HDFC Bank delivered well despite challenges with 20% y-o-y rise in profit. With just 9% of loans in moratorium, high quality corporate book & steady cashflows for borrowers of unsecured loans, risk to asset quality should abate. On retail loans, (i) despite halt in lending, book is down slightly q-o-q indicating higher moratorium & (ii) tighter new lending can drag NIMs. Successor may be from existing leaders. We raise estimates & upside exists; our Buy call stays.

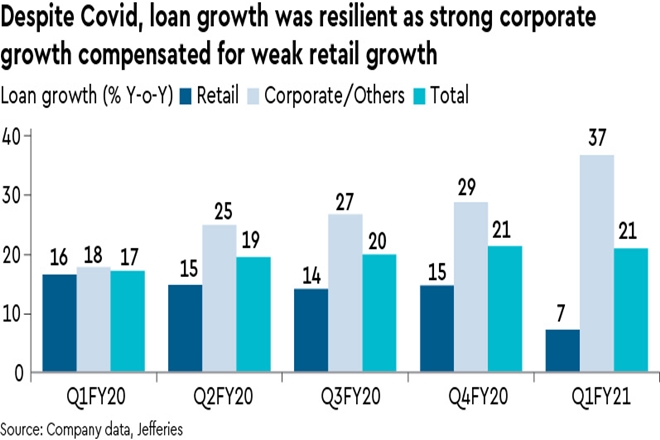

Pushing growth in corporate with high quality: Bank delivered 38% growth in corporate loans as it leveraged on deposit franchise and refinancing of capex and working capital loans. It maintained the high-rating profile of corporate loans with 86% of loans rated AA and above. Not only has it leveraged deposit franchise to gain market share here (deposits up 25% and Casa up 26% to 40% of total), it also leveraged corporate relationships for direct and salary deposit accounts. As highlighted earlier, banks with strong deposit franchise should see healthy growth in FY21-22 as they gain share from bonds and NBFCs.

Retail origination halts, ex-moratorium growth would be worse: Retail lending came to a near standstill with a combination of lockdowns and tightening of credit norms. Retail loans grew by just 7% y-o-y and were down 4% q-o-q — in fact, if not for moratoriums, book would have contracted even more given the short duration here (credit cards, personal loans, business banking etc.).

Topline & costs surprise positively; expect pressure on NIMs: Despite disruption due to Covid, the bank surprised positively with 20% growth in profit led by better topline and fall in non-staff costs . Going forward, we expect NIMs to see pressure from a rise in share of corporate loans, that will be partly compensated by uptick in fees.

Portfolio quality among the best: With just 9% of loans under moratorium, the bank has among the best asset quality in the sector. Though moratorium in Phase 1 isn’t provided, mgt. clarified that 70% of them cleared dues. We believe that retail loans would have higher moratorium, reflecting little q-o-q fall here — even in short-term loans. Slippages were higher at 1.5% of past year loans led by agri-NPLs and some pre-emptive downgrades (gross NPLs at 1.4%). The bank has beefed up contingent-provisions to 0.5% of loans.

Succession and staff issues: Aditya Puri clarified that announcement of successor will come soon and is likely to be from among long-standing internal leaders. On issue of personal misconduct in auto loans, the bank investigated & is following internal protocols.

Raise earnings: We raise estimates and see further upside if the bank can sustain momentum. With Tier I CAR of 17.5%, mgt. clarified it won’t need capital now. We maintain Buy with PT of Rs 1,350 based on 3.3x Jun-22E adj PB and value of stake in subsidiaries.