“Investment is an Act of Faith – Manmohan Singh, July 1991.”

The United States of America is a global hegemon – a dominant and leading power. It is referred so because of its military dominance and economic strength which allows it control over the international system.

Since the end of the second world war, the US has emerged as the largest economy in the world. It is also the most prosperous amongst the large economies when measured through per-capita income.

The US has been on the forefront of education, innovation, and entrepreneurship. It embraced and advocated free trade and has become the largest bilateral trade partner for many countries. The US Dollar is the global reserve currency of the world, and the US thus has an open capital account. This means that US attracts lot of capital into the country for its businesses and financial markets. The US corporations and financial investors are also large providers of capital to the rest of the word.

It is also remarkable that the US has a median population age below that of other advanced economies due to a conscious immigration system. The allure of the American life and opportunity attracts the brightest students, the best talent, and families from around the world to build their American dream.

It is the democracy, the freedom and liberty of thought and expression, the rule of law and the strength of its institutions which combine to make America a true leader of the global free world.

These attributes build a level of trust in committing capital and investing in America, its economy, its businesses, and in its markets.

The private capitalist system and the institutional framework has enabled the creation of deep and liquid markets for finance and investing. The US has the largest equity and fixed income market in the world. It hosts the biggest commodity trading markets. The US commands more than 50% share of global private equity, private credit, venture capital, real estate, and infrastructure investments. US companies form the highest share of the Global Fortune 500 companies.

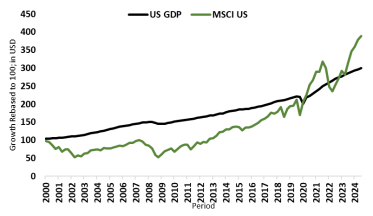

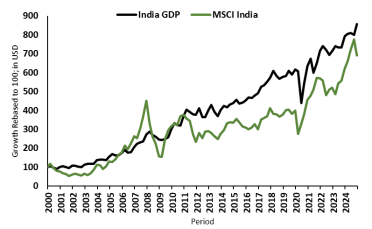

And investing in America has been successful as evidenced in the chart below on the reflection of US GDP growth with the returns in its stock market.

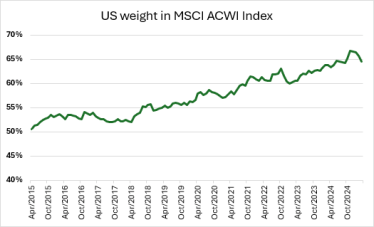

It has been a ‘no-brainer’ to invest in the US stock markets, especially so in the last 15 years. The ‘US exceptionalism’ as many have termed its success, was reflected in its stock markets. US companies, driven by its technology giants, became a major share of global portfolios and indices. The US stock markets now have a ~65% weight in the MSCI All Country world Index up from 50% in 2015 and 40% in mid 2000s.

Foreign Investors own US$ 31 trillion of US securities (~US$17 trillion of Public Equities; and ~US$14 trillion of US Debt). (Data as of June 2024).

Of this, European investors own ~ USD 9 trillion of US equities and debt. UK investors own ~USD 3 trillion. Canada and Japan own USD 2.5 trillion, China owns USD 1.4 trillion, and the Oil exporters own USD 1 trillion. India owns USD 260 billion, predominantly US Debt

If seen, as official holdings by foreign governments as part of their foreign exchange reserves, USD 6.5 trillion out of USD 31 trillion is owned by foreign official sources)

Furthermore, we can assume that of the ~US$ 13 trillion of global private and alternatives capital, 60% (~US$8trillion) is invested in the US.

So, foreign investors possibly own ~US$ 39 trillion (31+8) worth of US assets. This mostly excludes real estate holdings of foreign individuals.

| Foreign Investments in US | ||

| Foreign Investments in Public Markets * | USD 31 trillion | |

| of which: US Equities (USD 17 trillion) US Bonds (USD 14 trillion) | ||

| Foreign Investments in US Private and Real Assets (^60% of US$13 Trillion) | USD 8 trillion | |

| Total Foreign Investments in US (which may not include US real estate owned by foreign individuals) | USD 39 trillion | |

US has a ~26% share of global GDP. When adjusted for Purchasing Power Parity (PPP), it’s share of global GDP is ~15%. US has a ~50% share of global stock market capitalisation. Thus, allocations to US will be a large share in many global portfolios,.

