")

In the stock market, there are two ways to look at a company. One is through the lens of a Fundamental Analyst who dives into balance sheets, calculates PE ratios, and worries about future cash flows.

The other is through the eyes of a Market Veteran, who reads the “mood” of the market and the story the price is telling. And today we look at this PSU that has kept both sides busy.

With a market cap of Rs 60,683 cr, National Aluminium Company (NALCO) manufactures and sells Alumina and Aluminium.

The company is a Navaratna Central Public Sector Enterprise under the Ministry of Mines. It is one of the largest integrated Bauxite-Alumina-Aluminium-Power Complex in India and one of the largest integrated primary producers of aluminium in Asia.

However, the company is currently a battleground where two views are colliding. In November 2025, Two of India’s top brokerage houses, ICICI Securities and Motilal Oswal, essentially told investors to pack their bags.

They set targets of Rs 246 and Rs 250, suggesting that the stock was “fully priced.”

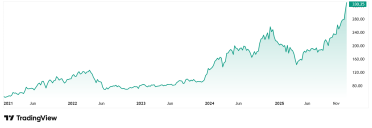

5-Year Stock Price Chart For NALCO

If one took their advice and backed out, they missed a 30% rally. The stock is now trading at Rs 330 (as of closing on 2nd January 2026). This divergence could cause investors significant grief. To try and understand why this probably happened, let me share with you what my friend and highly followed market veterans, Brijesh Bhatia said about it a few days ago.

Price Action vs. Excel Sheets

Brijesh points out that brokerage houses look at valuation reports through a rearview mirror, but price action looks through the windshield. While the analysts worry about spreadsheets, Brijesh argues that NALCO is riding a “Supercycle” wave that defies conventional logic.

In his recent article, he shared a perspective that explains this rally better than any excel sheet. He notes that when a stock ignores a major downgrade and hits a new 52-week high instead, it is a sign of “Institutional Appetite.”

According to Brijesh, NALCO isn’t just rising on fluff; it is breaking out of a multi-year slumber.

- The Breakout: He highlights that NALCO has shattered a massive resistance ceiling. When a PSU giant moves like this after years of underperformance, it’s rarely a fake out.

- The “Supercycle” Theory: Brijesh believes we are entering a phase where tangible assets (like Aluminium) will outperform paper assets. “In a commodity bull run,” Brijesh notes, “PE ratios often look expensive before the earnings explode to justify them. If you wait for the PE to drop, you’ll miss the bus.” If I understand him correctly, he is saying that the market is pricing in a future scarcity of Aluminium that the conservative analysts haven’t factored in yet.

Why The Analysts Said “Sell”

To be fair to them, their concerns are not completely invalid. Their standing comes from a place of what they read in the companies’ numbers.

- The Capex Monster: ICICI Securities downgraded the stock to “HOLD” with a target of Rs 246 primarily because of the company’s ambitious spending plans.

NALCO plans to sink nearly Rs 30,000 cr into expanding its smelter and power plants. History shows that when PSUs go into a heavy capex mode, their free cash flow dries up, and dividend yields (currently an industry high of 3.2%) often dwindle.

- Valuation Trap: Motilal Oswal maintained what we can call a neutral stance with a target of Rs 250. They believe the best-case scenario, which is high aluminium prices, is already priced in.

The 45% Margin Miracle

So, why is the stock climbing despite all these warnings?

Because the current numbers are simply too good to ignore. While analysts worry about future cash flow, the current cash flow is a sight for sore eyes.

- Profit Explosion: In Q2FY26, NALCO reported a Net Profit of Rs 1,430 cr, a massive jump of 37% year-on-year.

- The Margin Miracle: Operating margins (EBITDA) expanded to 45% in FY25, up from 22% in FY24. This is where Brijesh’s narrative of operational efficiency kicks in. NALCO is squeezing more profit out of every tonne of metal than almost anyone else.

- The Dividend Cheque: Ignoring the cash crunch fears, NALCO declared an interim dividend of Rs 4 per share in November. This signals that management isn’t as worried about cash as the analysts are.

The Bauxite Advantage (NALCO’s Secret Weapon)

The secret weapon that keeps NALCO profitable, even when prices fluctuate, is its backward integration. Unlike peers who buy Bauxite (raw material), NALCO mines it.

In Q2, their Alumina sales volume hit a multi-quarter high of 396,000 tonnes, up 39% YoY (Per Axis Direct Report in Nov 2025). As Brijesh often says, “In commodities, the lowest cost producer always wins.” With global Alumina prices staying elevated due to supply shocks in Australia and Guinea, NALCO’s free bauxite allows it to capture the entire profit margin.

This is a structural advantage that doesn’t disappear just because the stock price went up.

A moat few can boast about, nor can copy.

Risks: China, Capex, and Gravity

Now, as we all agree, trees don’t grow to the sky. All must act with caution and due diligence. Investors buying at Rs 330 must be aware of the risks:

- China Factor: If China floods the market with cheap aluminium (as it has done in the past), prices will crash. NALCO’s profits are highly sensitive to global prices.

- The Execution Risk: Spending Rs 30,000 cr is not easy. Delays in the new smelter could drag down Return on Equity (ROE) for years.

- Overbought Levels: The stock has rallied over 50% in a year. A technical pullback is overdue.

Verdict: Momentum vs. Safety

NALCO is currently something many would call a Momentum Beast. The disconnect between the Analyst Target (Rs 250) and the Market Price (Rs 330) is a rather glaring one. If you are a conservative investor who hates risk, the ICICI/Motilal reports could be your book to go by.

The valuation is stretched, but if you align with what Brijesh has to say, which respects price action and sector rotation, then NALCO remains a strong contender to consider to be a part of one’s watchlist.

The stock is proving that in a bull market, earnings growth (37% up) matters more than valuation multiples. Watching this unfold over the coming months and years will be fascinating. We recommend adding the stock to a watchlist and following it closely.

Disclaimer:

Note: We have relied on data from www.Screener.in and www.trendlyne.com throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Suhel Khan has been a passionate follower of the markets for over a decade. During this period, He was an integral part of a leading Equity Research organisation based in Mumbai as the Head of Sales & Marketing. Presently, he is spending most of his time dissecting the investments and strategies of the Super Investors of India.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.