By Sandeep Jhunjhunwala

As the Budget 2024 unfolded, all eyes were riveted towards the finance minister as she laid out the inaugural budget of the Government following the recent Lok Sabha elections. Among the multitude of macroeconomic and direct tax proposals, the capital gains taxation reforms emerged as particularly prominent. The rationalisation and simplification of the capital gains tax regime, a long-cherished aspiration of taxpayers, finally received the Finance Minister’s endorsement in this budget.

Significant strides have been undertaken to overhaul the capital gains tax regime, most notably through the unification of provisions related to the holding period, which has been reduced from a maximum of 36 months to a more streamlined 24 months.

Announcements in the budget speech slashing tax rates for long-term capital gains to 12.5 percent across all asset categories, increasing the exemption threshold for long-term capital gains from the transfer of listed equity shares, equity-oriented funds, and business trusts from INR 1 lakh to INR 1.25 lakhs, seemingly add luster to the Government’s tax proposals, masquerading realities muddled in the fine print.

The proposal, dressed in the guise of simplification, may paradoxically amplify the tax burden for many, dampening the initial enthusiasm surrounding these changes.

Significant concerns arise from the proposal, including an increase in the tax rate for short-term capital gains on the transfer of listed equity shares, units of equity-oriented funds, or units of business trusts from 15 percent to 20 percent. The increase in long-term capital gains tax by 2.5 percent in listed financial assets, is a possible step to mop up direct tax resources from around 148 million demat account holders, which is in sharp contrast to around 21 million taxpayers, paying income taxes in India.

Additionally, removing indexation benefits for unlisted securities and other non-financial assets, such as real estate, could have apprehensible repercussions for taxpayers. Assessing whether the reduction in the tax rate compensates for the loss of benefit of inflationary adjustment is a fact-specific exercise that could be a door chime for a few and yet a signal of distress for a few others depending on the statistical nuances involved.

A larger ramification that could flow due to this proposed amendment is more money channelising to the capital markets due to better returns. Although the fine print does not indicate any changes, a post-budget press conference revealed that the Finance Secretary has assured that the indexation benefit applicable until 2001 would remain grandfathered. Nevertheless, a definitive validation awaits the incorporation of these changes into the Finance Act.

Addressing concerns highlighted in the Economic Survey, the proposal envisages an increase in the Securities Transaction Tax (STT) on futures trading from 0.0625 percent to 0.1 percent and on options trading from 0.0125 percent to 0.02 percent. This adjustment appears to be a deliberate attempt to deter investors from engaging in the derivatives market.

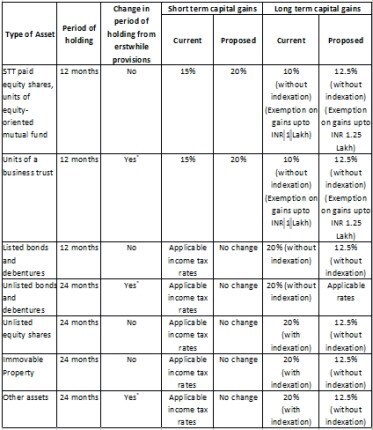

To summarize, the table below delineates the overarching implications of the proposed changes to capital gains taxation across various asset classes:

*The erstwhile period of holding was 36 months

Overall, the proposed reforms to capital gains taxation signify a profound, though complex, transformation in the Indian income tax landscape. As stakeholders await the official enactment of these changes, subtle intricacies revealed in the fine print highlight the necessity for meticulous analysis and strategic foresight. These modifications have the potential to fundamentally alter investment strategies and tax planning, underscoring the need for a deliberate and informed approach to adeptly navigate the evolving tax framework.

(Author is Partner, Nangia Andersen LLP and Amita Jivrajani, Director Nangia Andersen LLP with inputs from Sravani Raghuram, Nangia Andersen LLP)

Disclaimer: Views expressed are personal and do not reflect the official position or policy of FinancialExpress.com. Reproducing this content without permission is prohibited.