Global Investors will diversify their investments away from the US.

With trade wars and battle lines drawn, non-US owners of US assets face a risk not seen since President Roosevelt confiscated assets of the Japanese living in USA during World War 2 and President Nixon unlocked the doors of inflation by taking the US$ off the gold standard on August 15th, 1971, and set the foundation for unleashing untamed inflation internationally.

The problem is that ‘risk’ is, in a very narrow financial sense, only defined as standard deviation / volatility and currency movements.

Now there is the real ‘risk’ of permanent loss of capital by a Presidential directive – in any geography.

Will Canadians feel comfortable owning property in USA?

Will the European Pension Funds feel comfortable owning US treasuries and the S&P 500 Index?

Will a French company doing business with a Canadian company face the ire of a US government which sees that as bypassing tariffs?

Will Chinese government remain assured that their ownership of US treasury bonds will be honored?

Is it possible that an Administration, angry at the defiance emanating from certain allies, lashes out by placing a special tax on assets owned by a specific set of people? Or worse, outright confiscation?

Will foreign students feel safe and welcome to study in the US; Will foreigners travel on vacation to the US without fearing the risks and vagaries of the US immigration officer?

We don’t yet know whether President Trump’s tariff tantrums will yield the expected result or will the chaos lead to a significant shock to the US economy, business and markets.

What we do know though is that these actions over the last six months is a “Reset’ of the ‘Trust’ A Trust that everybody had on US ‘rule of law’, and the intentions and actions of the US government.

I am not questioning the US exceptionalism. All that I mentioned in my opening paragraph about US remains true. The US will remain the leader in technology and innovation. The US stock markets may continue its outperformance. The US dollar may also retain its reserve currency status.

However, this may not be a question of returns and opportunity. This is now a function of risk.

Global governments and investors, especially those directly impacted by the US administration remonstrations on Tariff, Military Security, Immigration, Spending, etc will relook at their investments and dependence on the US.

Will global corporations do the same as well? Will they re-orient some of their business, investments, strategies away from the US? Can they afford to do so, given the size and the opportunities in the US economy? Will they be forced by their governments to retaliate against US?

Will they sell some of their US investments?

Even if the global financial investors sell 10% of their outstanding US investments, that is ~USD 4 trillion in outflows from US markets. (10% of USD 39 trillion).

This is itself would be a significant re-balancing. A re-balancing of risk, and trust.

How will US investors react? An average US household, their 401K investments and their public pension funds will also have significant home bias and thus higher allocation to the US. This has worked well in terms of financial returns over the last 15 years as evidenced by the charts above. For US domestic investors, this still remains a function of returns and opportunity.

However, would they perceive the change in America’s tariff and immigration policies to be a big shock to the system which would impact financial returns. If so, will they diversify some of their allocation away from US.? We saw this diversification in the decade of 2000s, when investors allocated away from US to Emerging Markets, BRIC – (Brazil, Russia, India, China), Asia. This spawned a major rally in emerging market assets – equities, bonds and currency. Are we likely to witness a similar trend over the next 1-3-5 years?

In a follow-up piece, I will look at these probable trends from an investors perspective.

If this is indeed a Global Reset, it will lead to re-balance. A re-balance of geo-politics. A re-balance of military and security dependence. A re-balance of Trust. A re-balance of Trade. A re-balance of Investments.

In this Global India Insights series, I will focus on the investment implications of these global trends and its likely impact on India.

In a follow-up piece, I will look at this global re-balancing of investments.

Will all investors be nationalistic and become more home-biased? Will some of these investments be allocated to other ‘friendly’ countries? Does India stand a chance to benefit from this re-balancing away from US?

Look forward to it.

Disclaimer

Note: The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Arvind Chari is a Chief Investment Strategist and has been with Quantum Advisors India group since 2004. Arvind has over 20 years of experience in long-term India investing across asset classes. Arvind is a thought leader and guides global investors on their India allocation.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.