With the new CEO taking the bull by the horns and announcing sweeping changes in accounting transparency, governance, compliance and business mix, we are one of the many who are enthused with what he had to say post Q4 earnings. However, after looking at the numbers and factoring in the management’s guidance, we believe the road to a new way of doing things will be long and arduous as the disruption is not only at the asset-quality level but also at the fee line as well as on operating costs level.

Unless investors wish to give a significantly higher multiple for a long-term RoE potential (over 5 years), we expect the stock to see a suppressed multiple range of ~1-1.5x in the interim, leading to our TP of Rs 197, implying a 17% correction from current levels and our consequent downgrade to Sell from our Buy rating.

Q4 operating surprises and trends

Strong momentum in consumer loans (up 64% y-o-y) was offset by the continued sharp correction in corporate growth to 15% leading to an overall 18% loan growth (above industry averages). Management’s target is to bring down corporate-retail mix from 66-34 to 50-50 over the next 5-7 years, thus, reducing the risk tendency of the book. Deposit growth, too, decelerated keeping pace with loan growth. However, CASA mix remained healthy at 33% leading to NIMs that would have remained flattish but for an interest income reversal of Rs 1 bn on account of slippages. Fee growth collapsed—reporting a second successive quarter of a y-o-y decline (63% down y-o-y) led by corporate banking fees and financial market fees. The cost-assets ratio ticked up as the bank goes on hiring mode. Thus, pre-provisioning profits were down 38% y-o-y.

Asset quality summary

The bank made a not entirely unexpected contingency provision in Q4. However, the quantum was larger than expected at Rs 21 bn on a stressed asset base of Rs 100 bn in an effort to provide proactively for FY20e. This book of stressed, but standard exposures of Rs 100 bn comprises 6-7 accounts. Their airline exposure has already been recognised as an NPL. There is another approximately Rs 100 bn remaining under the BB & below category which will be closely watched for signs of stress. This quarter saw fairly high slippages of 5.8% vs under 3% for 9MFY19. Credit costs including contingency provisioning shot up to 550bps (annualised).

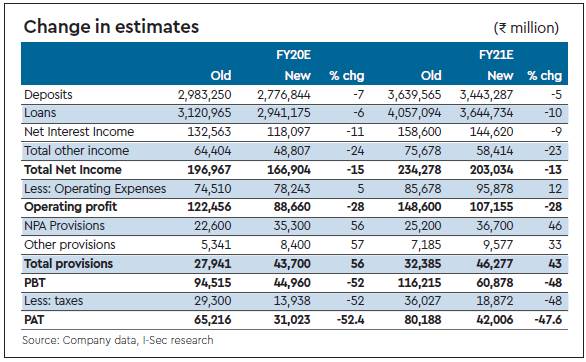

Revisions to earnings estimates

Given multiple pressure points across revenues, costs and asset quality, we take a steep cut to our earlier estimates by 52% and 48% in FY20e and FY21e, respectively, pulling down RoA to 75bps and 85bps, accordingly. We factor in a $1 bn equity raising in FY20e at current market price resulting in a 13% dilution and an ABV of Rs 154 per share in FY21e.

Valuations and target price

With management targeting a 1% exit RoA in FY21 and 1.5% in the years following that, we value the stock on a 13% RoE which would be the RoE under a 1% RoA scenario with max possible leverage considering their 83% RWA/assets ratio. This results in our revised TP of Rs 197 implying a target P/ABV multiple of 1.3x. Accordingly, we downgrade the stock from our earlier BUY rating to Sell rating.