Is fast food still a hot business? We have seen how different brokerage houses have recently downgraded key food delivery stocks like Zomato and Swiggy, citing increased competition. But that’s not deterring this internet-driven multi-brand food services player from trying its luck in the equity market. Not just that, it is also keen about scaling up its presence in tier 2+ cities along with metros.

Guess, the brand we are referring to? Well, it does not just sell its products through its own app, but also via Zomato and Swiggy.

Curefoods, the parent firm of the famous brand EatFit, has filed its draft red herring papers (DRHP) with the markets regulator, Securities and Exchange Board of India (SEBI), on July 3, 2025.

Curefoods IPO: Issue size

The total offer consists of a fresh issue as well as an offer for sale (OFS) of equity shares of face value Rs 1 each. The company wants to raise up to Rs 800 crore through the issue of fresh shares, while it plans to sell up to 48.54 crore equity shares through OFS, for which the company has not disclosed the amount yet.

Curefoods IPO: Objectives of the issue

The net proceeds from the fresh issue will be used for various purposes, including funding inorganic growth through unidentified acquisitions and strategic initiatives and general corporate purposes.

Curefoods IPO: Are there any plans for pre-IPO placement

The company, in consultation with the BRLMs, may consider a pre-IPO placement of specified securities aggregating up to Rs 160 crore prior to filing the Red Herring Prospectus. If undertaken, the amount raised from the pre-IPO placement will be reduced from the fresh issue and shall not exceed 20% of the fresh issue size.

Curefoods IPO: Book runners and registrar

JM Financial, IIFL Capital Services (formerly IIFL Securities), and Nuvama Wealth Management are working as the lead book managers for the issue, while KFin Technologies has been chosen as the registrar for the IPO.

Curefoods IPO: Shareholder selling stake in OFS

There are 11 shareholders in total who are planning to offload their shares in the OFS. However, the company’s founder is not taking part in it. The details of the key stakeholders who are selling include-

•Iron Pillar PCC (acting on behalf of Iron Pillar PCC – Cell C and Iron Pillar PCC – Cell E): Up to 19.01 million equity shares.

•Crimson Winter Limited: Up to 9.76 million equity shares.

•Accel India V (Mauritius) Limited: Up to 4.57 million equity shares.

•Chiratae Ventures India Fund IV: Up to 3.66 million equity shares.

•Global eCommerce Consolidation Fund, L.P.: Up to 3.52 million equity shares.

•Chiratae Ventures Master Fund IV: Up to 2.79 million equity shares.

•Alteria Capital Fund II – Scheme I: Up to 1.43 million equity shares.

•Curefit Healthcare Private Limited: Up to 1.28 million equity shares.

•Shripad Shrikrishna Nadkarni: Up to 1.15 million equity shares.

•Horizon Techno Pte. Ltd.: Up to 930,900 equity shares.

•Zephyr Peacock India Growth Fund: Up to 335,037 equity shares.

Cruefoods IPO: What does the company do?

The internet-driven multi-brand food services company offers a wide range of cuisines to cater to diverse consumer preferences and dietary needs, according to the company’s DRHP.

As per the company’s Memorandum of Association (MoA), the objective is to provide food-based solutions for ordering and delivering healthy food and drinks. It wants to create a ‘just-in-time’ food supply chain and establish chains of cafes, restaurants, and eating houses that offer various cuisines.

Cruefoods IPO: Business model and channels

Curefoods operates through a multi-channel approach, providing food offerings under its brands through both delivery and non-delivery channels. These channels primarily include cloud kitchens, kiosks, and restaurants. So, you can order its food through its app and other food delivery apps as well.

According to the company, as of March 2025, it is the second-largest digital-first food services company in India (excluding food delivery marketplaces), based on revenue from operations for FY25.

In technical terms, the business model is based on a hub-and-spoke system, which enables scalability, reduces capital expenditure, and allows for service through multiple touchpoints.

Before moving ahead, let me explain the hub-and-spoke system. It is a network topology where a central hub serves as the primary connection point for multiple spokes or outlying locations. Think of a bicycle wheel, with the central axle being the hub and the spokes connecting it to the rim.

The company doesn’t like to invest in heavy assets like land purchasing. They operate entirely out of leased premises, including their Registered Office, Corporate Office, central kitchens, cloud kitchens, restaurants, and warehouses.

Curefoods had five central kitchens, 281 cloud kitchens, 99 kiosks, 122 restaurants, and 13 warehouses as of March 2025.

