Axis Bank reported an ‘apparent’ Q2FY20 loss of Rs 1.1 bn, primarily due to the DTA markdown. That said, the quarter marks a strong core operating performance (with PPoP growth of 25%-plus y-o-y). Key highlights: (i) Slippages were elevated (at 3.9%), but not a negative surprise as 97% of corporate slippages stem from the watch list. Besides, limited downgrades to BB and below book lend comfort; (ii) sustained loan growth (>14% y-o-y) compared with moderation for peers, a better NIM (up 10bps q-o-q) and strong operating leverage (opex up merely 6% y-o-y) lifted core profitability.

While asset quality can be volatile ahead, we believe steps taken to de-risk strategy, strengthen liability and operating efficiency can help Axis turn in an RoE of 15–16% (even after recent equity raising). Capital buffer (tier-1 at 15.3%), the new management team and weaker competition imply Axis is well placed to capture emerging opportunities. Maintain Buy with a revised TP of Rs 850 (earlier Rs 761), factoring in recent capital raising.

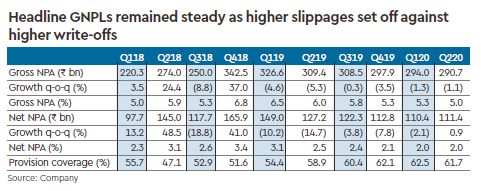

Slippages: Elevated but largely stem from watch list

Incremental stress continues to be elevated with slippages running high at ~Rs 50 bn (3.9%). However, we do not view it as a negative surprise given: (i) corporate slippages arise from the watch list; (ii) non-watch list slippages moderated (albeit too early to call it a trend); and (iii) lower downgrades to BB and below book has reduced the watch list to <2%. There were limited disclosures on eight stressed accounts highlighted in Q1FY20, but management did say that proportion of it has slipped or repaid and BB and below exposures fairly represents the stress pool. We reckon management’s aim of moving towards long-term average of credit cost is still some time away; we are, therefore, conservatively building in 2.4%/1.9% credit cost for FY20/FY21e.

Near-term RoE of 15–16% plausible; heading towards 18%-plus

We acknowledge limited NIM levers (despite capital raising), a volatile asset quality and the recent capital-raising pose challenges to the 18%-plus RoE target. The bank is likely to turn in 15–16% (post-raising) till FY21. Any progress towards 18%-plus driven by cost control and reduction in credit cost to long-term average would be an add-on.

Outlook: Credible changes

A clear strategy, credible road map to boost RoE, and strengthening franchise, not to mention de-risking initiatives, strengthen Axis Bank’s positioning in a weak competitive landscape. The recent capital will provide further succour. Maintain ‘BUY/SP’.

Better NIMs and cost control support core profitability

Loan growth momentum improved to 14% y-o-y (largely driven by sustained 20%-plus y-o-y retail growth). This along with better NIMs (10bps q-o-q rise) helped improve revenue traction (NII grew > 16% y-o-y). Lower cost (efforts getting visible) too helped core profitability (ex-treasury) register >25% y-o-y growth. While management has guided for stable to improving NIM in the near term and aims to achieve an NIM of 3.5–3.7% in two-three years, we perceive limited levers thereof (despite recent capital raising given limited levers on yield).