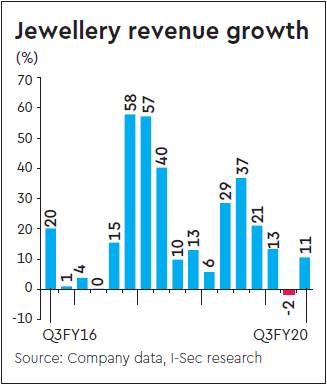

‘Growth’ was never under question for Tanishq; ‘Growth + Margins’ was. On that count it delivered on both in Q3. Jewellery sales grew 11%, continuing its market share gains in a declining category (c.-11%). Jewellery Ebit margins were nearly flat (-30bps y-o-y) despite a higher share of gold exchange. Similar to our other preferred pick JUBI, we model improvement in FY21 Jewellery growth (20%) from accelerated store expansions in smaller towns. Mandatory hallmarking effective FY21 is another catalyst for industry formalisation, of which Titan is a material beneficiary. Reiterate top-pick status on Titan along with JUBI.

Jewellery showing improved with festive sales: Company revenue/Ebitda grew 9/12% while PAT declined 3%. Comparable Ebitda (adjusting for Ind AS116) grew 8% as margin declined 20bps to 11.4%. Jewellery revenue grew 11%, at the lower end of management guidance of 11-13% for 2HFY20. Retail jewellery sales grew 15% in Q3 – the gap in company and retail sales magnified by a high institutional order (Rs2 bn) in the base quarter.

Accelerating store expansion to drive jewellery revenue in FY21: Tanishq added 13 stores in Q3 (after adding 21 in 1H), taking the total store count to 321 covering 1.2mn sqft as of Dec’19. We estimate another 15 stores to be added in Q4, taking FY20 store additions to 49, below the targeted 70 store additions. We believe that the miss is due to a delay in commissioning, meaning this gets spilled over to 1HFY21, which together with higher number of stores in 2H (historical trend) could result in sharp uptick in jewellery revenue growth for FY21.

Jewellery profitability impacted by higher advertising and management agents commission: Segment Ebit margin declined 30bps y-o-y to 13% despite a higher studded share (at 27% versus 25% in base). This was due to

(i) higher advertising expenses (a positive given need to gain market share in a declining category) and (ii) higher management agents commission (L2 stores) due to channel mix change.

Valuation and risks: We increase FY21 earnings by 2% to incorporate higher jewellery revenue growth expectations and adjust our model for Ind AS116. We model revenue/Ebitda/PAT CAGR of 17/21/20 (%) over FY19-22e. Maintain Add with a DCF-based revised target price of Rs1,450 (was Rs1,350) as we roll over. At our TP, the stock will trade at 50x P/E multiple Mar-22e. The key downside risks are: (i) high share (42% of revenues) of gold exchanges (consumers exchanging/bartering old jewellery and purchasing new jewellery), and (ii) any potential reduction in PAN card limit from Rs0.2 mn.