Although there will likely be impact of COVID-19 in the near term, the long term potential remains unaffected.

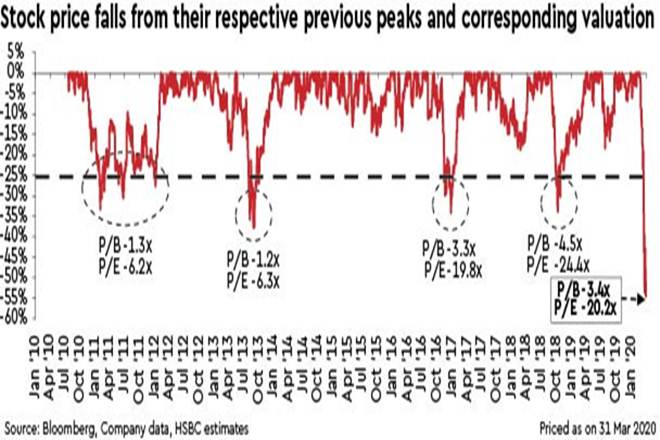

BAF stock has corrected sharply by 50%+ from its peak vs c31% and c41% fall in the Nifty and Bank Nifty indices, respectively. On comparison, past events such as taper tantrum (2013), note ban (2016) and IL&FS crisis (2018) resulted in 30-40% falls in the stock price, which makes the current fall unprecedented.

What are the key concerns? Investor concerns relate to (i) the immediate impact of the lockdown on consumption demand; (ii) impact on consumption demand in the event of a prolonged lockdown; (iii) asset quality outcome of the unsecured loan portfolio in the event of large-scale job losses; and (iv) the eventual impact on the return ratios and the valuations.

Near term highly uncertain: While it is difficult to project earnings in current scenario, we look at the factors that could impact earnings in near term – (i) run down in short term loan portfolios assuming very low levels of activity in Q1FY21; (ii) impact on net interest margins in view of run down in high yielding consumer durable loans; (iii) lower fee income driven by lower cross-sell activity; and (iv) rise in fresh delinquencies and credit costs.

What are the valuations factoring in now? We lower our FY21-22e earnings by an average 20%+ to factor in lower growth, lower NIMs and fees and higher credit costs. However, at current price the stock trades at 20.2x FY21e PE and 3.4x FY21e PBV for average ROEs of ~18% during FY21-22e and sustainable ROEs of 20%+. Although there will likely be impact of COVID-19 in the near term, the long term potential remains unaffected.

We believe this macro event will likely further strengthen BAF’s dominance in the retail loan segment. We expect the company to return back to the growth path sooner than expected once normality is restored. Retain BAF as our preferred pick among NBFCs; Buy with a revised TP of Rs 3,750 (from Rs 4,860).