ONGC’s 4QFY19 earnings halved q/q to Rs 40.45 bn missing JEFe by 19% on higher exploration write-offs. EBITDA was in line with full-year standalone EBITDA up 37% y/y driving up EPS 34% y/y. With subs & JVs also doing better, esp. OVL where prod. is near all-time highs, consol. EPS rose 38% y/y to a new record too. We expect this to be broadly sustained in FY20E, even with subsidies, leaving valuations undemanding at 7.2x P/E. We keep our Buy with a higher Rs 205 PT.

Q4FY19: ONGC’s std. 4QFY19 net fell 51% q/q (-32% y/y) to Rs 40.45 bn missing subsidy-adjusted JEFe by 19%. A Rs 2.2-bn forex gain and higher other income helped but higher dry-well write-offs (Rs 27 bn), a pick-up in survey expenses (Rs 9 bn) and a Rs 12-bn impairment were drags as were higher interest expenses as gross debt rose again to Rs 216 bn. The Rs 40-bn buyback would have weighed on cashflow although capex was softer than in earlier years.

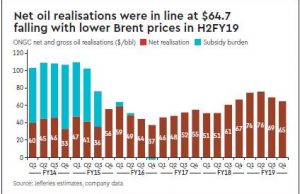

Core: As before though, operational performance was resilient with EBITDA in line with subsidy-adj. JEFe (-23% q/q, +7% y/y). Revenues were ahead, helped by higher own oil and JV gas sales, offset somewhat by marginally higher opex. Oil realisations ($64.7) fell as expected but it still left full-year realisations up 24% y/y to an all-time high of $71.

Full year: Indeed, with gas realisations also 20% higher in FY19, standalone EBITDA rose 37% y/y to a new record allowing standalone earnings to rise 34% y/y too to Rs 20.9/sh despite soft production trends. Oil production inched up 0.5% q/q, e.g., but remains near 30-year lows while gas production has also slipped from its highs in recent months.

Subs/JVs: And yet, consol. production rose to a new high in Q4 as output rose 4.6% q/q at ONGC Videsh. MRPL had a poor year but HPCL’s earnings were flattish.

Outlook: Overall, consol. EPS rose 38% in FY19, among the highest in JEF coverage, therefore. Indeed, this may sustain in FY20E helped by higher gas prices in 1HFY20 with room for upside if the Rs 56-bn subsidy burden that we model proves too harsh.

Maintain Buy: In turn, this leaves valuations at an modest 7.2x FY20E P/E with a 5% yield likely too after a soft 39% payout in FY19 that factored in the Rs 40-bn buyback. We keep our Buy with a Rs 205 PT (from Rs 195) noting that lower oil realisation is the key risk.