There’s a wire behind the wall of the room you’re sitting in right now. You don’t see it. Don’t think about it. But without it, electrical equipment doesn’t work.

That wire is made of copper.

And right now, somewhere between a mine in Chile and a factory in Gujarat, a very quiet, very expensive scramble is underway to make sure there’s enough of it.

The problem is that India digs up barely a fraction of the copper it consumes. Every electric vehicle rolling off an assembly line needs roughly four times the copper of the petrol car it’s replacing.

Meanwhile, new data centers, or upgraded power grid, and even rooftop solar panel – all of them are quietly bidding for the same shrinking pile of metal that is copper.

What’s noteworthy is that global mines are ageing, ore quality is falling, and building a new one takes over a decade.

While India is behind on copper production, a select few companies aim to change that and if successful, the potential rewards can be huge.

Keeping that in mind, here are four copper stocks worth putting on your watchlist.

#1 Hindustan Copper

First on the list is the obvious name, Hindustan Copper.

Hindustan Copper is a public sector undertaking under the administrative control of the Ministry of Mines, the Government of India (GoI). At present, the government holds a little over 66% stake in it.

It has five units viz. Malanjkhand Copper Project (MCP) in Madhya Pradesh, Khetri Copper Complex (KCC) in Rajasthan, Indian Copper Complex (ICC) in Jharkhand, Taloja Copper Project (TCP) in Maharashtra and Gujarat Copper Project (GCP) in Gujarat.

Among all the domestic players, Hindustan Copper truly stands out as India’s only fully integrated copper producer. It engages in all stages of copper production, from mining to the final conversion into marketable products. The company holds nearly two-fifths of the nation’s copper ore reserves.

What’s interesting is that the company has had a spectacular run both in terms of stock price appreciation and financials, due to the copper situation.

Over the past 5 years, its sales have grown at a compounded annual growth rate (CAGR) of 20% and 18% respectively.

During the same period, its ROE and ROCE have averaged 15% and 18%.

To meet the rising domestic demand, Hindustan Copper is expanding its mines and plans to increase its annual capacity from the current 4.3 MT to 12 MT by 2030-31.

At the 12 MT production level, it anticipates producing 80,000-90,000 tons of metal-in-concentrate. It also plans to invest Rs 20 billion (bn) over the next 5-6 years, with an annual allocation of Rs 4.5-5 bn for mine expansion.

It’s also acquiring new copper deposits in India and exploiting new blocks in Chhattisgarh, Rajasthan, and Jharkhand. The company is also participating in upcoming mineral auctions abroad to diversify its geographical base.

The company has also signed agreements to sell its primary product, copper concentrate, to Kutch Copper and Hindalco.

With all these ambitious plans, Hindustan Copper is a must have stock on your watchlist.

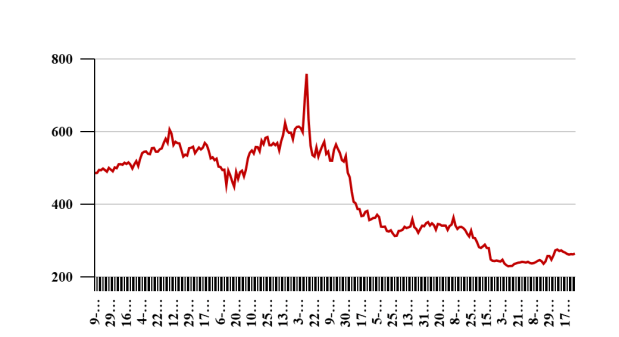

Hindustan Copper Share Price

Data Source: BSE

#2 Hindalco

Second on the list is Hindalco.

It’s the second-largest aluminium manufacturer in India, with capacity of 1,340 kilo tonne per annum (KTPA) of aluminium and 3,740 KTPA of alumina. It has a custom smelter with copper cathode capacity (including recycling) of 421 KTPA in Dahej, Gujarat.

This integrated smelting complex in Gujarat is one of the largest single-location custom copper smelters in the world. Thus, it has strong economies of scale to compete globally and thereby diversify its revenue mix.

Coming to its financials, Hindalco’s sales have grown at a CAGR of 16% and 21% between FY21-26.

During the same period, its ROE and ROCE have averaged 12% and 13% respectively.

At present, Hindalco is investing heavily in expanding its downstream and global footprint, particularly through Novelis.

Moreover, it has robust demand prospects. Aluminium is a critical material for electric vehicles, renewable energy projects, and infrastructure development. With growing global emphasis on green energy and electrification, demand for aluminium continues to rise steadily.

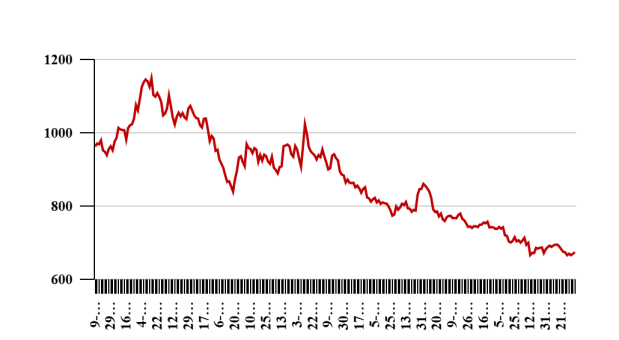

Hindalco Share Price

Data Source: BSE

#3 Precision Wires

Third on the list is Precision Wires.

