Hindustan Unilever (HUVR)’s Annual Investor Meet once again underlined the immense moats the company has and the remarkable nimbleness it has exhibited and continues to exhibit despite being much larger than peers. Mgmt shared details on the augmentation of its analytics and R&D strengths, which were already far superior v/s peers.

As highlighted in our Annual Report note, there have been a host of initiatives in the past year focusing on the burgeoning E-Commerce market, which now contributes 8–9% to HUVR’s sales. The company’s portfolio is already well-placed, with its E-Commerce market share higher than its Modern Trade (MT) market share, which, in turn, is higher than its General Trade (GT) market share.

Winning in Many Indias (WiMI) has been a key factor driving volume growth and market share gains for the company in recent years. However, the localisation of products as well as communication is only gathering further steam – of which the company stated several examples at the analyst meet in categories ranging from Foods to Beauty and Personal Care (BPC) – and ought to be a key driver of growth for many years to come.

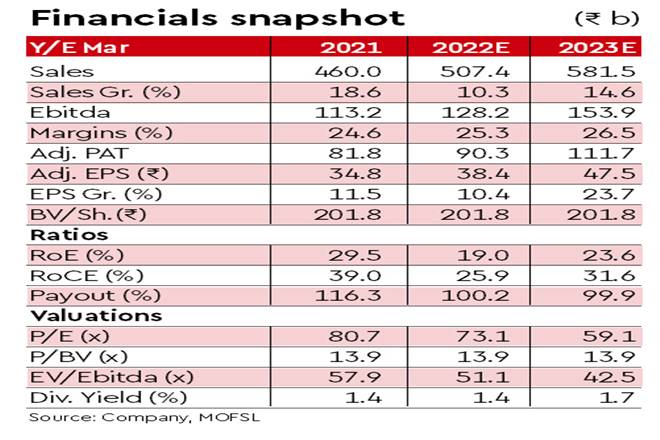

In the past decade, the company has seen a 9% sales CAGR and Ebitda margins have expanded ~1,000bp (despite the consistent guidance for modest improvement in operating margins). This was in spite of significant disruptions in the form of weak rural growth in the second half of the decade, demonetisation, GST, and COVID. Mgmt is aiming for double-digit EPS CAGR over the next 10 years, led by top line. With the long runway for growth in FMCG in India, increasing premiumisation, and synergies from GSKCH, we believe earnings could continue to compound at 14–15% over the next 10 years, similar to growth in the preceding 10 years.

The demand outlook is healthy as good rural growth in recent quarters would be sustained by good kharif (monsoon crop) sowing and recovery in the urban markets post the lockdown impact in Q1FY22. Commodity costs, while still elevated, have remained stable on a sequential basis, improving the margin outlook, especially with further price increases taken in Skin Cleansing, Detergents, and Tea in Q2FY22.

There is no material change in our forecasts. We maintain a Buy rating, with TP of `3,280 (60x Dec’23e EPS).