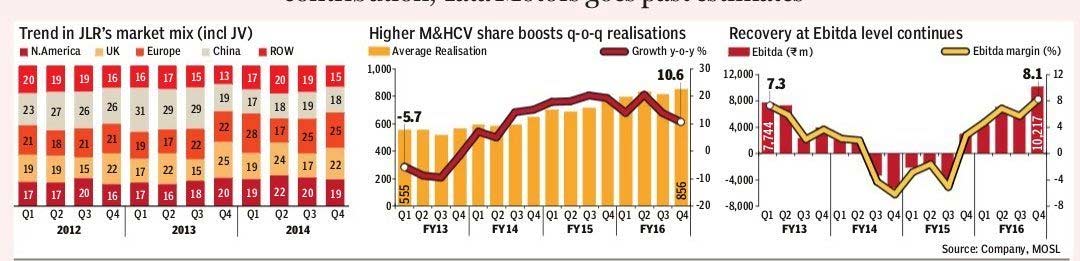

Consol sales at R807 bn (v/s R732 bn; +19% y-o-y). Ebitda at R113.8 bn (v/s est R91.5 bn; +35% y-o-y). Adj. PAT at R47 bn (v/s est R39.5 bn; +158% y-o-y): JLR realisation at £44k (v/s est £42k) grew 5% q-o-q due to better product mix. Adj. Ebitda margins of 16.2% (v/s est 14.2%), were driven by higher volumes and favourable mix. Further, higher share in Chery Automobiles joint venture PAT (£49m) and lower tax boosted adj. PAT to £560m (v/s est £368m), up 30%. S/A realisation grew 5% q-o-q (+10.6% y-o-y) to £856k/unit (v/s est. £865k) driven by higher M&HCV contribution. Ebitda margins at 8.1% (v/s est 8.3%), up 240 bp q-o-q, were driven by product mix and operating leverage. Higher other income and higher tax credit boosted adj. PAT to R5 bn (v/s est R617m).

Earnings call highlights:

(i) JLR’s product lifecycle is on track with F-Pace launch starting Apr-16, XE in US in May-16 and XFL in China in 2HCY16. (ii) Despite stable q-o-q volumes, share in Chery JV PAT grew to £49m (v/s £22m in Q3FY16). (iii) Provided £67m for airbag related recall in the US. (iv) JLR generated FCF of £1.4 bn in Q4FY16 and £743m for FY16. (v) Capex guidance for FY17 for JLR at £3.75 bn (v/s £3.13bn in FY16) and India business at R35-40 bn. (vi) Turned net cash at consol level with net cash of R6.8 bn (v/s R133.9 bn net debt in Q3FY16). S/A net debt reduced to R137 bn (v/s R151 bn in Q3FY16).

Valuation & view: We raise our EPS for FY17/18 by 7%/2%. The stock trades at 9.2x/7.3x FY17/18e consol EPS. Maintain Buy with TP of R524 (FY17 SOTP based).

JLR: Higher volumes and better mix drives strong performance

JLR’s (ex Chery JV) wholesale volumes were up 20% y-o-y (+9% q-o-q) to 149,895 units (v/s est 138,531 units), driven by Jaguar volume growth of 60% y-o-y to 32,193 units and LandRover volume growth of 12% to 117,702 units. Chery JV volumes were marginally lower by 2% to 12,532 units. Including JV, JLR volumes grew 26% y-o-y (+8% q-o-q) to 162,427 units (v/s est 155,847 units). JLR realisation at GBP44k (v/s est GBP42k) grew 4.7% q-o-q (-5.5% y-o-y) driven by better mix (10pp q-o-q decline in XE contribution).

Net sales at £6.6 bn (v/s est. £5.8 bn) grew 13% y-o-y (+14% q-o-q). JLR adj. Ebitda margins at 16.2% (v/s est 14.2%) improved 180bp q-o-q (-120bp y-o-y), driven by higher volumes and better mix.

In Q4FY16, other expenses included £166m one-off expenses pertaining to (i) the recall in the US of potentially faulty passenger airbags supplied by Takata (£67.4m), (ii) doubtful debts and (iii) previously capitalised investment. Adj Ebitda grew 5% y-o-y (+29% q-o-q) to £1.07 bn (v/s est £825m). Higher profits of Chery JV and lower tax due to deferred tax credits boosted adj PAT to £560m (+30% y-o-y, 35.5% q-o-q). Total Capex and Product development spend for the quarter was £742m and £3.13 bn for FY16. JLR’s Q4FY16 FCF was £1.4 bn, with CFO of £2 bn (driven by

£1.16 bn favourable working capital). For FY16, FCF generation was £743m (v/s £733 m in FY15).

The JV’s wholesale volumes were at 12,532 units (v/s 12,830 units in Q3FY16). JLR’s share in profit of Chery JV grew 123% q-o-q to £49m.

Valuation and view

Ex-China demand remains strong, JLR to gain share across geographies: FY16 is the year of transition for JLR as it would have three unprecedented events viz (i) own engine plant for the first time, (ii) China manufacturing plant and (iii) entry into high volumes with Jaguar XE. Jaguar portfolio has potential to go up 3x in volumes led by XE and Crossover F-Pace (FY16). China JV has started in Q4FY15, starting with three models (XF, Evoque Discovery Sport). These three models currently contribute 45-50% of China volumes, and as per management it has potential to go up 2.5x over 2-3 years on local production. Volume momentum is expected to improve driven by Discovery Sport, Jaguar XE and Evoque (in China JV).

China growth normalising but transitory issues receding: JLR’s transitory issues, in the form of model phase-out and teething troubles in China JV, have impacted volumes by 5-8% since Q3FY15. We expect volume recovery from transitory issues from Q3FY16, driven by (i) China Evoque ramp-up from Q3FY16, (ii) Discovery Sport launch in China in Q3FY16, (iii) New XF and XE in China from Q4FY16, and (iv) ramp-up of new launches in other markets. Despite China’s volume growth moderation, it is still expected to outgrow other markets with 8-10% CAGR over CY14-20. JLR is expected to outperform in China, driven by strong product pipeline, dominance in the fast growing SUV segment, and dealer network expansion.

JLR’s profitability has many levers: Pricing pressure due to moderating growth, adverse terms of trade, and increasing share of compact luxury cars are driving normalisation of profitability in China. We expect JLR’s profitability in China to normalise from 25% in FY15 to 15% by FY17, implying gross impact of 400bp. JLR has several levers, both cyclical and structural, to dilute the impact of China margin normalisation. Near-term Ebitda margin drivers (100bp savings) include (i) favourable commodity prices, (ii) operating leverage driven by recovery in volumes as transitory issues recede, and (iii) ramp-up in Chery JV. JLR has several structural drivers to margins (50bp factored in) including (a) full roll-out of modular strategy, (b) operating leverage driven by ramp-up in Jaguar portfolio, and (c) incremental production from low-cost countries.