Bajaj Consumer Care’s (Bajaj’s) Q1FY21 revenue, Ebitda and PAT dip of 18.4%, 19.2% and 11.4% y-o-y, respectively, was higher than our estimates. The company faced significant disruptions during the first fortnight of April, but operations reverted to near normal in May and June. Though LLP prices fell ~7% y-o-y, inferior mix due to sale of lower-margin product (sanitiser) and lack of sales in modern trade led to gross margin falling 330bps y-o-y.

Sharp cut in other expenditure (down 32.3% y-o-y) because of lower ad spends aided Ebitda margin a tad, whose dip was contained at 31bps y-o-y. We believe Bajaj should revert to its earlier dividend policy, especially looking at other companies such as HUL, which is considering a special interim dividend. Maintain Hold.

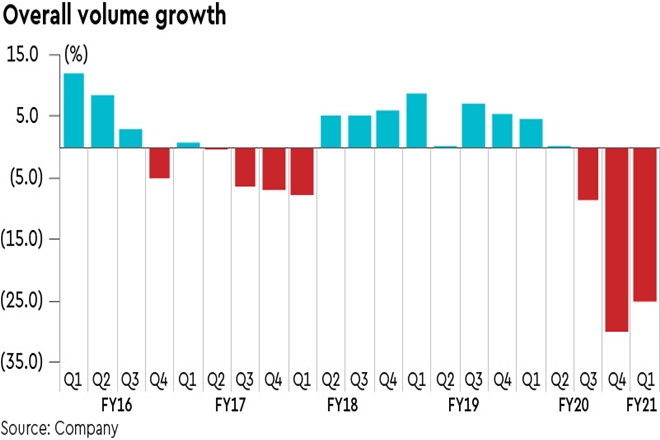

Hair oil takes severe beating; new launches to bolster revenue: Hair oil category, which was already clocking low growth, fell 6.9%, 50.6% and 25.2% y-o-y in March, April and May, respectively, in value terms. With its core category severely impacted, Bajaj’s agility to launch hand sanitiser under its Bajaj Nomarks brand should help near-term revenue to some extent. The company leveraged e-commerce channel to drive sales in Q1FY21. It launched Bajaj Zero Grey, a premium natural hair oil, on the platform.

Conference call takeaways: ADHO sales decline is 23.5% y-o-y. Overall hair oil portfolio declined by 25% y-o-y. Volume decline was also 23-23.5% y-o-y and no price changes have happened. More focus would be on absolute sales and sales growth as well as Ebitda growth.

Outlook: Gradual recovery—The consumption slowdown and Covid-19 have taken a toll on Bajaj’s volumes. Although financial stress at the promoter level has been alleviated, low growth in the hair oil category persists. Hence, we maintain ‘HOLD/SP’ with TP of Rs 195. The stock is trading at 11.1x FY22e EPS.