ONGC’s fy18 consolidated EPS was hemmed in by soft profits at OVL but much of this was due to non-recurring items. We expect FY19e earnings at OVL to more than treble therefore, with room for upside if oil prices stay high. Indeed, OVL and ONGC’s domestic JVs, petro-product sales and natural gas assets cushion earnings at a time when subsidies leave domestic net realisations uncertain. Even so, risk-reward appears favourable with the shares pricing in just $55 Brent.

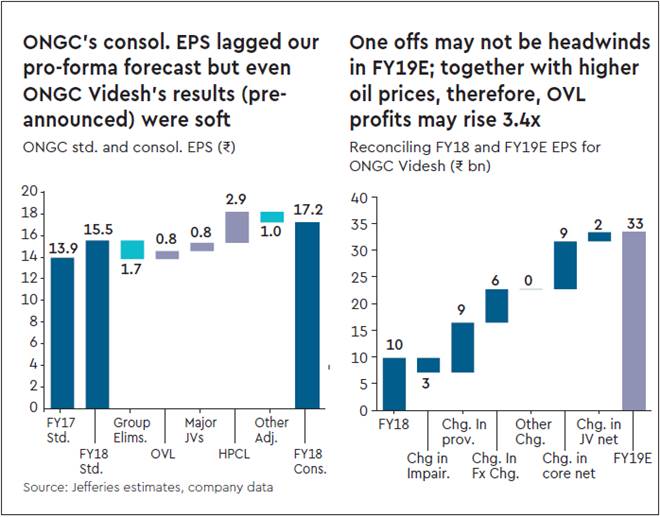

FY18: ONGC’s Q4FY18 net was better than JEFe but full-year FY18 consolidated EPS was still soft. While earnings fell y-o-y at MRPL, OMPL, OPAL and OTPC, OVL profits were also weak. Despite a full year contribution from Vankor that saw OVL production rising 10% y-o-y (to 23% of consolidated production), e.g., earnings rose 30% from a low base to just Rs 9.8 bn (4% of consolidated PAT).

One-offs: A closer look shows, though, that much of this was due to one-offs. It wrote back Rs 2.74 bn in impairments but added Rs 11.7 bn in provisions (mainly in Kazakhstan) with adverse forex changes and derivative losses (net Rs 6.3 bn) also hurting.

Oil prices: These may not recur with higher oil prices leaving scope for impairment writebacks like in FY18 (FSU and Lat-Am). Indeed, higher oil prices should help core EPS too; every $1 lifts OVL earnings by Rs 1.1 bn or Rs 0.09/share of ONGC, in our estimates.

Crude: We expect OVL profits to rise 3.4x to Rs 33 bn in FY19e, therefore — a key tailwind when subsidy risks cloud the overall outlook. Yet, OVL, domestic JVs, gas assets and petro products also cushion the impact of potential subsidies for ONGC.

Subsidies: Even if net realisations for the domestic oil assets were capped at say $55 Brent ($57 in FY18), e.g., we estimate FY19e earnings at Rs 19.7/sh (and Rs 22/sh at spot Brent of ~$76). Yet, these risks may be less pronounced than what investors envisage. The govt’s Rs 208 bn FY19 budget provision for LPG/SKO is inadequate and it appears jittery on auto fuel prices but it may also lean on downstream SOEs to share the burden like in FY03-07.

Risk-reward: Even otherwise, we find valuations inexpensive at 9.9x FY18 P/E ($58 Brent). Indeed, at its LT averages of ~10x P/E, the shares appear to be pricing in $55 LT Brent or $40-45 domestic realisations if current spot Brent of ~$76 holds.

Valuation/Risks: We keep our Buy, therefore, with a Rs 225 price target (SOTP incl. value of investments, Mozambique and KG-98/2). Subsidies or prolonged uncertainty around it are the key risk.