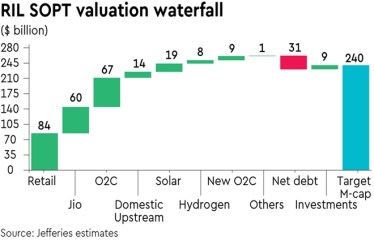

After having outperformed Nifty by 4% in 2022, shares of Reliance Industries (RIL) can rally to fresh lifetime highs this year, global brokerage firm Jefferies said. It has forecast 18% Ebitda growth in FY24E with 21% in Retail on the back of floorspace growth and 24% in Jio on tariff hike and home broadband traction. We see potential earnings upside from oil-to-chemicals (O2C) if China’s demand recovers by mid-CY2023 and export duties are eliminated. Valuation has moderated imputing little value to green energy in our view. Borrowings are likely to rise. Maintain Buy with a PT of `3,100 for 23% upside.

Reliance Retail – Expect strong FY24: After a 40% core area addition in FY23E, we expect network expansion to normalise in FY24. Revenue growth will remain strong at 25% driven by improvement in store throughput. Ebitda should rise 21% as margins moderate a bit as covid-related cost controls are reversed. We expect further expansion in merchant network and product assortment in New commerce. Working capital investments will increase net debt in FY24.

Reliance Retail (RR) has more than doubled the core area in the last 3 years and bulk of the additions were in 1HFY23 itself. We expect the ramp-up of the newly added stores to be the key revenue driver in FY24 and forecast a 30% core growth. Margins should moderate somewhat due to reversal of the Covid-related cost tailwinds, the continuing burn in new commerce and portfolio mix.

Digital and New commerce continues to be a focus area for the management, and we expect strong momentum. RR has now set eyes on FMCG business and has already announced a few forays (organic as well as M&A). This along with increased working capital requirements may drive the net debt higher.

Reliance Jio: Reliance is expected to deliver 19% y-o-y revenue growth led by tariff hikes in the mobile segment and continued traction in the non-mobile segment. “5G pricing/adoption and its impact on market dynamics is key monitorable. The timing and quantum of next tariff hikes and Jio’s response to Bharti’s rural expansion would also be key focus areas,” the brokerage said.

Also read: Gold: A Decent Start For The Year

Oil to Chemicals business (O2C)- Marginally better: RIL O2C business is expected to achieve 7% y-o-y Ebitda growth in FY24 on flat refining growth and recovery in petrochemicals in 2HCY2023. “We expect Sgp GRM to remain firm but lower y-o-y in CY2023 and withdrawal of export duties if crude prevails at $90 levels. We expect gradual recovery in petrochemical margins in 2H2023 as Chinese demand recovers,” it said.

Domestic E&P Ebitda to grow ~30% in FY24E: Elevated gas price and a 60% y/y jump in KG Offshore production should add US$ 0.55bn to FY24E Ebitda.

Renewable capex on schedule: First phase of solar PV module and grid scale battery plants will commission in 2024. It is working on pathways to lower captive round the clock renewable power cost to `3/KWh. This will result in $ 100 crore in annual power cost savings and improve economics of PV modules and green hydrogen production.

Attractive: RIL outperformed Nifty by 4% in CY22. We forecast 18% Ebitda growth in FY24E driven by 21% in RR and 24% in Jio. We see potential earnings upside from O2C if China’s demand recovers by mid-CY2023. Tariff hike in Jio, removal of export duties are other triggers. Current stock price imputes little value to green energy in our view. We have lowered FY23E EPS 2% on 4% reduction in Jio Ebitda (delay in tariff hike) and lower other income but FY24E is unchanged. Maintain Buy with `3,100 PT (23% potential upside).