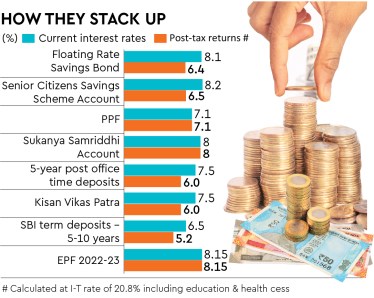

While the Reserve Bank of India (RBI) has increased the interest rate of Floating Rate Savings Bonds (FRSBs) to 8.1% (October 30, 2023 to April 29, 2024) and has also enabled subscription through its Retail Direct Portal, a web-based platform for investing in government securities, risk-averse investors should note that such bonds are more attractive in a rising interest rate environment.

Experts say investors must keep in mind that we are at the peak interest rate which is likely to come down once the inflation outlook improves. So, when interest rates fall, the coupon of FRSBs will also come down. In such a case, locking at current bank fixed deposits or small savings would be more attractive over an investing period of five years.

The FRSBs have a tenure of seven years and the interest payout frequency is half-yearly. While the minimum investment amount is Rs 1,000, there is no upper limit of investment in these bonds. The returns are fully taxable as per the individual’s marginal tax rate. The coupon will keep varying during the tenure and will be fixed based on the rate of interest of National Savings Certificates (NSC) plus a spread of 0.35%.

Peaking of interest rates

Adhil Shetty, CEO, Bankbazaar.com, says the FRSB offers assured returns, capital protection and the sovereign guarantee is attractive. “However, in the current environment, a peaking of interest rates will be followed by a fall in rates. Therefore, the returns on NSC and by extension FRSB will fall as well in the near future. If you are a senior citizen you could lock into a 7.5 to 8% fixed deposit for an assured return of a similar time-frame.”

Similarly, Sushil Jain, CEO, PersonalCFO.in, a wealth management firm, says investors should lock in at high rates for the long run in bank deposits. “In floating rate, you will enjoy the high interest rate for a short term only as we are not expecting an increase in interest rate in the long run,” he says. Keep in mind that there is no exit option from these bonds before maturity, except for senior citizens aged 60 and above. These bonds cannot be used as collateral for loans from banks, financial institutions, or non-banking companies and are not tradable or transferable.

Other attractive fixed income options

As interest rates have peaked, risk-averse investors should look at various fixed income instruments to lock in to the longest available tenure at peak rates. Investors can also look at special FDs launched by banks. However, these schemes do not allow premature withdrawal facility and some banks may also set higher minimum deposit amounts for their special FD schemes. Banks are offering interest rates ranging between 6.5 to 8% for 5-year fixed deposits and post office 5-year time deposit is offering 7.5%.

For senior citizens, small finance banks are offering interest rates of up to 8.6%. In fact, the Senior Citizens Savings Scheme Account is an attractive option offering 8.2%. A senior citizen (above 60 years) can invest up to Rs 30 lakh, the lock-in period is for five years and can be extended only once for three years.

Salaried employees contributing to Employees’ Provident Fund (EPF) can opt for additional voluntary contributions to EPF to earn tax-free returns of 8.15%. Contributions of up to 100% of the basic salary and dearness allowance can be made to VPF.