")

Banking is becoming more important as the global economy turns faster, more digital and more interconnected. Businesses need funding to expand, consumers depend on credit for major purchases, and digital payments now support everyday transactions. Banks also help move savings into productive investments. As economic activity grows, the need for banking services becomes difficult to avoid.

India’s banking sector is expanding with the country’s digital and economic growth. UPI has changed how people make payments. Formal credit is reaching more individuals and small businesses. Rising incomes, urbanisation and infrastructure spending are also increasing the demand for loans. At the same time, technology is helping banks serve customers beyond traditional branches.

Banking stocks are important for stock market investors because banks sit at the centre of the economy. Their loan growth can reflect business and consumer demand. Their asset quality can indicate financial stress. Their profitability can also offer clues about the broader economic cycle. This makes banking stocks an important part of many investment portfolios.

In this article, we look at three of India’s cheapest banking stocks using the price-to-book value, or P/BV, ratio. The ratio compares a bank’s market price with its book value per share. It is widely used for banks because their main assets and liabilities are financial and appear on the balance sheet. A lower P/BV ratio can signal a cheaper valuation. However, investors must also examine asset quality, profitability and growth prospects.

#1 Bank of India: Can Growth and a 3.2% Dividend Yield Support a Re-rating?

Bank of India is a public sector bank with operations in India and overseas markets. Its business spans retail, agriculture, MSME, corporate and international banking.

Bank of India Financial Performance

| Metric | FY26 |

| P/BV | 0.7x |

| Dividend yield | 3.2% |

| NII growth | 3.0% |

| Net profit growth | 14.0% |

| Net NPA | 0.56% |

| RoE | 12.4% |

Bank of India trades at a price-to-book value of 0.7x. This is below the peer median of 1.0x. The stock also offers a dividend yield of 3.2% as on July 17, 2026. This combination places it among the cheaper banking stocks. However, improvement in margins will be important for a sustained re-rating.

The bank reported steady earnings growth in FY26. Net interest income rose 3% year-on-year (YoY) to Rs 25,172 crore. Net profit increased 14% to Rs 10,527 crore. Non-interest income also grew 10% to Rs 9,874 crore. However, global net interest margin fell to 2.52% from 2.82% in FY25.

Business growth was stronger than income growth. Global advances increased 15.8% to Rs 7.7 lakh crore. Global deposits rose 13.6% to Rs 9.3 lakh crore. Retail, agriculture and medium, small and micro enterprises (MSME) advances grew 19.1%. These segments accounted for 58.7% of advances.

FY27 Credit Pipeline and Corporate Lending Projections

For FY27, the bank expects global advances to grow by 15-16%. Global deposit growth is expected at 13-14%. It has a credit pipeline of Rs 65,000-70,000 crore. Around Rs 50,000 crore relates to the corporate segment. The pipeline includes roads, power, data centres, electric vehicles, solar panels, biogas and gas transmission projects.

Bank of India is also expanding its branch network. It opened 200 branches in FY25 and another 200 in FY26. More than 200 new branches are planned in FY27. These branches will focus on deposits, retail loans and wealth-management products.

Deposit mobilisation remains central to the expansion. Under Project UDAAN, the bank is tracking branch-level targets for current accounts, savings accounts and retail term deposits. It has also started Zonal Deposit Centers. The bank aims to increase current account savings account (CASA) deposits to around Rs 3.3 lakh crore in FY27 from Rs 3 lakh crore in FY26.

International operations account for about 14% of the bank’s loan book. Margins in this portfolio remain low at around 1.10-1.30%. The bank is therefore focusing on domestic retail, MSME and mid-corporate loans, where yields are better. It is also seeking a domestic or international partner for its mutual fund business.

Asset Quality Gains vs Core Margin Compression

Asset quality continued to improve. Gross non-performing asset (NPA) declined to 1.98%, while net NPA fell to 0.56%. The slippage ratio improved to 0.83%. Bank of India earns a return on equity (RoE) of 12.4% and a return of capital employed (RoCE) of 5.9%.

The 0.7x P/BV and 3.2% dividend yield strengthen the stock’s value proposition. Loan growth and improving asset quality offer further support. However, falling margins remain a concern. A recovery in net interest income growth and margins will be central to narrowing the valuation discount.

