In our interaction, mgmt sounded optimistic on growth with rising share of protect & non par likely to aid margin expansion. Proactive vaccination and digital enablement of sales force is helping growth. Lagged wave-2 claims are tracking co. estimates and June’21 Covid reserves seem adequate, but mgmt is watchful of wave-3. Not much repricing pressure from reinsurers currently. We lift VNB est. by 7-9% and raise TP to Rs 1,380 (vs Rs 1,240) on 2.9x June-23EV. Buy.

Strong growth momentum expected to sustain: Mgmt sounded sanguine on premium growth for the year. July-Aug growth has been very strong at 30%-70% while Sept. is also tracking well. Growth is driven both by savings and protection. SBIL’s efforts to proactively vaccinate employees/agency force and facilitating digital tools is yielding results. SBI remains a key growth driver across products; non-SBI partners (such as SIB, PSB, UCO) are posting very high growth on a low base. Currently, these banca tie-ups form ~2-2.5% of NBP mix; SBIL expects its share to move up to ~8% over the next 3-4 years.

Focus on protection to rise further: SBIL has posted strong growth in protection (43% in FY21 and 76% in Q1FY22). SBIL has been traditionally RoP heavy in protect with ~85:15 mix for RoP:non RoP. Pure term product launched this quarter will help diversify its offering and further increase share of protection in product mix – mgmt intends to take protection share to ~14-15% of NBP vs. ~12% in FY21. Credit Life is also seeing strong traction due to higher disbursal rate at SBI – attachment rates have moved up here from ~45% to 47%. On group term, however, the company maintains a cautious approach.

Market conditions helping savings products growth: Favourable capital market conditions are supporting growth in ULIPs. SBIL saw y-o-y decline in guarantees in Q1FY22, but with repricing of rates it has started to push for growth in guarantees again. Annuities is a focus area growing strongly in individual segment. Mgmt targets to take share of non par savings to ~14-15% over next few years with share of ULIP likely to ease lower.

Reinsurance: SBIL has not faced much repricing pressure from reinsurers owing to somewhat different product construct. RoP products have much lower sum assured which moderates need for medicals. Moreover, SBIL’s term pricing has been more broad based. In recent discussions, too, SBIL is not seeing indications from reinsurers to hike term prices – lower ceding rate also likely helping.

Lagged Covid wave-2 claims in line with reserving: Mgmt does not see material risk of overshoot on its June-21 Covid reserves of Rs 4.4 bn. While wave-3 is yet to become concerning, mgmt remains watchful of any claims spike from delta variant induced wave-3.

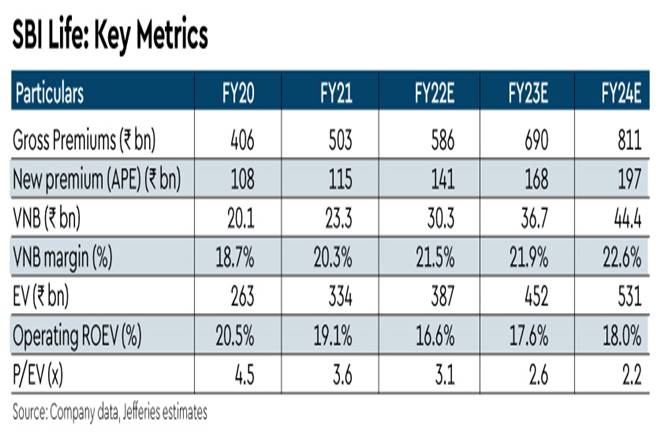

Buy stays: We maintain Buy and raise PT to Rs 1,380 (from Rs 1,240) driven by better growth (FY22 APE growth est. at 23%) and margin assumption (lifting VNB est. by 7%-9%) and higher multiple of 2.9x on June-23 EV. We build in VNB CAGR of 24% over FY21-24e. Stock trades at 2.6x FY23e EV for an op RoEV of 17%.