The National Pension System (NPS), launched in 2009 on a voluntary basis for citizens above 18, has been a popular savings-cum-retirement plan in India. With the NPS, one can build a large corpus with small monthly savings.

Over the last one decade or so, more and more people from the organised and unorganised sectors have subscribed the NPS, reflecting growing seriousness towards retirement planning. They have started giving retirement planning top priority in today’s time. Employed people often think about how they can arrange a safe and stable income, so that financial independence remains even after the age of 60. Keeping this need in mind, the government started the NPS. It is a long-term investment option, which not only gives market-linked returns, but also guarantees pension after retirement.

NPS rules clearly state that once the scheme matures when the subscriber retires at the age of 60, it is mandatory for the person to invest at least 40% of the corpus in an annuity scheme. This annuity gives monthly pension in future. At the same time, the remaining 60% can be withdrawn by the person as a lump sum. However, if the total corpus is less than Rs 5 lakh, there is also an exemption to withdraw the entire amount. This is the reason why NPS is considered more attractive than traditional savings schemes.

Investment from the age of 25: Rs 5,000 every month

Suppose a person starts a job at the age of 25 and decides that he will invest Rs 5,000 every month in NPS Tier-1 account. He continues this investment for 35 years continuously, i.e. till the age of 60.

NPS is a market-linked product and its average return in the long term has been between 8-10%. Here we are doing the calculation assuming a 10% annual return.

How much corpus will be available on retirement?

If you do a SIP of Rs 5,000 for 35 years, the total investment amount will be:

5,000 × 12 × 35 = Rs 21 lakh (approx.)

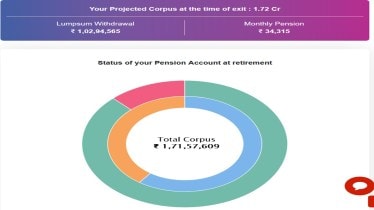

But due to compounding and 10% annual return, this amount will increase to – Rs 1.72 crore (approx.)

That is, by saving just Rs 5,000 per month, a person can become a crorepati by the age of 60.

Division of corpus: How much lump sum and how much pension?

As per NPS rules:

It is mandatory to invest 40% of the corpus in annuity.

The remaining 60% amount can be withdrawn as a lump sum.

According to this:

Will go into annuity: Rs 68.63 lakh (approx.)

Lump sum withdrawal: Rs 1.03 crore (approx.)

Calculation of monthly pension under NPS

Now let’s see how much monthly pension will be generated by investing Rs 68.63 lakh in annuity.

We assume that annuity will give an average annual return of 6%.

Annual pension = Rs 68.63 lakh × 6% = Rs 4.12 lakh

Monthly pension = Rs 4.12 lakh ÷ 12 = Rs 34,315 (approx.)

That is, this investor will get a lifetime pension of about Rs 34,315 every month.

Source: NPS Trust

Information about NPS Tier-1 and Tier-2 accounts

Tier-1 account: This is the main retirement account. It offers tax benefits and strict rules apply on withdrawal.

Tier-2 account: This is a voluntary account in which the investor can withdraw money anytime. There is no tax benefit in this, but there is more liquidity.

Tier-1 account is more effective for retirement planning as it maintains long-term discipline and also provides tax exemption.

Benefits of NPS investment

Long-term compounding benefit – The sooner you start investing, the bigger the corpus will be.

Tax exemption – Additional deduction of up to Rs 50,000 is available under section 80CCD (1B), under the Old Tax Regime.

Secure retirement – Guaranteed lifelong pension through annuity.

Flexibility – Facility to choose investment between equity and debt.

Summing up…

If a person starts investing in NPS at the age of 25 and invests just Rs 5,000 per month for 60 years, he will get a corpus of about Rs 1.72 crore on retirement. Out of this, about Rs 1.03 crore will be received as lump sum and about Rs 34,315 every month as pension.

That is, NPS is not only a way to become a millionaire, but also ensures regular income after retirement. So if you are also serious about retirement, then start NPS as soon as possible and make your future secure.