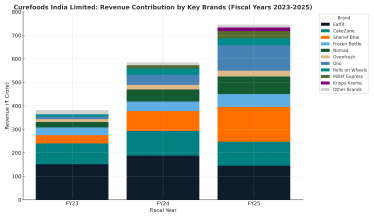

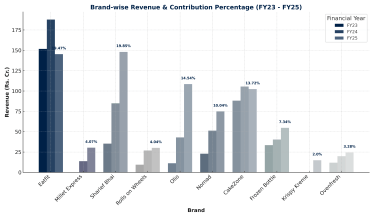

Cruefoods IPO: Brands of Curefoods

The company operates a portfolio of 10 key brands, generating over Rs 24 crore in FY25. Some of their notable brands include:

- EatFit (acquired in 2021, significant contributor to revenue)

- Cakezone (dessert offerings, acquired through Cakezone Foodtech)

- Sharief Bhai (healthy Indian cuisine, acquired through Fan Hospitality, expanded internationally in the UAE).

- Frozen Bottle (desserts, operated through Munchbox)

- Nomad Pizza (diverse range of pizza styles, operated through Yum Plum, includes sub-brands like Enso and Crunch)

- Millet Express (healthy Indian cuisine, acquired in 2024)

- Olio Pizza (acquired the company Bechamel that owned the brand in 2021, merged into our Company in 2023)

- Krispy Kreme (franchising rights acquired for South and West India in 2024 and North India in May 2025; revenue only pertains to generation by Curefoods under the rights)

- Other brands whose use is governed by deeds of assignment include “Pomp”, “Smoodies”, “Yumlane”, “Juno’s Pizza”, “Rolls on Wheels”, and “Captain Biryani”.

So, the company considers Krispy Kreme a key brand due to its strategic importance. However, it pays development, franchise, and royalty fees to Krispy Kreme Doughnut Corporation.

Curefoods IPO: Strategy and growth

The company’s growth strategy involves expanding its brand portfolio, increasing geographical footprint (especially in Tier 2+ cities), and accelerating delivery.

Curefoods’s approach has remained expanding through acquiring other brands, which it aims to continue in future as well. “The company aims for inorganic growth through unidentified acquisitions and strategic initiatives, leveraging deep industry insights to identify unique and synergistic opportunities,” read the DRHP. Past acquisitions include various brands and businesses to enhance market presence and offerings.

The company advertises through social media influencing and not using conventional TV ads, as the target customer base is mostly stuck to their phone screens. They focus on long-term brand building through social media activation and targeted marketing techniques.

Curefoods IPO: Operations and technology

The company emphasises quality control and food safety, operating under the ‘ISO 22000:2018’ food safety management system and sourcing from FSSAI-licensed suppliers. The company uses a lot of technological tools to manage its operations, which include:

- SupplyNote for end-to-end supply chain management, inventory tracking, and vendor coordination

- Oracle for finance, payment, and collections management

- Bluecopa for finance automation and reconciliation

- An AI-driven customer support system for streamlining queries

- Tools like Freshdesk for customer support and engagement

- Various internal systems for managing orders, kitchen operations, and supply chain

They have a robust supply chain with over 750 suppliers of ingredients and packaging materials and dedicated warehouses in key cities.

Key cities and regions where Curefoods operates

Curefoods India operates across a wide geographical footprint, with a presence in over 70 cities and towns in India as of March 2025.

- Metro cities

The company operates in major metro cities that include Bengaluru, Mumbai, New Delhi, Chennai, Hyderabad, Kolkata, Pune, and Ahmedabad.

- Tier I cities

While in Tier 1 cities, it has its operations in Mohali (Punjab), Patna (Bihar), and Kota (Rajasthan).

- Tier 2+ cities

In Tamil Nadu, it operates in three cities: Coimbatore, Salem, and Madurai. While it operates in Karnataka’s Mysore and Kerala’s Cochin.

- Intended expansion

It intends to expand in Uttar Pradesh’s Lucknow, Gwalior and Indore of Madhya Pradesh. It also wants to expand its operations in Beltola, Rajarhat, and Behala of West Bengal.

- International markets

Curefoods expanded its operations in the United Arab Emirates (UAE) by launching Sharief Bhai in 2024, and aims for further international expansion, leveraging the significant presence of the Indian diaspora.

Curefoods IPO: Financial performance

A look now at the company’s financial performance

Curefoods: Still no profit

The online food delivery play has reported losses for the last three years. According to the company, the loss was primarily due to significant expenses incurred on advertising and sales promotion.

- In FY23, Curefoods reported the largest loss, at Rs 342.73 crore

- In FY24, it posted a net loss of Rs 172.61 crore

- In FY25, the company reported a net loss of Rs 169.97 crore

The objective behind it was the expansion of its customer base and enhancing brand recognition. This apart, the inorganic expansion through business acquisitions and the launch of new service locations also contributed to the losses.

Curefoods revenue

The company has shown consistent growth in its revenue from operations over the past three fiscal years. Here is the revenue for the specified fiscal years:

- Fiscal 2023: Rs 382.04 crore

- Fiscal 2024: Rs 585.12 crore

- Fiscal 2025: Rs 745.80 crore

There was a consistent increase in revenue, reflecting a Compound Annual Growth Rate (CAGR) of 39.72% to FY25 from FY23. The revenue grew 53.16% to FY24 from FY23 and 27.46% to FY25 from FY24.