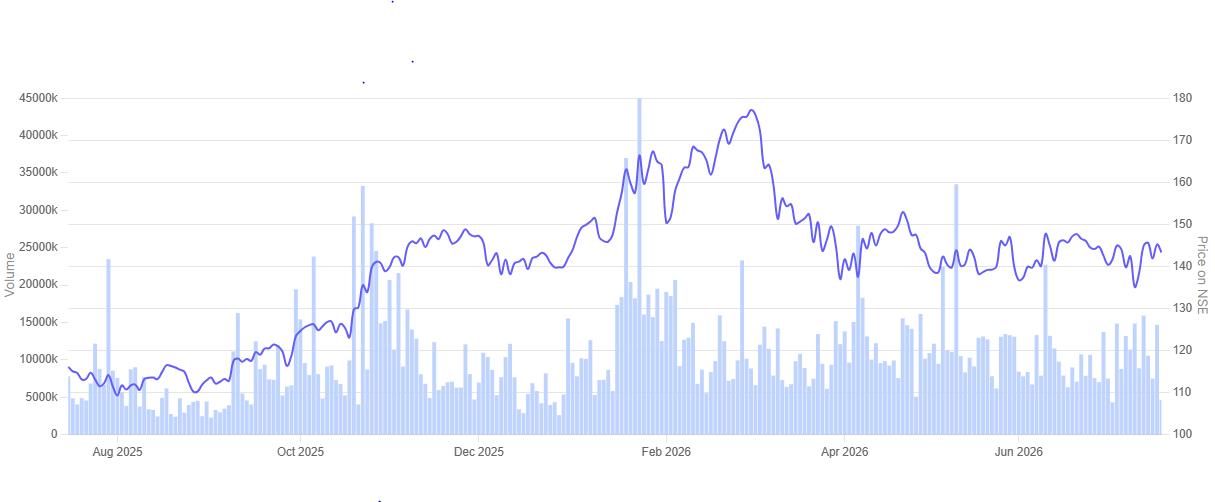

In the past year, the share price of Bank of India is up 23.2%.

Bank of India 1 Year Share Price Chart

#2 Central Bank of India: Credit Growth Outpaces Competitors as Slippages Soften

Central Bank of India has a strong retail-focused lending model. Retail, agriculture and MSME loans account for a major share of its advances.

Central Bank of India Financial Performance

| Metric | FY26 |

| P/BV | 0.8x |

| Dividend yield | 3.7% |

| NII growth | 2.0% |

| Net profit growth | 15.4% |

| Net NPA | 0.49% |

| RoE | 11.9% |

Central Bank of India trades at a price-to-book value of 0.8x. This is below the peer median of 1.0x. The stock also offers a dividend yield of 3.7% as of 17 July 2026. The discount places it among the cheaper banking stocks. However, further improvement in earnings will be important for a re-rating.

The bank reported steady profit growth in FY26. Net interest income rose 2% YoY to Rs 14,171 crore. Net profit increased 15.4% to Rs 4,369 crore. The annual profit growth came despite a one-time deferred tax impact of Rs 632 crore.

Credit growth remained the main driver. Gross advances increased 18.8% to Rs 3.4 lakh crore. Retail, agriculture and MSME loans together grew 21%. Retail loans rose 25.7% and crossed Rs 1 lakh crore. Agriculture and MSME advances grew 17.6% and 17.1%, respectively.

Operational Outreach and Targeted Credit Growth for FY27

The bank expects advances to grow by 14-16% in FY27. Deposit growth is projected at 10-12%. It has conducted outreach programmes at more than 100 locations to generate retail, agriculture and MSME business. The bank has also identified 225 branches with MSME potential and more than 300 branches for agriculture lending.

Expansion is also planned in corporate banking. The bank intends to open more corporate finance branches and mid-corporate branches. More than 900 officers are expected to join in October 2026. They will be deployed at branches with higher credit potential. A separate sales and marketing team is also being set up.

Technology remains another area of investment. Overall, Central Bank of India has budgeted Rs 1,442 crore for capital spending and Rs 1,276 crore for revenue expenditure in FY27. It is also setting up a wealth-management division. The bank is also strengthening its centralised forex operations and digital account-opening facilities.

Improving Asset Ratios and Capital Spending Roadmaps

Asset quality improved during FY26. Gross NPA declined by 51 basis points to 2.67%. Net NPA stood at 0.49%. The slippage ratio fell to 1.16% from 1.45%. Management aims to bring it below 1% in FY27. The bank earned a RoE of 11.9%.

At 0.8x book value, the stock continues to trade below the peer median. Its 3.7% dividend yield adds to the value proposition. Strong credit growth and improving asset quality offer support. However, net interest income grew at a slower pace than advances. Maintaining margins above 3% will therefore be important for narrowing the valuation discount.

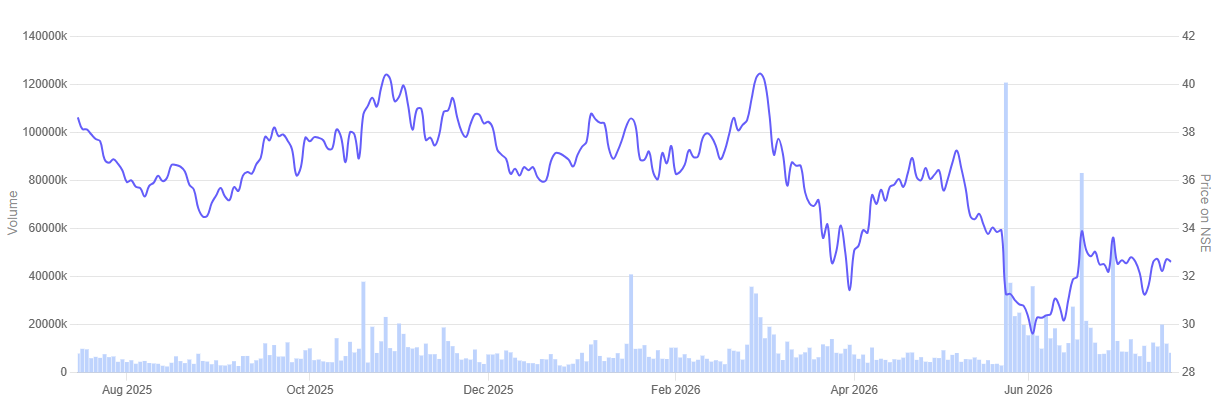

In the past year, the share price of Central Bank of India is down 15.4%.

