")

Drones have transformed warfare. The next defence race may be about stopping them.

In 3 Unlikely Winners of India’s ₹5.2 lakh-crore Drone Opportunity, we said that India’s drone boom could create winners far beyond drone manufacturers. Firms supplying electronics, embedded systems, and aerospace manufacturing gained as drone implementation rose.

But every tech cycle has a second phase. The first is about creating the technology. The second is about guarding against it. Modern wars have brought that second phase much sooner than expected.

A ₹50,000 drone can destroy military equipment worth several crores. That simple equation has brought a new challenge for armies globally. Air defence systems devised to stop aircraft and missiles are often too costly to use against low-cost drones flying in large numbers.

As armies improve their Counter-UAS capacities, the bigger break may lie not in making more drones but in building the engineering tech that can spot, rank, and destroy them.

Every attacking tech generates a defensive industry

History shows that every breakthrough in warfare eventually creates another industry. Aircraft made radar indispensable. Guided missiles led to missile-defence systems. Cyberattacks gave rise to cybersecurity. Drones are now driving demand for counter-drone technologies.

Unlike drone manufacturing, however, this ecosystem remains largely hidden. Most listed companies do not report anti-drone revenue separately because these capabilities sit within broader defence electronics businesses.

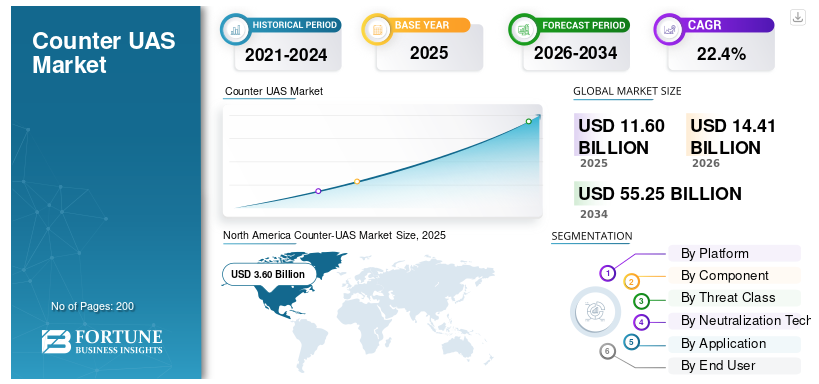

According to Fortune Business Insights, the global Counter-Unmanned Aerial Systems (C-UAS) market may grow from US$14.4 billion in 2026 to over US$55 billion by 2034, suggesting the scale of this evolving opportunity.

Counter UAS Market

These capacities may likely become crucial as drone usage rises. We’ve zeroed in on three listed companies that deal in different parts of this ecosystem: Astra Microwave, Paras Defence, and Zen Technologies. The last is perhaps the closest India has to a pure-play counter-drone company.

Battle One: Finding the Threat, Astra Microwave

Every anti-drone structure begins with a simple question: Is there danger in the sky?

Answering that question demands far more than a standard radar. Air-defence systems depend on several technologies to detect, recognize, and destroy low-flying airborne dangers.

And Astra neatly fits into the need. The company has quietly bettered its proficiency in RF, microwave, and defence electronics, positioning it as a key supplier to India’s advancing air-defence ecosystem.

The numbers show a business quietly moving up the value chain

Astra’s transformation has been gradual rather than spectacular, which is perhaps why it has largely stayed under the market’s radar.

