PART E- Other Information like bank details like IFSC code, Account number etc

ALSO READ: What is Form 26AS? Why should you care about it?

Let’s see how to fill Part B of the form

Step 1- Enter the “income chargeable under the head salary” in the row B1. Take help from Form 16 to complete the procedure.

Step 2- In the row B2, tick on the Self-occupied box

Step 3- In the row B5, fill in the amount of the interest payable on borrowed capital. You can ask the bank or financial institution about the break-up of the principal and interest amount. The annual value of the self-occupied house is nil and the maximum deduction for interest paid on the home loan will be Rs 200000. Income chargeable under house property will be in a negative ( interest amount)

Step 4 – Fill in details of the income from other sources in the row B3. Your gross total income shall be the combination of B1+B2+B3= B4

Step 5 – In Part C, fill in details of your chapter VI deductions like 80C, 80D etc. It will appear in C1

Now, you shall have your total income which is B4- C1= C2

Part D – Your tax will be calculated in Part D

Words of caution:

Under Section 24(b), homeowners can claim a deduction of up to Rs 2 lakh on their home loan interest if the owner and his family reside in the house property. However, the loan must have been taken on or after 1 April 1999. The loan must be for the purchase and construction of the property. The purchase or construction must be completed within 3 years from the end of the financial year in which the loan is taken. The deduction is limited to Rs 30,000 in case of loan taken for repairs, renovation, and reconstruction of property.