Curefoods claimed that it is the fastest-growing food services company in India in terms of revenue generation between FY22 and FY24, among companies that generated over Rs 500 crore in FY24.

Furthermore, it is the first food services company (excluding food delivery marketplaces) in India to generate revenues exceeding Rs 750 crore within five years of operations.

| Particulars | FY23 | FY24 | FY25 |

| Revenue | 382.04 | 585.12 | 745.8 |

| Net Loss | -342.73 | -172.61 | -169.97 |

Profit margin in focus

The PAT margin, which is calculated as the loss for the year as a percentage of revenue from operations, provides further insight into the company’s profitability:

- Fiscal 2023: (89.71%)

- Fiscal 2024: (29.50%)

- Fiscal 2025: (22.79%)

The loss for the fiscal year is also attributed to both the owners of the company and non-controlling interests. For instance, in FY25, Rs 159.65 crore was attributable to the owners, and Rs 10.31 crore to non-controlling interests.

Cash losses

For FY25, the cash loss was Rs 89.53 crore, and in FY24, it was Rs 183.02 crore. Similarly, for FY23, the cash loss was Rs 210.25 crore.

Curefoods IPO: Major shareholders

As per the DRHP, the company’s major shareholders include:

- Ankit Nagori: 88.7 million equity shares, representing 27.80%.

- 3State Ventures Pte. Ltd. (Formerly known as Three State Capital Pte. Ltd.): 55.26 million equity shares, representing 17.32%.

- Accel India V (Mauritius) Ltd: 22.88 million equity shares, representing 7.17%.

- Iron Pillar Fund II Ltd: 18.82 equity shares, representing 5.90%.

- Crimson Winter Ltd: 13.01 million equity shares, representing 4.08%.

- Iron Pillar PCC (acting on behalf of Iron Pillar PCC – Cell C): 12.96 million equity shares, representing 4.06%.

- Sixteenth Street Asian Gems Fund: 12.37 million equity shares, representing 3.88%.

- Chiratae Growth Fund – I: 9.93 million equity shares, representing 3.11%.

- Chiratae Ventures India Fund IV: 9.27 equity shares, representing 2.91%.

- Curefoods India Welfare Trust: 7.1 million equity shares, representing 2.22%.

- Chiratae Ventures Master Fund IV: 7.06 million equity shares, representing 2.21%.

- Iron Pillar PCC (acting on behalf of Iron Pillar PCC – Cell E): 6.13 million equity shares, representing 1.92%.

- Global eCommerce Consolidation Fund, L.P.: 5.26 million equity shares, representing 1.65%.

- Iron Pillar India Fund II: 5.26 million equity shares, representing 1.65%.

- RB Investments Pte Ltd: 4.27 million equity shares, representing 1.34%.

- Zephyr Peacock India Growth Fund: 3.35 million equity shares, representing 1.05%.

Curefoods IPO: Reservation of shares

The company has decided that it will not allocate less than 75% of the offer to Qualified Institutional Buyers (QIBs). Meanwhile, it wants to reserve up to 60% of the QIB Portion for Anchor Investors on a discretionary basis. Out of this, at least one-third is reserved for domestic Mutual Funds.

According to the DRHP, Curefoods will not allocate more than 15% of the offer for Non-Institutional Investors (NIIs) and not more than 10% of the offer for Retail Individual Investors (RIIs).

Curefoods IPO: Key risks associated

There are a lot of risks associated with Curefoods, like high dependence on food aggregators, diversified brand portfolio, unsuccessful acquisition, and others.

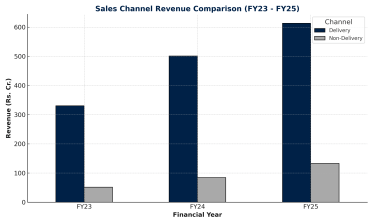

- Significant dependence on food aggregators: Curefoods heavily relies on food aggregators for selling its food offerings through the delivery channel. In FY25, the company generated 82.20% of its revenue through this channel. Any adverse changes in the policies or operations of food aggregators like Swiggy and Zomato, like an increase in commission, restrictions to data, visibility algorithms modifications, or the launch of their own cloud kitchen brands, could negatively impact the business.

- Risks with diverse brand portfolio: The company operates a portfolio of 10 key brands. These different brands cater to customers of various price points, cuisines, and meal preferences. The multi-brand strategy raises the risk of inventory management, increased overhead costs, and extended breakeven timelines.

- Unsuccessful new brand launches: The company may face challenges in successfully launching new brands, which could hinder its growth which may affect its business.

- Inability to successfully acquire new brands: Curefoods is not confident that acquisitions of other brands may turn out to be successful. Plus, they may require significant costs in terms of royalty payments, lease obligations, and other operating expenses.