A financial emergency can knock on our doors anytime, and it can be challenging for anyone to handle that crisis without being financially affected. A personal loan is an unsecured debt which helps you avail funds based on your credit history, income and existing financial relationships with the lenders.

Personal loans are quickly available, and you can avail of funds as per your requirements and eligibility. These days you don’t even need to visit a bank physically. You can find many options for getting small funds in a day or two.

Because of flexibility of availing funds and easy approval process, personal loans have emerged as a popular financial product. Whether it’s for home improvement, or unexpected expenses, personal loans offer a convenient solution. However, like any financial product, personal loans come with their fair share of advantages and drawbacks. Let’s explore both the pros and cons of personal loans to help us make an informed decision.

The Pros:

Flexibility and Versatility

Personal loans are versatile, as borrowers can utilize the funds for various purposes. Whether you need to pay for medical bills, plan a wedding, or take a dream vacation, personal loans provide the freedom to use the funds as per your needs.

Also Read: How to save money effectively for short-term financial goals

Quick Access to Funds

Compared to other loan options, personal loans are relatively easy to obtain. Financial institutions and online lenders have simplified the application and approval process, allowing borrowers to access funds quickly. In many cases, you can receive the loan amount within a few days, which is particularly helpful during emergencies.

No Collateral Requirement

Personal loans are generally unsecured, meaning you don’t need to provide collateral such as your home or car as security. This eliminates the risk of losing valuable assets in case of loan default, making personal loans more accessible to a wider range of individuals.

Fixed Interest Rates

Most personal loans come with fixed interest rates, ensuring predictable monthly payments throughout the loan term. This stability can be advantageous when creating a budget and planning your finances, as you know exactly how much you need to repay each month.

The Cons

Interest Rates and Fees

While personal loans offer convenience, they often come with higher interest rates compared to secured loans. Borrowers with lower credit scores may face even higher rates, resulting in increased repayment costs. Additionally, some lenders may charge origination fees or prepayment penalties, which can further impact the overall loan cost.

Debt Accumulation

Personal loans can contribute to debt accumulation if not managed wisely. The accessibility and simplicity of personal loans may tempt borrowers to borrow more than they actually need, leading to unnecessary financial burden in the long run. It is crucial to borrow responsibly and avoid falling into a cycle of debt.

Impact on Credit Score

Taking on additional debt through a personal loan can affect your credit score. If you miss payments or fail to repay the loan on time, it can have a negative impact on your creditworthiness. It is essential to assess your repayment capabilities and ensure timely payments to maintain a healthy credit score.

Risk of Default

Since personal loans are unsecured, lenders rely solely on the borrower’s creditworthiness to determine loan approval. If a borrower faces unforeseen financial difficulties or loss of income, it may become challenging to repay the loan, resulting in default. Defaulting on a personal loan can have severe consequences, including legal action and damage to your credit profile.

Personal loans provide flexibility, quick approval, and the absence of collateral requirements. However, it’s important to consider the potential drawbacks. Before taking out a personal loan, carefully assess your financial situation, repayment capability, and explore alternatives if available. By understanding the pros and cons, personal loans can be a valuable tool for financial flexibility.

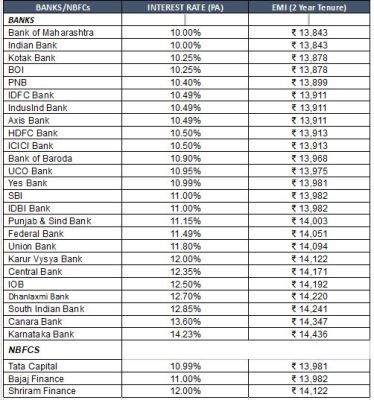

The table below compares interest rates of multiple banks and EMIs on a Rs 3-lakh loan for a 2-year tenure. It can help you compare interest rates and take a decision based on your financial needs.

Personal Loan Interest Rates & EMIs for Rs 3-Lakh Loan for 2-Year Tenure

Compiled by BankBazaar.com

Note: Interest rate on Personal Loan for all listed (BSE) Public & Pvt Banks and selected NBFCs considered for data compilation. Banks for which data is not available on their website are not considered. Data collected from respective institution’s website as on 27 June 2023. Banks and NBFCs are listed in ascending order on the basis of interest rate in their respective category, i.e. bank offering lowest interest rate on Personal loan is placed at top and highest at the bottom. EMI is calculated on the basis of interest rate mentioned in the table for Rs 3 Lakh Loan with a tenure of 2 years (processing and other charges are assumed to be zero for EMI calculation). Interest and charges mentioned in the table are indicative and may vary depending on the banks’ T&C.