")

The narrative around global investing is often built around stories. Investors weave these stories around cycles, themes, and opportunities to justify and support their investment rationale.

When these stories are simple and the rationale is sound, they can benefit investors.

However, investment bankers and asset managers, often make straightforward strategies appear complex to justify their fees and expertise. You’ll frequently encounter mnemonics or catchy phrases explaining investment rationales. My advice: when an investment rationale becomes a ‘theme’ or a ‘meme’, it’s time to be cautious about the risks and expected returns.

I’m not referring to classic ‘bubbles like ‘Tulip Mania’, or the ‘dotcom’ bubble. These were speculative frenzies which led to dramatic gains and sudden crashes.

Instead, I’m focusing on the positives and negatives of theme-based investing.

The allure and pitfalls of thematic investing

Consider the current global theme: Artificial Intelligence (AI). Many call it a ‘mega trend’—one that could shape investment outcomes for decades. Investors are chasing the AI theme by allocating capital to companies, sectors, and countries poised to benefit from the AI boom. Conversely, those not aligned with the AI narrative are seeing capital outflows.

“India is Not AI” Narrative

This article is prompted by a recent theme I’ve seen applied to India:

‘India is Not AI’ – a phrase used in a research report to explain India’s current underperformance relative to China, Korea, Taiwan etc.

Foreign investors are pulling capital from India and reallocating it to markets perceived as AI beneficiaries.

(Dear readers, you may like to read two previous editions of the Global India Insights – Foreign Investors are Exiting India and The Great India Under-Allocation, to understand the context of these outflows and how foreign investors invest in India)

This argument holds weight from an ‘AI theme investing’ perspective. India hasn’t developed foundational Large Language Models (LLMs), nor does it design or manufacture high-end semiconductor chips for generative AI. There’s no AI-driven data center boom, and India’s large IT services sector could be threatened by widespread AI adoption. Investors chasing the AI story are logically allocating to the US, China, Korea, and Taiwan—markets leading the AI-driven boom.

As investors who trend follow theme driven investing, the above trade seems logical. However, the hype often leads to over-valuation and misallocation of capital. We have seen over time, that some investing themes dissipate, as investors rotate out and move to other stories and investing themes which find favour.

Thematic investing is best suited for tactical, short-term allocations and requires deep expertise to execute well. It may be profitable, but it’s difficult to replicate across cycles.

In contrast, strategic allocation—by its long-term nature—should be simple, predictable, and replicable. As I’ve argued in this Global India Insights series, India is not just a theme; it’s a strategic, long-term allocation that is both simple and predictable.

Themes change, India endures: A historical view

Over the past 25 years, India investing has been assigned many themes, both positive and negative:

- In 2003, Goldman Sachs included India in ‘BRIC’.

- In 2013, Morgan Stanley labeled India as part of the ‘Fragile Five’.

- In 2014, PM Modi’s victory elevated India to ‘TINA’ (There Is No Alternative).

- In 2019/20, Xi Jinping’s domestic policies led to the ‘China + 1’ narrative.

- In 2024, India’s lack of high technology and AI has led to the ‘Not AI’ theme.

Despite these shifting narratives, India investing has thrived and survived. The real change during these periods is in investors’ expectations and outcomes.

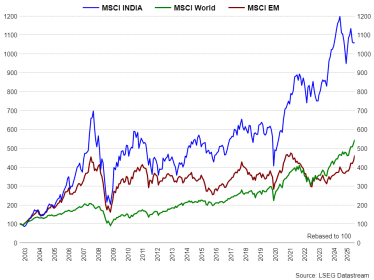

However, India investing has thrived and survived these investing mood swings. This chart below is a testament to the long-term case of India being a simple, strategic, long-term allocation.

The real change during these periods is in investors’ expectations and outcomes.

(Source: All data in USD, Rebased to 100 in 2003, Data till September 2025)

Lessons from past themes (BRIC, TINA, China+1)

For instance, India was grouped as part of ‘BRIC’ – Brazil, Russia, India and China – four emerging economies whom Goldman Sachs ‘dreamed’ as long-term growth engines into 2050.

It coincided with a global growth surge, and we found investors expecting India’s near-term real GDP growth of 8-9% to continue. India began receiving investment flows with return expectations based on that 8-9% real GDP growth rate. ‘BRIC’ Funds proliferated. Flows moved from large cap equity to mid and small cap stocks. A lot more capital was being committed to private equity in the hope of even higher returns. Long-term Investors chanced their luck began betting on tier 2/3 real estate and green field infrastructure.

The first shock to the “BRIC” thesis was the global financial crisis of 2008. By 2011-2012, as the growth fizzled out, many of these investors exited in the next few years frustrated with their outcomes and extorted, INDIA – I Will Never Do It Again!

A similar exuberance occurred from 2014-2017 under Prime Minister Modi’s ‘Ache Din’ (Good Days) campaign. The ‘There is no Alternative’ (TINA) narrative toom hold. to India. While I agree and have made the case for dedicated allocations to India, however I also caution on being realistic on your return and outcome expectations.

Stock markets rose on expectations and sentiment, but corporate earnings remained subdued. Growth settled closer to 6%, and thematic expectations were tempered.

The ‘China + 1’ narrative seemed real with some production shifting from China to other destinations for cost and geopolitical reasons. However, apart from Apple’s mobile assembly in India, most ‘China + 1’ capital inflows were in private equity and venture capital between 2019-2022 (read Foreign Investors are Rolling the Dice’). Meaningful manufacturing relocation has yet to materialize.

The ‘India is Not AI’ theme has merit—India lacks significant technological prowess outside of space research. When ChatGPT and other LLMs emerged, India had little to show. Generative AI chips are dominated by US, Taiwan, and Korea. China’s ‘DeepSeek’ open-source LLM has drawn global attention back to China’s R&D capabilities. In this AI-driven environment, investors have questioned India’s markets and valuations, leading to outflows and underperformance versus global and emerging markets.

However, as with previous themes, it’s important to maintain realistic expectations and outcomes. Investors should recognize that India is not a high-tech frontier. Instead, India offers consistent economic growth, reflected in corporate earnings, with businesses known for better governance and superior return ratios.

India’s unique investment case: Beyond the themes

India may lack advanced technology, critical natural resources, and perfect governance. But it offers a bottom-up, diverse economic story. Growth is broad-based, spanning multiple sectors and regions. This diversity ensures that the benefits of growth are widely distributed and reflected in the stock market.

The link between GDP growth → corporate revenues → profitability → stock market returns has held true for decades. I believe it will continue.

Conclusion: A sensible, strategic allocation

Investing in Indian public equities offers a simple, predictable way to participate in India’s growth story. Investors can maintain a realistic assessment of India and avoid being swayed by positive or negative themes and mnemonics.

Arvind Chari is a Chief Investment Strategist and has been with Quantum Advisors India group since 2004. Arvind has over 20 years of experience in long-term India investing across asset classes. Arvind is a thought leader and guides global investors on their India allocation.

This article is for educational and discussion purposes only and is not intended as an offer or solicitation for the purchase or sale of any investment in any jurisdiction. No advice is being offered nor recommendation given and any examples are purely for illustrative purposes. The views expressed contain information that has been derived from publicly available sources that have not been independently verified. No representation or warranty is made as to the accuracy, completeness, or reliability of the information.

The views and opinions expressed in this article are my personal views and should not be construed of the Firm. There is no assurance or guarantee that the historical result is indicative of future results, and the future looking statements are inherently uncertain and cannot assure that the results or developments anticipated will be realized.