Hero has multiple growth headwinds in our view: (i) entry motorcycles will lag industry growth; BS-6 is an additional head wind; (ii) sharp decline of Maestro is a concern in an already weak scooter franchise; (iii) weak presence in premium motorcycles; (iv) exports ramp-up has been slow. High dealer inventory and margin pressures over FY19-21e add to our concerns. As a result, we believe valuation de-rating is justified and stay

cautious despite discount to Bajaj.

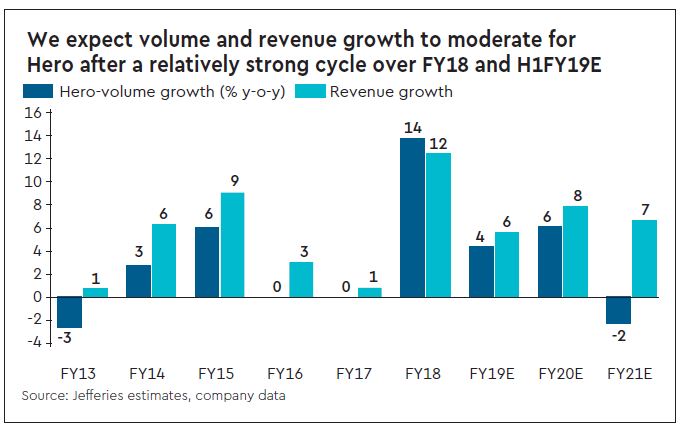

Multiple growth challenges

Hero’s growth prospect has multiple headwinds in our view: (i) we expect entry motorcycles, which account for 80% of Hero’s revenue, to lag industry growth in medium to long run; cost increase post shift to BS-6 will be particularly sharp for this segment in FY21e. (ii) Hero’s relatively weak franchise in scooters has weakened further with market share of Maestro Edge declining to below 3% vs. 7-8% till 2017; recent momentum in Destini 125 is unlikely to sustain; (iii) despite some new launches, we do not expect much traction in premium motorcycles; (iv) Hero continues to lag in exports, the other long-term growth opportunity.

ALSO READ: Tech Mahindra only Indian firm among top 20 global digital companies; check top 3

High inventory levels an overhang

Dealer inventory for 2-wheelers is currently high across OEMs—our channel checks suggest Hero’s may be even higher than industry average. This will hurt reported monthly wholesale growth in the near-term especially given high base over March to June last year.

Margin pressure to continue

We expect Hero’s margin to remain under pressure over FY19-21e given high competitive intensity and cost pressures. We estimate Ebitda margin to be in 13-15% range over FY19-21e vs. 15-17% over FY16-18. We cut revenue estimates by

2-4% and Ebitda estimates by 3-7% over FY19-21e to reflect weaker volume growth and margin. Our price target declines to `2,530 (prev. `2,700) and implies 13.5x FY20e/21e P/E.

Valuation de-rating justified

Sharp valuation de-rating in Hero over last 18 months and particularly its recent sharp discount to Bajaj has led to some interest in the stock amongst investors. However, we believe the valuation de-rating is justified given weaker growth prospects relative to 10-year history. We expect Hero to continue to trade at a discount to Bajaj, given latter’s better growth prospects in exports and value from KTM.