Spurred by the various steps taken by the RBI and the government in recent months, the residential real estate in India has started showing signs of revival, which is visible from improvement in new launches and sales on a quarter-over-quarter basis.

According to a quarterly analysis of India’s eight prime residential markets by PropTiger.com, new units launched in Q3 2020 stood at 19,865 units, registering a YoY decline of 66 percent during the period between July and September 2020. However, on a quarterly comparison, new supply registered a growth of 58 percent in Q3 2020, as compared to the preceding quarter of April-June.

In line with the new supply, residential sales across the top eight cities have also started to show green shoots of recovery. The third quarter of 2020 saw primary residential sales to the tune of 35,132 units, registering a growth of 85 percent from the bottomed-out preceding quarter, which was heavily impacted by restrictive movement and uncertainty surrounding the global coronavirus pandemic. However, on a yearly comparison, demand registered a decline of 57 percent over the same period last year, with nearly 81,800 units sold in Q3 2019.

Amid the ongoing crisis, Mumbai and Pune continue to dominate sales with a share of 41 percent in the overall pie, followed by Bengaluru and NCR with 14 percent and 13 percent, respectively. All the top-eight cities witnessed an increase in sales as compared to the previous quarter, with Hyderabad and Ahmedabad leading the tally. A reduction in stamp duty by the Maharashtra government is being seen as one of the major catalysts in wooing prospective homebuyers to sign on the dotted line in the cities of Mumbai and Pune.

During Q3 2020, the demand in Hyderabad and Ahmedabad has more than doubled from the previous quarter, with nearly 6,600 units sold in these two cities in Q3 of 2020, as compared to 2,280 units in Q2’2020.

The third quarter saw maximum traction in the projects priced below Rs 45 lakh, with sales in the price bracket contributing nearly 45 percent to the overall demand pie in Q3 2020, followed by 28 percent in projects priced above Rs 75 lakh, as per the report.

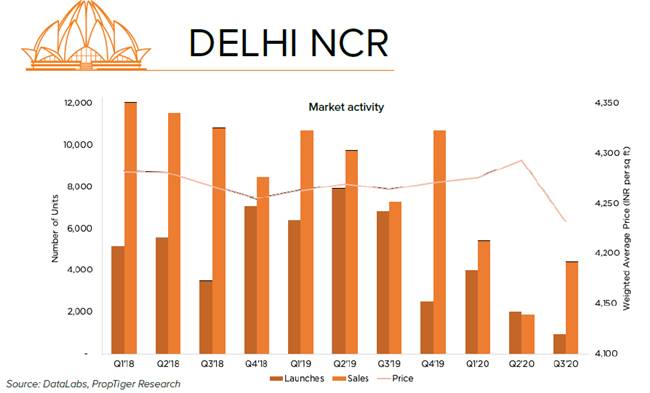

So far as Delhi NCR is concerned, new supply in Delhi NCR fell by a steep 86 percent on a YoY comparison, with a mere 940 new units launched during Q3 2020. While other metros, barring Bengaluru, saw a positive growth compared to previous quarters, Delhi NCR registered a degrowth of 53 percent. A majority of new supply was concentrated in Gurugram, followed by Ghaziabad.

The sales, however, are inching towards revival across Delhi NCR due to the on-going phased opening of economic activities. While sales declined by 39 percent on a YoY basis, they have more than doubled as compared to the previous quarter. Gurugram recorded a majority (59 percent) of sales, followed by Greater Noida with 13 percent share in the overall pie.

Commenting on this trend, Dhruv Agarwala, Group CEO, Housing.com, PropTiger.com & Makaan.com, said, “For the real estate sector, various steps taken by the Central bank and the Government of India have infused confidence and invigorated demand, which has been able to resuscitate the market from the bottomed-out second quarter of 2020. Corroborating the cues, our Virtual Residential Demand Index for September 2020 also indicates an uptick in interest levels for residential properties from the top eight cities, with the index spiking to 182 — overarching pre-COVID levels. As we head towards the festive season, the cues of revival and the historical low mortgage rates are expected to cushion sentiments and enliven residential demand.”