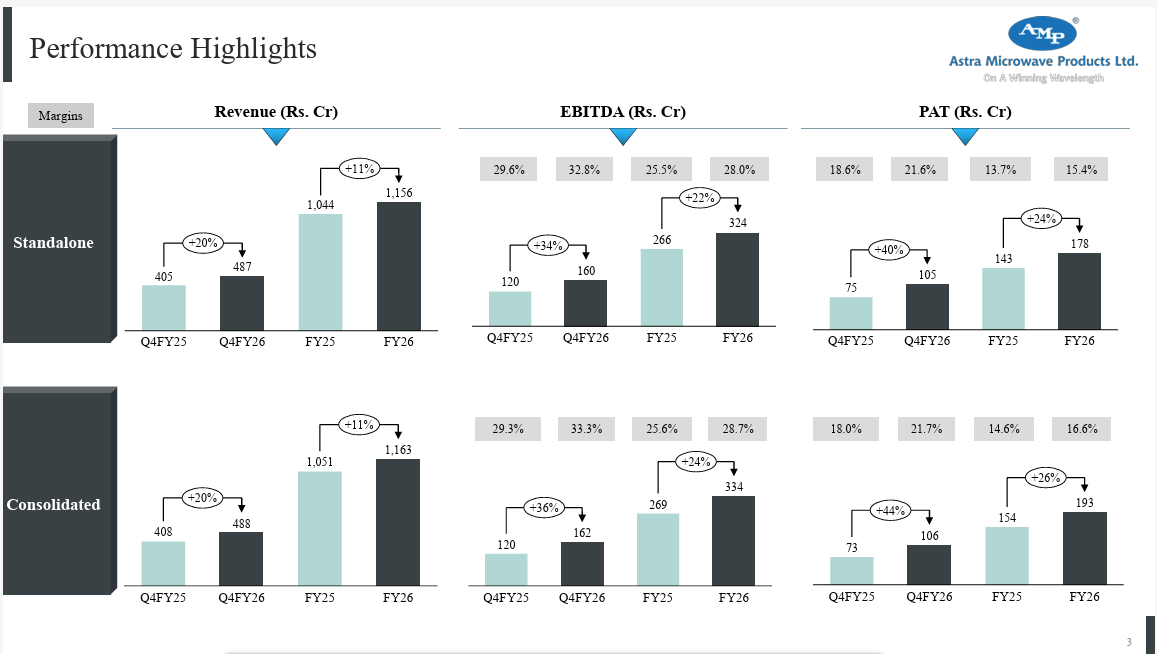

Revenue has grown to ₹1,163 crore in FY26 from ₹909 crore in FY24. The profitability has expanded even faster at 59.5% YoY from ₹121 crore in FY24 to ₹193 crore in FY26. The growth was driven by the shift to higher-value defence electronics and improved execution through long-cycle programmes.

Astra Microwave Performance Q4 & FY26

The progress is noticeable in its operating metrics. The operating margin expanded from the low teens to around the 29% in FY26, while return on capital employed was ~20%, suggesting better operational leverage and stronger returns on capital translating to shareholder gains, with Astra Microwave’s stock rising 68% over the past three years.

Astra Microwave 3-Year Share Price Trend

Equally important is the order book. At the end of FY26, Astra’s order book of ₹2,141 crores offered a strong revenue view in a business where defence orders usually run for several years.

The company has relationships with the Defense Research and Development Organisation, Indian Space Research, Bharat Electronics, Hindustan Aeronautics, and Bharat Dynamics.

In defence electronics, qualifying as a supplier is tough, but once included in tactical programmes, suppliers often benefit from long product cycles and high switching costs. That creates a competitive advantage, not directly obvious in quarterly earnings.

Beyond radar: Astra’s growing role in defence electronics

Astra Microwave is often seen as a radar company, but its role extends much further. The company supplies RF and microwave systems, electronic warfare components, and specialised defence electronics that back modern reconnaissance and air-defence platforms.

That diversification counts because anti-drone warfare is no longer about detecting an object in the sky. It demands multiple electronic systems to sense, process, and react to threats in real time. As armed forces spend more on spectrum authority and electronic warfare, Astra’s expertise places it above a conventional radar supplier.

Valuation

Astra Microwave is trading at a P/E of 83x, higher than the sector median of 62x as of 17th July 2026. Investors are obviously pricing in constant growth in radar, RF, and electronic warfare instead of valuing the company just on current earnings.

What Investors Should Watch

With much of the optimism already reflected in the valuation, investors must see if the business maintains its premium. Keeping an eye on the execution of the ₹2,141 crore order book, the latest orders in radar, RF, and electronic warfare programmes. Check if the operating margin is still above 25%, and if exports to friendly nations grow.

Key Risks

A premium valuation leaves little room for disappointment. Gaps in defence procurement, relaxed order execution, or margin compression could affect earnings and lead to a correction in valuation. The stock’s next leg of returns may likely depend more on earnings expansion than on multiple expansion.

Battle Two: Identifying the Threat, Paras Defence

Discovering a dangerous object is just the first step. The next question is verifying whether it is a friend, foe, or harmless resident drone.