It manufactures enamelled copper winding wires essential for motors, transformers, and EV components.

It has a manufacturing facility located at Silvassa, Dadra Nagar Haveli and Palej, Gujarat with a total estimated installed capacity of 55,000 metric tons per annum (MTPA) as on March 2026.

At present, it’s touted to be a leading player in the organized copper winding wires, catering to diverse industries.

In recent years, the company’s financials have been supported by higher operational efficiency and some price pass-through in a high copper environment.

What sets the company apart is its focus on backward integration, copper scrap recycling, and cathode production. This reduces dependency on volatile market prices and positions the company well for margin stability.

Coming to its financials, its sales and net profit have grown at a CAGR of 20% and 23% respectively over the past 5 years.

Its ROE and ROCE have averaged 15% and 26% during the same period.

With good demand for electric vehicles and green energy, the company is looking to expand its production capacity.

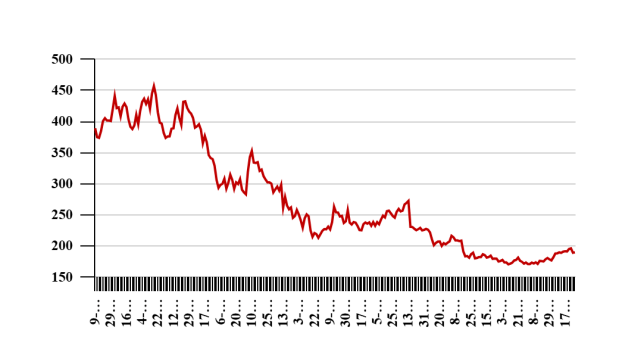

Precision Wires – 1 Year Share Price

Data Source: BSE

#4 Bhagyanagar India

Fourth on the list is Bhagyanagar India.

Bhagyanagar India, incorporated in 1985, is the flagship company of the Hyderabad-based Surana Group. It manufactures a wide range of copper products, with an annual installed capacity of 15,000 metric tons.

The company caters to various Original Equipment Manufacturers (OEMs) and players in the auto components industry. Its products find applications in telecommunications, power and distribution, low-range transformers, solar panels, and auto ancillaries, among others.

Its customer base includes original equipment manufacturers (OEMs) such as Lucas, TVS Limited, MICO, Commutator, Emvee Solar, Amar Raja Batteries, and HBL Nife.

While relatively small at the moment, the company’s copper segment is expected to gain traction on the back of growing demand.

Coming to its financials, its sales and net profit have grown at a CAGR of 28% and 63% respectively over the past 5 years.

Its ROE and ROCE have averaged 10% and 16% during the same period.

Looking ahead, the company has diversified its operations into the export market.

It also plans to conduct research and development to develop copper foils and commutator segments.

The strategy is to maintain a continued focus on adding new value-added products to attract OEM customers across various sectors, including Automotive, Electrical Switchgear, and Heating.

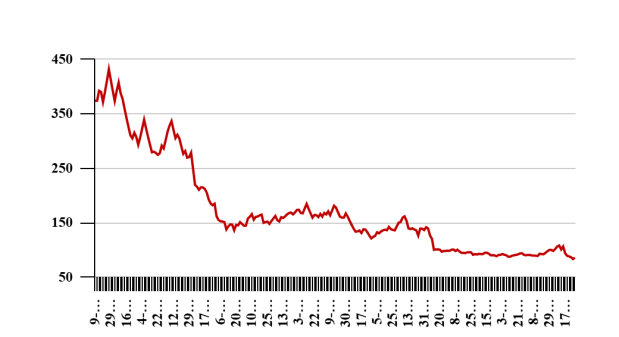

Bhagyanagar Ind – 1 Year Share Price

Data Source: BSE

Conclusion

Copper never gets the applause that gold gets, or the excitement that a hot IPO gets. It just sits quietly at the centre of everything being built, and it will sit there whether or not anyone’s watching.

That’s exactly why it deserves watching. The companies we discussed here have a seat at the table of a demand story that isn’t slowing down anytime soon.

EVs that need four times the copper of the cars they’re replacing, a power grid being rebuilt for a different energy era, and a mining pipeline that simply cannot keep pace.

But make no mistake – that mismatch doesn’t resolve itself in a quarter. It plays out over years.

Also, none of this means you should put blind conviction in those companies. Commodity cycles are brutal to the impatient and unkind to the overleveraged. Copper has humbled plenty of investors who mistook a structural story for a straight line.

Investors should carefully evaluate these companies’ fundamentals, corporate governance, and valuations as key factors when conducting due diligence.

Happy investing.

Disclaimer: This article is for information purposes only. It is not a stock recommendation and should not be treated as such. Learn more about our recommendation services here…

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.