Jubilant Foodworks’ (JUBI’s) sales increased 12.1% y-o-y to Rs 9.9 bn (in-line), with SSS growth of 4.9% y-o-y (our estimate: +6%). Like-for-Like growth (i.e., sales growth of stores that were not split since 1st Apr’18) stood at 6.5% y-o-y. Ebitda was up by 59.3% y-o-y to Rs 2.3 bn (our estimate: Rs 2.3 bn) and adj. PAT rose 13.9% y-o-y to Rs 884 mn (our estimate: Rs 767 mn). Reported PAT was impacted by one-off provision of Rs 125 mn.

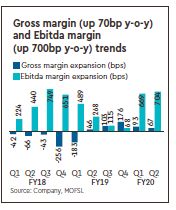

Excluding the Ind-AS 116 impact, underlying Ebitda was up 9.7% to Rs 1.6 bn with the margin at 16.4%. Gross margin expanded by 70bp y-o-y to 75.3% and Ebitda margin by 700bp y-o-y to 23.8%. Underlying Ebitda margin contracted 30bp y-o-y to 16.4%.

Valuation and view: The stock has been underperforming over the 12 months. As highlighted in our update note two weeks ago, JUBI’s competitive positioning will get stronger as a result of the corporate tax cuts. Moreover, the challenge of a high SSSG base eases significantly going forward and JUBI has done well in the face of 20% SSSG base in recent quarters. With demand stabilising, discretionary players with strong brands offer high scope for upside, in our view. We expect over 25% EPS CAGR and improving RoEs over FY20-FY22. Targeting 45x Sep’21e EPS (30% discount to five-year average P/E), we derive a target price of Rs 1,720, offering a 20% upside. Upgrading to Buy.