That is becoming gradually harder as unmanned aircraft grow smaller, quicker, and more independent. Counter-UAS systems, today, hang on sophisticated optics, imagery, and investigation tech that can recognize and track dangers before there is any action.

Paras Defence has progressed from a niche defence optics company into a broader defence technology player, with devoted Counter-UAS solutions that place it at the heart of this swiftly growing segment.

From defence optics to anti-drone systems

Paras Defence created its standing in defence optics, imaging, and reconnaissance systems. Over the years, it has forayed into wider defence electronics, including devoted Counter-UAS solutions through Paras Anti-Drone Technologies.

Its portfolio now has drone RF and microwave customer developments, advanced phased arrays, next-gen software-defined radio, complex sensors, jammer guns, and unified anti-drone systems. That places the company at a key stage of the counter-drone chain: helping armed forces identify, track, and guard against unmanned aircraft before they become a threat.

The numbers show a steadily evolving defence business

The financial performance reflects a company benefiting from rising defence indigenisation and a growing portfolio of high-value technologies.

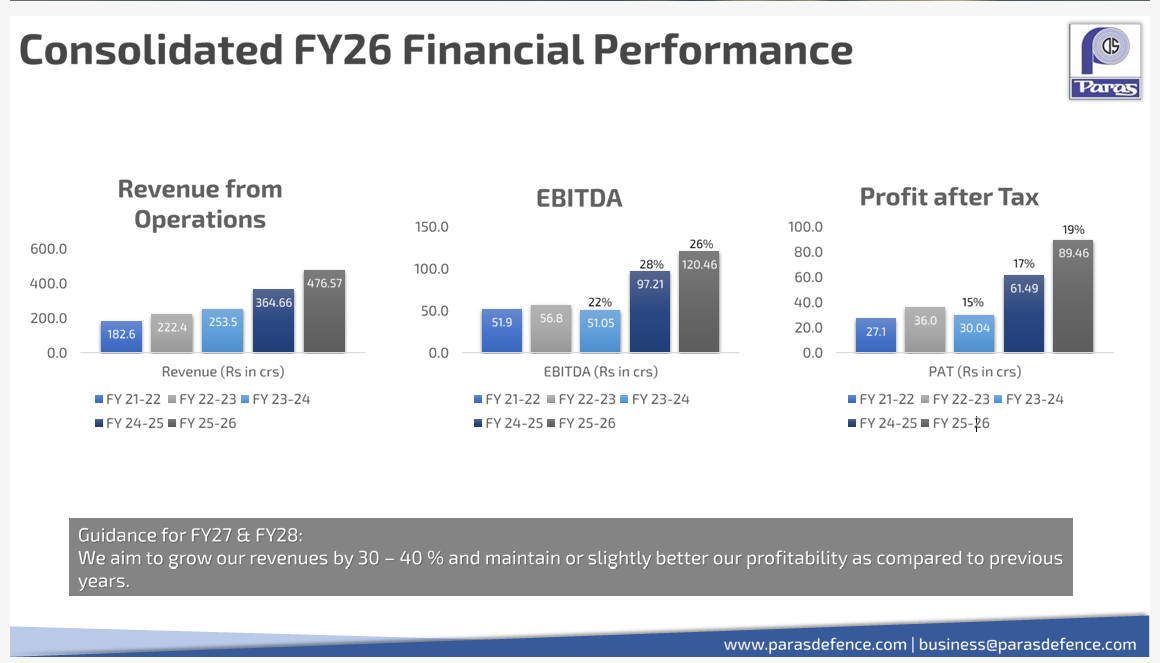

Revenue has increased from ₹254 crore in FY24 to over ₹477 crore in FY26, growing at a CAGR of 29% over the past three years. The net profit grew at a CAGR of 34% over the last three years from ₹30 crore in FY24 to ₹87 crore in FY26.

Paras Defence Performance FY26

The ROCE was 16.9%, driven by better capital efficiency and execution. The market seems to have rewarded this progress. The stock gained over 53% over the past three years.

Paras Defence 3-Year Share Price Trend

The company has a diversified order book of ₹986 crore. As India’s defence procurement slowly moves to local suppliers, Paras Defence may gain from long-term demand across multiple strategic programmes.

Valuation

Paras Defence has 110x P/E, which is higher than the sectoral median of 62x, suggesting the valuation has discounted a big part of the projected growth.

