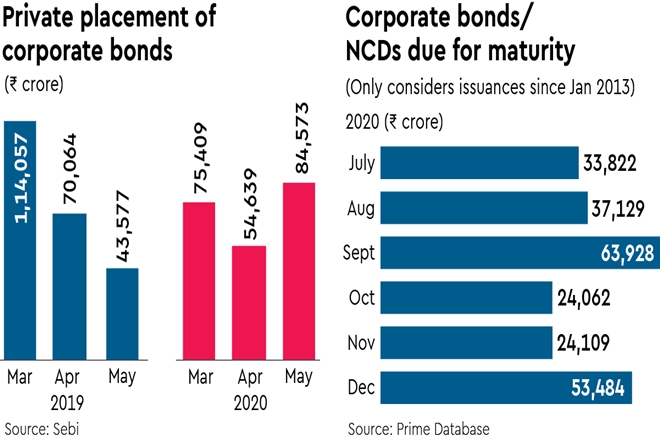

With the Reserve Bank of India (RBI) injecting surplus liquidity into the system through targeted long term repo operations (TLTRO) that helped boost the corporate bond market, private placement of corporate bonds between March and May this year stood at Rs 2.14 lakh crore, having fallen by just over 6% compared to the same period last year.

Experts say that the month of March generally witnesses huge volumes in issuances but the trend changed this time due to the Covid-19 crisis. Unlike last year when private placements in March stood at Rs 1.14 lakh crore, March 2020 saw only over Rs 75,000 crore worth of issuances.

Ajay Manglunia, MD and head of institutional fixed income at JM Financial, said TLTRO turned April and May 2020 into hectic months for the corporate bond market. “The funds that the banks took from the RBI in form of TLTRO have been gradually parked into corporate bonds over last two months. Banks usually do not buy so much of corporate bonds but the cheap funding via TLTRO brought in significant participation from their side. However, we may see a slower pace in private placement and may be a lower number in June,” Manglunia said.

With cash flow being a problem for many NBFCs, the potential for bond defaults are something that market participants are keenly watching out for; albeit, experts do believe that credit events with large and mid-size firms could be unlikely.

A Credit Suisse report dated May 2020 says rising risk aversion and accelerating rating downgrades are expected to add to Indian banks’ asset quality stress. “We estimated Rs 2.5 trillion of debt is already downgraded to ratings that are likely to make refinancing challenging. These ‘fallen angels’ have about Rs 220 billion of bond repayments due over the next 12 months,” the report stated.

Indeed, a good amount of corporate bond maturities are scheduled in the coming months. According to data provided by Prime Database, over Rs 1.34 lakh crore worth of corporate bonds/non-convertible debentures are due for maturity between July and September 2020.

MS Gopikrishnan, independent market expert, said larger NBFCs will be able to navigate through this phase through line of credit from their relationship banks. “We shouldn’t see any bond defaults from the larger and the mid-sized NBFCs. Also, the larger ones are being continuously monitored by the RBI as has been mentioned by the governor himself many times. However, the smaller NBFCs and MFIs are likely to find it difficult to go through this tough phase and I won’t be surprised if we see some defaults there,” Gopikrishnan said.

According to a CARE Ratings report, the credit risk of corporate bonds over government securities increased further in May 2020 as evidenced from the widening of the spread between G-secs and corporate bonds across credit rating categories on a month-on-month basis. “The widening of the spreads can be attributed to the concerns over the extension of the Covid-19 led lockdowns and the toll of the shutdown on businesses. The comparison of yield spreads on the last day of May 2020 with that of end April 2020 showed that the yield spread widened by 40 bps for bonds with ratings in the category of AA- to BBB- , while it broadened by 11 bps and 16 bps for bonds carrying ratings of AA+ and AA respectively,” the report stated.

inflows short of expectations: Barclays")