and now contributes 3.8% to domestic revenues.")

With 10% YoY growth, Nestle’s domestic revenues are in line with our expectations. Slightly better GMs & lower staff costs helped and Op Ebitda growth at 16% is ahead. Lower other income, however, resulted in an in-line outcome at the net level. Management is confident of managing disruption arising from the second Covid-19 wave although the bigger concern at the moment is on margins, following a sharp rise in input prices. We retain estimates & our Hold rating.

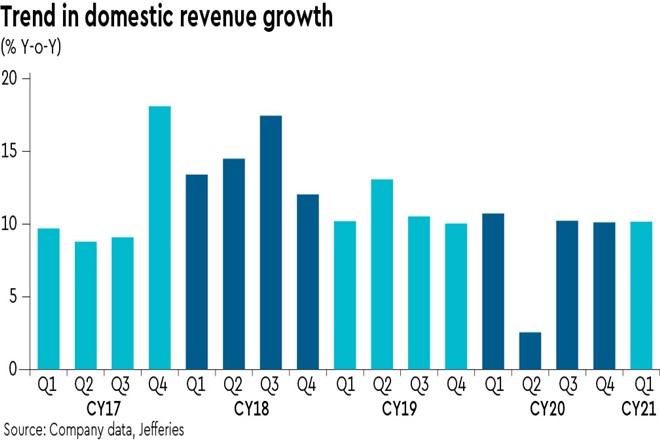

Double-digit growth: Domestic revenues grew 10% y-o-y, similar to the trend seen in the last two quarters. Overall revenue growth was slightly lower at 9%, as export revenues declined 13% due to lower exports to affiliates. Key brands such as Maggi noodles, KitKat, Nescafe Classic, Maggi sauces, Milkmaid and Maggi Masala-ae-magic grew in double-digits. Unlike other FMCG peers, Nestle performed well even in the March quarter last year and hence Q1CY21 does not have a favourable base.

Out-of-home: Nestle’s out-of-home portfolio recovered further q-o-q but remains impacted by Covid-19 disruptions. No comments made by the management on possible disruption due to the second Covid-19 wave; however, it does note that ‘the organisation has learnt to cope with the operating volatility in the pandemic’. However, local restriction would still impact the demand for OOH products, in our view.

E-commerce: The channel witnessed 66% growth y-o-y in Q1CY21 (after 110% growth in CY20) and now contributes 3.8% to domestic revenues.

Input inflation: Gross margin was a tad better than our estimates, down only 50bps q-o-q and up 240bps y-o-y to 58.4%. Gross profit growth was hence strong at 14%. However, going forward, management has sounded caution on the sharp escalation in prices of key inputs and packaging materials, which may impact GM.

Ebitda marginally above: Staff expenses grew just 3% y-o-y (-9% q-o-q). This was partly offset by 14% growth in other expenses, led by higher A&P spends. Ebitda margin, expanded 170bps y-o-y to 25.8%, the highest level in 12 quarters. As a result, Ebitda growth of 16% was marginally better than our estimates.

EPS in line: PBT grew 14% due to lower other income (-31% y-o-y). Pre-ex earnings grew 13% to Rs 6.0 bn and was in line with our estimates.

Retain Hold: We largely maintain our EPS estimates. We expect limited supply disruptions, at least for now due to localised restrictions, unlike last year, along with the learnings & better preparedness on the part of the industry, incl. Nestle. However, out-of-home demand would likely get impacted, like last year. Inflation in key input prices would be a key monitorable going forward. We retain Hold rating with a PT of Rs 18,000.