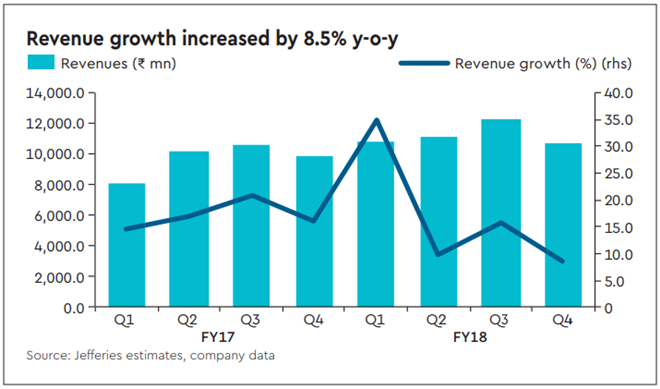

FLFL Q4FY18 LTL revenue growth of 8.5% y-o-y came in line with our estimates while Ebitda (down 4.2% y-o-y) and PAT (flattish) were below our expectations. 5% overall Same Store Sales Growth (SSSG) growth was decent considering apparel industry saw soft SSSGs impacted by lower discounting period during Q4FY18. Preferential issue to L Catterton Asia for 2% stake will lead to Rs 1.7 bn fund infusion and reduce debt (Rs 6.4 bn net debt currently) during FY19. We maintain Buy with TP of Rs 540.

Central: Central saw soft SSSG of 1% y-o-y though it came on a high base of 23.3% y-o-y. Company opened a total of five stores during FY18 on a net basis (2 stores in Q4FY18) taking the count to 40 stores.

Brand Factory: Brand Factory was the growth driver and saw strong 13.7% y-o-y SSSG during Q4FY18 on a base of 9.6% y-o-y. Innovative ways to drive footfalls such as The Big Bag sale (any 5 apparels at Rs 999), etc. helped SSSG. Company added 10 Brand Factory during FY18, taking the total to 63 stores.

Brands: Performance of brands saw improvement in Q4FY18, also helped by lower discounting days during which sale of own brand increases. Majority of the brands (except Scullers and aLL) saw strong growth — Lee Cooper (up 38% y-o-y), Indigo Nation (up 45% y-o-y), John Millers (up 48% y-o-y).

Margins: Adjusting for IND AS, gross margins expanded by 81bps y-o-y led by mix improvement (higher growth in own brands) and lower sale period, containing the impact of higher growth in lower margin Brand Factory. Ebitda margins however dipped by 113bps y-o-y impacted by 117bps y-o-y increase in staff costs — result of increased employees of Lee Cooper footwear business and ESOPs approved during FY18.

Estimates: We align FY18 numbers to that of the reported in terms of IND AS. We increase our Ebitda for FY19 and FY20 by 2% and 3% on higher margin due to increased growth in own brands.

Valuation/risks

FLFL stock is trading at 13x EV/Ebitda for FY20e which in our view keeps the risk-reward favourable considering the business model and consistency of the performance. We assign 16x March20e Ebitda to arrive at revised price target Rs 540. Risks to TP: (i) Higher competitive intensity leading to price cuts and increased promotions that puts pressure on margins; (ii) subdued performance in the owned brands.