What Investors Should Watch

To sustain this premium, the company must show that its new divisions are growing with its core operations. Investors should monitor growth in anti-drone systems, expansion of the order book and execution, export opportunities, and planned tech partnerships.

Key Risks

At over 100x earnings, hopes are high. Any stoppage in order inflows, delays in commercialising new tech, or ineffective execution may lead to a sharp market reaction. Investors should therefore focus as much on execution as on growth.

Battle Three: Neutralising the Threat, Zen Technologies

Finding and tracking an aggressive drone serves little purpose if it cannot be deactivated.

Modern anti-drone warfare today depends on signal jamming and combined counter-UAS systems that can defuse threats quickly and efficiently. As armies pivot from depending on costly missile interceptors, such tech is becoming a critical layer of new air defence.

Best known for its defence training simulators, Zen Technologies has progressively extended into Counter-UAS and electronic warfare solutions, placing itself at the final stage of the counter-drone chain.

The numbers tell a much bigger story.

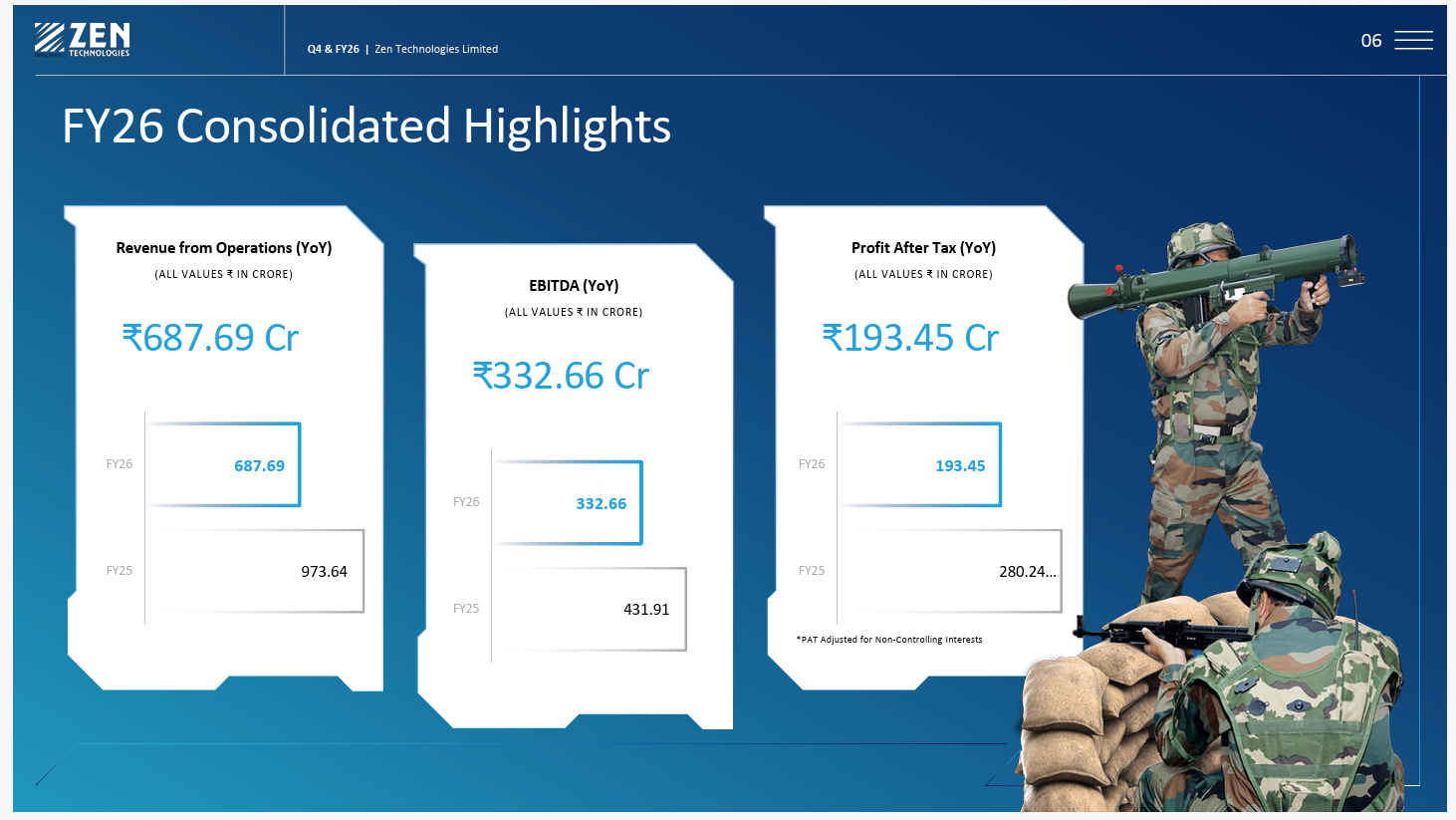

Zen’s financial performance echoes the fundamental shift underway in defence training and counter-drone technologies. Revenue rose from ₹440 crore in FY24 to over ₹689 crore in FY26, while the net profit excluding exceptional items increased to ₹217 crore in FY26 from ₹126 crore in FY24. The profit rose dramatically as the operating leverage improved and a significant share of revenue came from proprietary defence solutions.

Zen Technologies Consolidated Performance FY26

The quality of growth is equally impressive. The operating margins for FY26 was 48.4%, perhaps among the highest in the sector, driven by the company’s strong execution. Investors have taken notice, with Zen Technologies’ stock growing at a CAGR of 44% over the past three years.

Zen Technologies 3-Year Share Price Trend

The company’s order book of ₹1,336 crore in FY26 offers a glimpse into its growth trajectory.

Beyond simulation: A broader defence technology company

Zen Technologies has expanded into anti-drone and electronic warfare systems, indicating the changing needs of modern battlegrounds.

Rather than concentrating only on training soldiers, Zen is building technologies designed to interrupt and defuse hostile drones, making it one of the few listed companies with a direct presence in this emerging segment.

With mounting investments in simulation, anti-drone systems, and electronic warfare, Zen has changed from a training solutions provider to a defence tech business.

Valuation

Zen Technologies trades at 83x P/E, lower than the sector median of 62x, but well above most conventional defence manufacturers. Investors are pricing the company not just for its simulation business, but also for the promise of its anti-drone and electronic warfare portfolio.

