Slight miss in revenue, but large margin beat: TCS’ revenue growth at 0.3% q-o-q cc/6.8% y-o-y cc missed even our muted estimate of 0.7% as growth was tepid in North America due to weakness in BFSI & retail, further hurt by higher than expected furloughs in a seasonally weak quarter. Ebit margin at 25% surprised positively though vs. our expectation of 24.3%, expanding 100bps q-o-q. Higher utilisation, better cost control and ccy aided margin improvement. Lower other income led to miss in PBT though this was partly offset by lower tax rate. The company also announced a dividend of Rs 5 per share.

Key takeaways from earnings call: (i) Within BFSI (5.3% y-o-y cc, -0.7% q-o-q), management indicated strength in insurance and Europe & Australia but weakness in North America and UK; (ii) management attributed weakness in retail (5.1% y-o-y cc, 4% q-o-q) mainly to issues with a few large North American accounts even as the vertical has done well in Europe & UK; (iii) strength in life sciences & healthcare (17.1% y-o-y cc, 3.8% q-o-q) was attributed to a number of large transformational deals; (iv) communications & media vertical continued to grow well (+9.5% y-o-y cc, 1.3% q-o-q); (v) on 2020 client budgets, management said that it was too early to call out but early indications appear to be mixed.

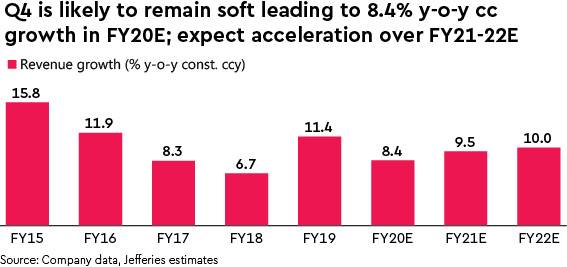

Maintain Buy: We tweak our FY20-22e estimates mainly to reflect better margin. Our price target increases to Rs 2,500 (prev. Rs 2,300) based on 23x 12m forward EPS as of Jan-21. Despite near-term headwinds, we maintain Buy.