Central Bank of India 1 Year Share Price Chart

#3 Bank of Baroda: Re-Rating Outlook Anchored to 3.4% Yield and Margin Recovery

Bank of Baroda is one of India’s larger public sector banks, with a sizeable domestic and international presence. It serves retail, corporate, MSME and rural customers across markets.

Bank of Baroda Financial Performance

| Metric | FY26 |

| P/BV | 0.8x |

| Dividend yield | 3.4% |

| NII growth | 2.5% |

| Net profit growth | 2.2% |

| Net NPA | 0.45% |

| RoE | 12.7% |

Bank of Baroda trades at a price-to-book value of 0.8x. This is below the peer median of 1.0x. The stock also had a dividend yield of 3.4% as of 17 July 2026. The discounted valuation places it among the cheaper banking stocks. However, margins and deposit growth will shape any re-rating.

As on 31st March2026 the bank’s global business stood at Rs 30.8 lakh crore. This was an increase of 13.9% YoY. Global advances rose 16.2%. Domestic advances grew 14.5%, while international advances increased 24.4%.

Retail, agriculture and MSME lending remained the main growth drivers. The organic retail book grew 17.9% and crossed Rs 3 lakh crore. Agriculture loans increased 20.7%, while organic MSME loans rose 15.6%. Corporate lending grew at a slower 11.2%.

For FY26, net interest income rose 2.5% YoY to Rs 47,682 crore. Net profit increased 2.2% to a record Rs 20,021 crore. However, operating profit declined 0.5% to Rs 32,259 crore. Global net interest margin stood at 2.89% for the year.

CASA Deposit Mobilisation Challenges and Yield Pressures

Bank of Baroda expects loan growth of 12-14% in FY27. Deposit growth is projected at 10-12%. Total deposits grew 12% in FY26. However, term deposits increased faster than low-cost deposits. Domestic CASA grew 9.8%, while term deposits rose 14.8%. This mix could keep the cost of funds under pressure.

The bank is also expanding beyond traditional lending. It raised nearly Rs 10,000 crore through green infrastructure bonds. Its primary dealer subsidiary began operations on 1 April 2026. The bank has committed Rs 2,000 crore to this business. It also plans to establish a pension fund. Management expects this process to take six to nine months, subject to regulatory approvals.

International operations remain an important part of the business. Advances outside India grew 24.4% during FY26. The portfolio includes operations in the US and the Middle East. Management said the international book remains diversified. However, geopolitical risks will require monitoring.

Loan Growth Balancing International Book Risks

Asset quality continued to improve. Gross NPA declined to 1.89%, while net NPA fell to 0.45%. The FY26 slippage ratio improved to 0.72%. The bank reported a RoE of 12.7% and a RoCE of 5.6%.

The 0.8x P/BV and 3.4% dividend yield support the valuation case. Credit growth and asset quality are also favourable. However, the bank must protect margins as loans grew faster than deposits in FY26. This will be central to narrowing the discount to peers.

Conclusion

For now, the valuation discount across these banks comes with different trade-offs. Credit growth remains strong, while asset quality has improved. Dividend yields also offer some support. However, growth in net interest income has not always kept pace with the expansion in advances.

The next test will be funding this growth without putting further pressure on margins. Deposit mobilisation, particularly through low-cost CASA deposits, will be important. Investors must also track fresh slippages, credit costs and returns on equity.

A lower P/BV can indicate value, but it can also reflect weaker profitability or slower earnings growth. A sustained re-rating will depend on whether these banks can convert loan growth into stronger interest income and returns, while keeping asset quality under control.

India’s Cheapest Banking Stocks

| Metric | Bank of India | Central Bank of India | Bank of Baroda |

| P/BV | 0.7x | 0.8x | 0.8x |

| Dividend yield | 3.2% | 3.7% | 3.4% |

| FY26 NII growth | 3.0% | 2.0% | 2.5% |

| FY26 net profit growth | 14.0% | 15.4% | 2.2% |

| Net NPA | 0.56% | 0.49% | 0.45% |

| RoE | 12.4% | 11.9% | 12.7% |

Source: Screener.in and FY26 company results and earnings-call transcripts.

You can track how these are progressing by adding stocks to your watchlist.

Disclaimer:

Note: We have relied on data from www.Screener.in throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Ekta Sonecha Desai has a passion for writing and a deep interest in the equity markets. Combined with an analytical approach, she likes to deep dive into the world of companies, studying their performance, and uncovering insights that bring value to her readers.

Disclosure: The writer and her dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.

offers overtake domestic rates at many banks")