What Investors Should Watch

The investment theory now centers on Zen’s capacity to grow into a broader defence technology company. Investors must look for growth in anti-drone and munition orders, product adoption, export growth, global partnerships, order implementation, repeat contracts, and capital efficiency.

Key Risks

Zen’s valuation supposes that recent growth will stay over the long term. Any slowdown in defence spending, gaps in new product adoption, or lower order inflows could alter earnings expectations. Allowing the premium valuation, the stock may still be vulnerable to execution risks.

The market may still be asking the wrong question

This story is not truly about three companies. It is about where value travels when technology changes. Investors often begin by focusing on the most visible product.

In earlier tech cycles, the investors focused on automobiles before component makers appeared as large gainers. The smartphone era emphasized phone brands, but semiconductor companies created massive long-term value.

The drone industry may follow a similar path. Every drone inducted into service creates demand for technologies that can find, catalogue, and defuse it. That is quietly giving rise to an ecosystem that extends far beyond drone manufacturers. Most listed companies do not distinctly disclose revenue from anti-drone or electronic warfare systems, making the opportunity easy to miss.

As defence budgets increasingly prioritise resilience alongside capability, companies building radar systems, electro-optics, and electronic warfare solutions could become just as important as those building drones themselves.

The next phase of returns for Astra Microwave, Paras Defence, and Zen Technologies, however, will depend on execution, converting tech capabilities into repeated earnings growth.

For investors, that may mean the next defence opportunity may belong to those building the invisible shield that stops them.

Want to keep an eye on these businesses? Add them to your watchlist.

Disclaimer:

Note: We have relied on data from the May 2026 investor presentation, www.Screener.in, throughout this article. Only in cases where the data was not available have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative

purposes only.

Archana Chettiar is a writer with over a decade of experience in storytelling and, in particular, investor education. In a previous assignment at Equentis Wealth Advisory, she led innovation and communication initiatives. Here, she focused her writing on stocks and other investment avenues that could empower her readers to make potentially better investment decisions.

Disclosure: The writer and her dependents do not hold the stocks discussed in this article.

The website managers, their employees (s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities, or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources, and only after consulting such independent advisors as may be necessary.