")

TCS’ Q3 earnings missed as stronger cross ccy headwinds and higher subcontracting & employee expenses led to Ebit margin of 25.6%, well below estimates. However, it delivered on top line as (i) revenue growth in Q3 at 1.8% q-o-q const. ccy (12.1% y-o-y) was in line; (ii) deal TCV surprised positively at $5.9 bn vs. $4.9 bn in Q1/Q2; (iii) management maintained its positive outlook including for BFSI, retail & North America. We maintain Buy despite cut in margin estimates.

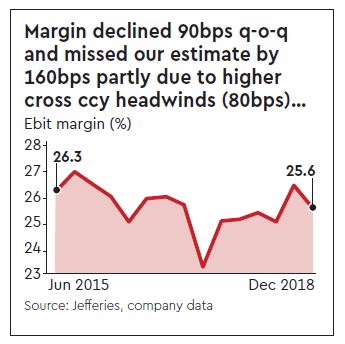

Revenue in line but margin misses

TCS’ Q3 revenue growth of 1.8% q-o-q const. Ccy (12.1% y-o-y const. ccy) was in line with our and consensus estimates; however, Ebit margin of 25.6% was well below our estimate of 27.2% as well as consensus of 26.7% and implies a decline of 90bps q-o-q. Some of the margin miss was on account of lower INR-USD realisation and stronger cross ccy headwinds (80bps) while the rest was mainly on account of higher employee and sub-contractor expenses and could remain a drag at least in the near term. TCS also announced a dividend of Rs 4/share.

READ ALSO: Flipkart’s Sachin Bansal books $21 million ride in Ola

Deal TCV surprises positively; commentary remains positive

Deal TCV of $5.9 bn was 20% higher than $4.9 bn in Q1/Q2, a positive surprise. Management indicated a strong deal pipeline build-up going into Q4 and that the deal win growth has been broad-based across verticals and geographies. Commentary on outlook remained positive including for BFSI, North America and retail, a relief given concerns going into results especially on the backdrop of Accenture’s cautionary tone in December and macro concerns.

Key takeaways from call

(i) Within BFSI, TCS indicated North America is doing better than Europe & UK in banking while the latter are leading in insurance; (ii) within retail, shift in spend from front end to back-end supply chain is emerging as a key trend helping TCS;

(iii) communications vertical continues to be volatile and 5G spend is still some time away and could manifest across verticals; (iv) share of digital revenue grew to 30.1% (+53% y-o-y) with AI-based automation and blockchain emerging as areas that saw lots of new deals.

READ ALSO: Bajaj Finance slapped with Rs 1 crore penalty by RBI; here’s why

Revising estimates mainly to temper margins

We cut EPS estimates by 3% over FY19-21e mainly to reflect lower margins as we now build in 25.5-25.7% Ebit margin vs. 26.3-26.5% earlier, slightly below management target of 26-28%. Our price target reduces slightly to Rs 2,230 as a result.

Maintain Buy — best growth outlook amongst Tier-1 IT companies

We maintain our Buy rating on the stock as TCS is best placed to deliver double-digit revenue growth over FY19-21e among Tier-1 IT cos in our view. High FCF/dividend yield, USD exposure, sector leadership should support its premium valuation.

READ ALSO: Reality check: 10% quota for economically weaker section, but govt job vacancies shrinking, shows DoPT data

Company description: TCS is the largest and among the oldest IT companies in India. It is a part of the diversified Tata Group. It provides a comprehensive range of IT services to industries such as banking & financial services, insurance, manufacturing, telecom, retail and transportation.