United Spirits (USL) has been our key anti-consensus ‘REDUCE’ call (20% ‘REDUCE’ on Street vs 80% ‘BUY/HOLD’). The stock has underperformed the FMCG Nifty by 25% since its peak in mid-February and is down 26% thereof. This was also due to low visibility on its delisting. Diageo Plc has taken a write-down of GBP772 mn for the Indian market, recognising the impact of Covid-19.

That said, with USL’s underperformance behind, we are upgrading the stock to Hold with a revised TP of Rs 545 on the back of: (i) normalcy returning to outlets and factories; (ii) worst for out-of-home consumption behind; (iii) greater clarity on pricing and taxation—with huge tax hikes in Delhi and Odisha rolled back and company receiving hikes in 7–8 states; (iv) a shift from beer to spirits; (v) sequentially benign raw material prices; and (vi) potentially positive levers in home delivery from a long-term standpoint.

Normalcy back in manufacturing and opening of outlets: Manufacturing and sale of alcoholic beverages was banned from 24th March to 4th May, which dragged USL’s volumes 49.2% y-o-y. By the end of June, all manufacturing units had become operational; by mid-August about 90% off-trade outlets had opened up.

Exorbitant taxes rolled back: Huge tax hikes (70–75% of MRP) levied by Delhi and Odisha have been rolled back, and USL is working with other states that had raised taxes due to Covid-19.

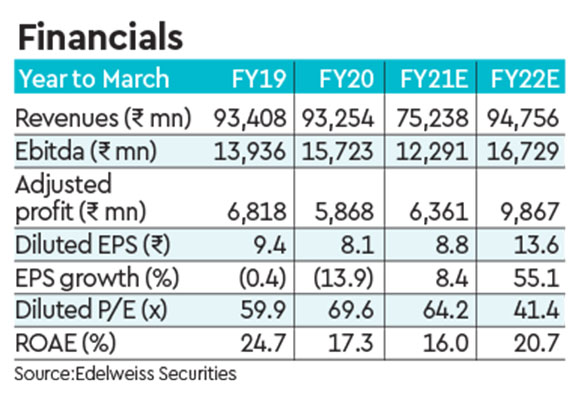

Outlook: Worst is behind firm—Mgmt’s efforts to enhance productivity and premiumisation are on track, in spite of macro and political disturbances. Although Covid-19 has presented challenges, it has also uncorked a positive development—online delivery, which can be a significant structural positive for the industry. Hence, we upgrade to ‘HOLD/SP’. The stock is trading at 41.4x FY22e EPS.