Varun beverages (VBL) is well-place to capitalise on the opportunity that the early onset of summer/likely hot summer presents. The company has expanded capacity and distribution and built supply for the peak season well ahead of the usual schedule. Further, the strong growth momentum (100%+ y-o-y) of energy drink ‘Sting’ continues. Overall, the stage is set for another good year, and we see upside risk to our CY2023 estimates.

The company is prepared to capitalise on the opportunity, led by capacity addition and adequate stocks for the peak season, thanks to early ramp-up to peak utilisation. Sting—the energy drink can potentially deliver 100%+ volume growth in Q1CY23E. Stable raw material prices that are linlked to crude oil, an improving product mix with the brand (Sting) and operating leverage augur well for profitability.

VBL’s 41% volume growth in CY2022 was led by distribution expansion in underpenetrated markets (South/West/East India), stellar growth ‘Sting’ (up 160%+ to 63 mn cases, contributing 9.6% to India volume in CY2022; 16% salience in Q4), and an undisrupted hot summer. The GM decline was restricted to 180 bps y-o-y as 30% inflation in PET was partly offset by early stocking of RM, price increases, better product mix (Sting) and the rationalisation of discounts. Ebitda margin expanded 240 bps y-o-y to 21.2%, aided by operating leverage.

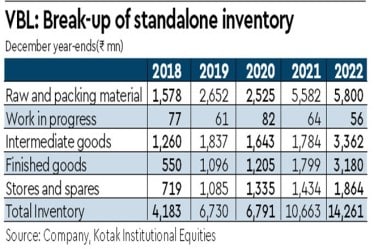

The cash conversion cycle increased to 41 days from 40 days, as the partial normalisation of inventory days was offset by a decline in payable days. The capex outgo for the year stood at Rs 18 bn—(i) Rs 6.3 bn: greenfield units in Bihar/J&K and brownfield expansion at Sandila, (ii) Rs 2.5 bn: brownfield expansion in Morocco and Zimbabwe, (iii) Rs 3.7 bn: land purchase for future expansion, (iv) increase in CWIP of Rs 1 bn to Rs 6 bn, and (v) capital advances of Rs 4.5 bn.

Also read: The yellow metal to shine ahead of March Fed meeting

The company is well-positioned to deliver 18%/26% revenue/ earnings CAGR over CY2022-24E, led by (i) continued success of Sting, (ii) significant capacity expansion, (iii) introduction/scale-up/pan- India rollout of new products (Dairy, Gatorade Rs 20/250 ml SKU, juices and Rockstar premium energy drink), (iii) distribution expansion by 10-15%/year,

(iv) further share gains in underpenetrated markets (South, West and East).